Here are the headline numbers from yesterday, with consensus numbers from CNBC

| Reported | Consensus | YoY Change | |

| EPS | $1.46 | $1.39 | 13% |

| Revenue (in $ billons) | 89.5 | 89.28 | -1% |

| iPhone Revenue (in $ billons) | 43.81 | 43.81 | 3% |

| Mac Revenue (in $ billons) | 7.61 | 8.63 | -34% |

| iPad Revenue (in $ billons) | 6.44 | 6.07 | -10% |

| Wearables Revenue (in $ billons) | 9.32 | 9.43 | -3% |

| Services Revenue (in $ billons) | 22.31 | 21.35 | 16% |

| Gross Margin (in $ billons) | 45.2% | 44.5% | Almost 300 basis points |

This is the fourth consecutive quarter when Apple reported revenue decline. It’s understandable why some investors are disappointed and critics are having a laugh. I can see why, but in this post, I’d like to talk about the nuances around Apple’s business that will help Apple investors digest the numbers. At least for me, I find such nuances helpful.

Year-over-year Comparison

YoY comparison is a useful method to evaluate how the business does compared to the same time 12 months ago. For a business like Apple, it removes the seasonality effect like you see below. With that being said, there are still nuances that come with YoY compare, especially when a company has some unusual reporting practices like Apple. First, it is important to know that once every 6 years, Apple adds an extra week to its December quarter (Q1 of a fiscal year). They did it for FY2023 and FY2017 before that. As a result, Q1 FY2023 had an advantage of an extra week while Q1 FY2024 will be disadvantaged by the same factor. To quantify the impact of this extra week, Apple CFO said it was worth 7% of Q1 FY2023 revenue.

The second performance element is foreign exchange. A global business like Apple is prone to changes in foreign exchanges around the world. For 6 consecutive quarters, this has been a performance drag to the company. For instance, in Q1 FY2023, foreign exchanges had a negative 800 basis point impact on revenue. Hence, although the company reported a decline of 5% in that quarter, on a constant currency basis, it would have been a 3% growth.

The third element is the timing of product launches. The company has multiple product lines and to keep the appeal to consumers refresh and invigorated every year, Apple must have new releases. And of course, when something new and fancy comes out, it usually drives sales more than old versions. Case in point, Apple disclosed that they had been supply-constrained for iPhone 15 Pro and iPhone 15 Pro Max; two most expensive phones that can drive margin. Because they expect to be supply-demand balance for the December quarter, Apple forecast similar revenue to the previous year despite having one less week.

The final element is force majeure. Unexpected incidents that are not under Apple’s control can negatively impact the company’s earnings. Tim Cook yesterday referred to a factory disruption last year that impeded the supply in the June quarter and led to the substantial record of the September quarter when pent-up demand was fulfilled. And let’s not forget that there are international incidents like what is happening in Israel or Ukraine, inflation or supply chain bottlenecks a while ago. These can be material drag to the company’s earnings.

Looking at quarterly revenue of the last few years, while it’s important to keep an eye on each quarter’s performance, it matters to acknoweldge that revenue is trending in the right direction: up and to the right. For a consumer staple brand the size of Apple, it’s no mean feat.

