On Monday, Apple introduced its in-house credit card called Apple Card. Since it’s not available yet and the details are quite numerous, you can read more in these two articles on TechCrunch and The Verge or watch the presentation yourself here. I’ll just lay out my thoughts on the card below

I am convinced that Apple Card will attract a lot of sign-ups. After all, it’s Apple. The application process is reportedly straightforward and easy (we’ll see soon in the upcoming months). You can apply for the card from your Wallet app and the card will be shipped to you. If you use an iPhone 6 or later and are a fan of Apple, you will likely want to try your hands on the beautiful-looking titanium card for free, as long as you qualify for one. Plus, there are millions of installed iPhone 6 or later out there. So getting folks to sign up won’t be an issue. What about the usage for Apple Card? For consumers to use the Card, Apple has to give them a reason to, an incentive.

Security & Privacy

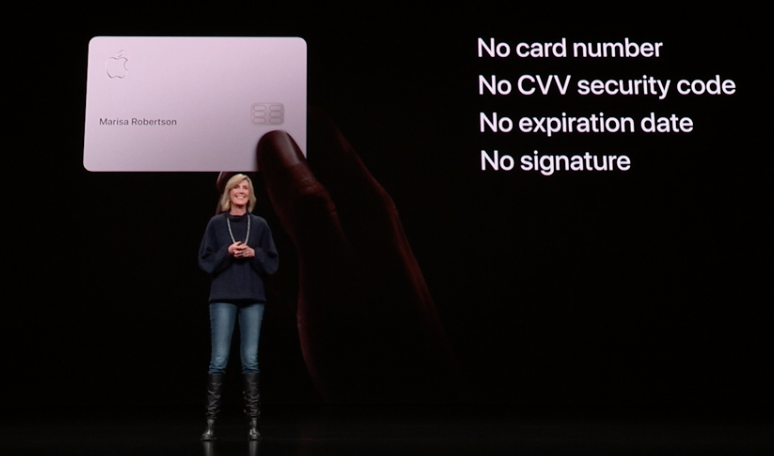

Security & Privacy is a big sell from Apple and it’s no different in this case. Apple Card comes without the stuff that makes credit card fraud possible from the physical card perspective. Plus, the way Apple sets it up makes credit card fraud significantly more difficult

Because of the way it is set up, every purchase with Apple Card requires biometric identification aside from purchases with the physical card. In the case of a non-Apple Pay transaction online — you must get your card number from the app and that is unlocked via Touch ID or Face ID, so biometrics are still in the path. And, for Apple Pay transactions, they are authenticated at the time of transaction. I personally think it would be cool to optionally require a confirmation from your phone to let a charge go through as well, but that is likely a v2 situation.

From TechCrunch

In other words, somebody needs to steal your card, your phone and either your thumb(s) or your face to make an unauthorized purchase.

Apple claimed that it wouldn’t know anything about consumer purchases using Apple Card. Plus, Goldman Sachs won’t sell data to marketers. If you care about privacy, it is attractive. Now that I work in the credit card industry, I can tell you that the level of privacy intrusion by banks is crazy. It is entirely possible to track the location of a cardholder to a store, know whether a purchase is made and if a purchase is not made, use the user data to run ads offline and online to motivate spending. If Apple and Goldman Sachs can do what they claim, this is an appealing feature, but I doubt it will be the dominant one.

No fees

According to Apple, you won’t be charged with late fees or penalty fees. You will just incur interest on your late payments. A nice feature, but from my perspective, it is not a hugely attractive one, especially if you are like me who isn’t late on credit card payments. After all, late payments will affect your credit score and consequently future APRs.

APRs

Pretty in line with the industry standard. Nothing special about this as far as I am concerned

Visibility into purchase details

Apple claimed that users could see more details on what a purchase was and where it happened from the Wallet app, instead of the user-unfriendly lines you see from your balance statement or mobile app. Once again, a nice feature that won’t be a dominant one.