Margin

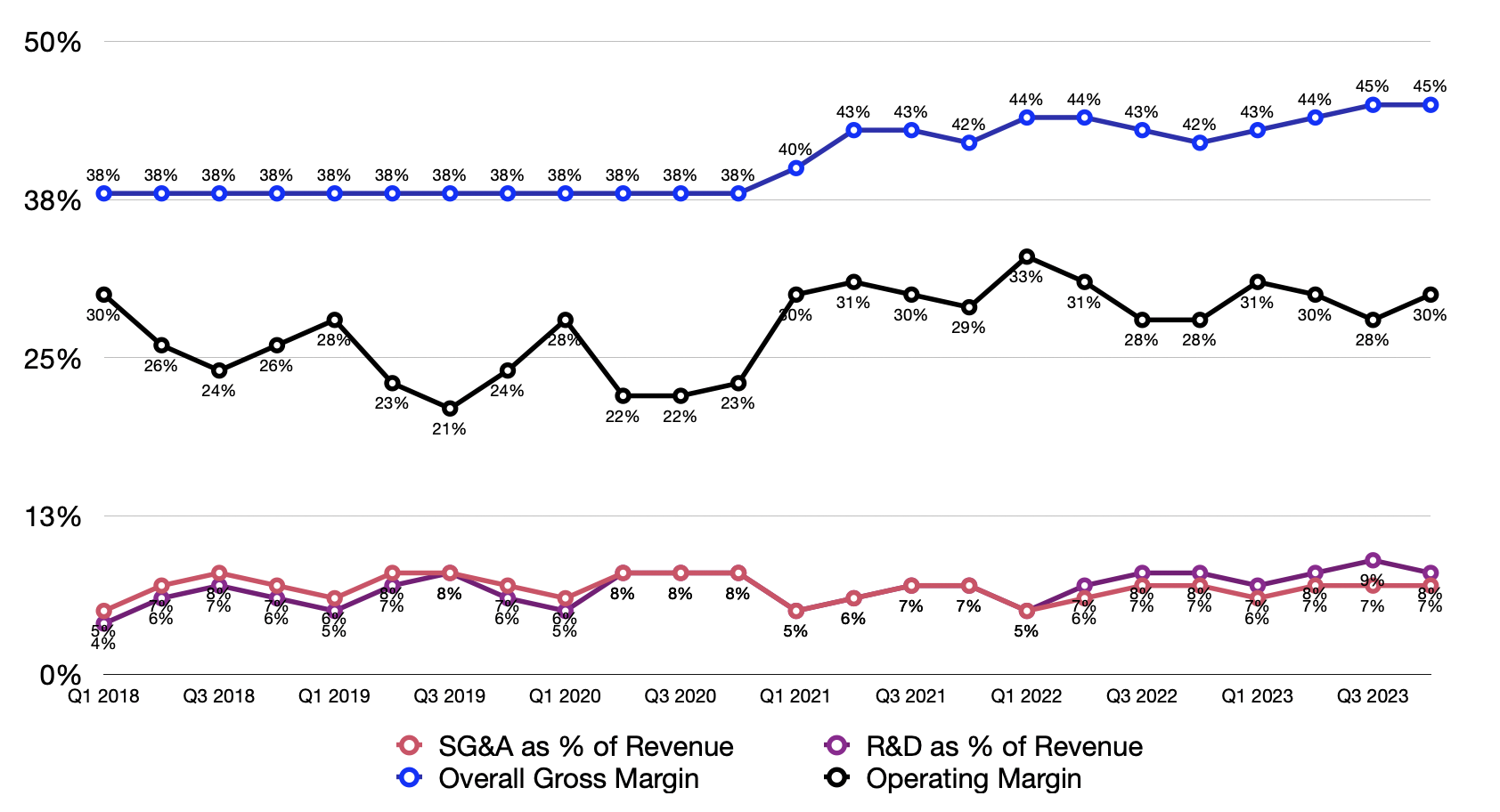

Below are Apple’s margins in the last 5 years:

Consistent. Predictable. Expanding. Those are the words that come to my mind. This is the hallmark of a well-run company despite its size ($2.6 trillion) and challenging market conditions. If you place a high value on the management and capable leadership, look no further than Apple’s executives. They set the standard in my opinion.

And there are signs that Apple can further raise its margins:

- The CFO mentioned that the elevated margin forecast for the December quarter would stem primarily from operating leverage and favorable mix of products. In other quarters, Services would play a bigger role in driving margin.

- Even though the new products have lower gross margin due to being early in the cost cycle, the higher end versions like iPhone 15 Pro and iPhone 15 Pro Max have favorable margins. And Apple expects to have enough supply for those two products in the December quarter.

- The company is launching Vision Pro next year. There is little information on its margin profile, but at $3,000+ per item, I assume it will be accretive to the company’s margin. Plus, Apple made it clear that its stores would be critical in letting customers test out the product and selling it. This direct channel will give Apple a higher margin than working with a carrier or a channel like Costco or Amazon.

- Apple said that its strategic R&D and M&A investments contributed to margin expansion as well. It’s likely we’ll see that play out in the future too.

In short, there are causes for concern over growth. The best case scenario, in my opinion, is single-digit growth in the near future. The baseline and low expectation is to have no growth and decline modestly. I still have faith in the company. And I look forward to seeing the impact of India and Vision Pro on the company’s performance.

Leave a comment