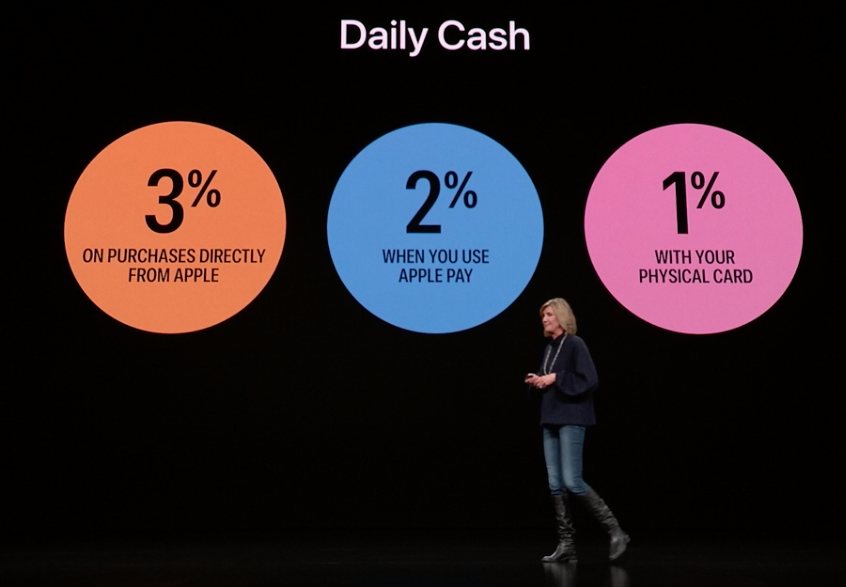

Cash back

Above is the cash back policy for Apple Card and Apple Pay. 3% on Apple-related purchases is nice, but it is not a daily event, given how expensive Apple items are. 1% cash back with the physical card is nothing special. It’s even less attractive than many credit cards out there on the market. The interesting one is Apple Pay

Because other credit cards offer two percent cash back or more on certain categories only, two percent cash back on every category by Apple Pay is more beneficial to users. According to Apple, Apple Pay will be available in 40+ countries at the end of this year. The number of merchants that accept Apple Pay is impressively high in some countries. Here is what Apple reported on the presentation

There are cases in which Apple Pay will not be competitive. For instance, if you have a card that gives back 4% cash back on dining, it sure is a better alternative than Apple Pay, even if Apple Pay is an available option. Or if you have a co-branded credit card such as a hotel or airline co-branded credit card, there is a switching cost as you want to increase your rewards points.

But using a physical credit card isn’t as convenient as a contactless option such as Apple Pay, nor is it as secure. So which payment option works in a situation depends on what situation that is and what kind of credit card user you are. If you care a lot about rewards and cash back, as well as have the time and mental fortitude to remember all the details, using multiple cards is the way to go. Nonetheless, if you are like me, a “one guy, one card” type, I would prefer something simple and easy to use/remember. Then I can see the appeal of Apple Pay. Contactless, fast, secure and decent cash back.

A push for Apple Pay

I believe that Apple Card is another push for Apple Pay to make it the “iPhone” equivalent of payment methods. Since Apple Pay is not ubiquitously available, the Card offers the connection between Apple Pay and merchants who don’t accept the service yet. If you use the Card, you’ll earn cash back that can be, in turn, used for Apple Pay. As explained above, Apple Pay can seem to be an attractive payment method to a certain type of users. According to Apple, they are on their track to meet the goal of 10 billion transactions on Apple Pay this year. If you are already satisfied with Apple Pay, I suspect that you will get more hooked when Apple Card is launched.

It makes sense to push for Apple Pay as I think Apple will earn more revenue from the service than the Card. After all, whatever revenue from the Card will have to be split with Goldman Sachs as well.

To recap, I think that this is a push for Apple Pay from Apple, an attempt to thread a delicate line between getting into the financial world and not suffering from the regulatory headaches that come with actually getting in there. Personally, I don’t think it is a “winner takes all” situation. I suspect that users will carry multiple options around and that each type of credit card user will display different levels of love towards Apple Pay and Card. I am excited about the future updates from Apple for the Card, regarding features and benefits. After all, this is just their first iteration.

Leave a comment