Highlights from the press release and earning call

- iPhone sale down by 17% YoY. Mac had a great quarter with a YoY increase of 21%. Mac had a 5% revenue decline compared to last year

- Half of the Mac customers during the quarter were new to Mac and the active installed base of Macs reached a new all-time high

- 75% of the Watch customers never owned a Watch before

- Apple Pay transaction volume more than doubled year-over-year and on track to reach 10 billion transactions this calendar year. Apple Pay is now available in 30 markets and will be live in 40 markets by the end of the year. New York’s MTA system will begin their rollout in early summer.

- 390 million paid subscriptions at the end of March, an increase of 30 million in the last quarter alone.

- “As we mentioned in January, we’ve been working on an initiative to make it simple to trade in our — trade in a phone in our store, finance the purchase over time and get help transferring data from the old phone to the new phone. As part of this initiative, we rolled out new trade-in and financing programs in the U.S., China, the U.K., Spain, Italy and Australia. The results had been striking. Across our stores, we had an all-time record response to our trade-in programs and with more than 4 times the trade-in volume of our March quarter a year ago.”

- All-time services revenue records in four of our five geographic segments. Services accounted for 20% of March quarter revenue and about one-third of gross profit dollars.

- “In fact, the number of paid third-party subscriptions increased by over 40% compared to last year in each of our geographic segments. And across all third-party subscription apps, the largest accounted for only 0.3% of our total Services revenue.”

- Wearables business grew close to 50%

- Total cash, plus marketable securities: $225 billion. Total Debt: $113 billion

- App Store search ad business: up around 70% over the previous year and expanding into new geographies

- An additional $75 billion for share repurchases is authorized

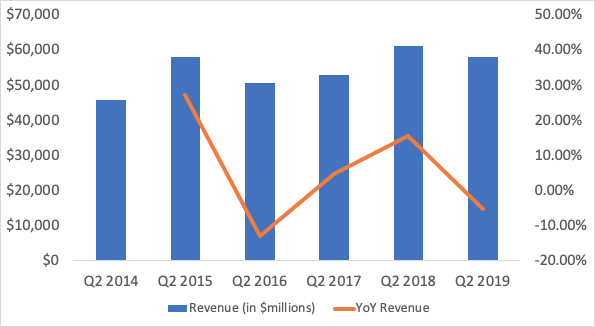

Note: In the following chart, Other Products refers to Wearables, Home and Accessories . I tried to update the historical figures as much as possible, but there might be some discrepancies to the latest ones.

Revenue in Q2 2019 is down by 5% YoY

iPhones and Mac disappoint while the other segments impress year over year

iPhone and Mac’s makeup of Apple’s total revenue continued to decline. Services and Wearables/Home/Accessories become increasingly more significant

Revenue from Greater China as % of the total revenue continues to slide while Americas’ share went up this quarter

Both Gross and Net Margin decline year over year

| Quarter | GrossMargin | NetMargin | R&D/Rev | SG&A/Rev |

| Q2 2014 | 39.32% | 22.40% | 3.12% | 6.42% |

| Q2 2015 | 40.78% | 23.39% | 3.31% | 5.96% |

| Q2 2016 | 39.40% | 20.80% | 4.97% | 6.77% |

| Q2 2017 | 38.93% | 20.85% | 5.25% | 7.03% |

| Q2 2018 | 38.31% | 22.61% | 5.53% | 6.79% |

| Q2 2019 | 37.61% | 19.93% | 6.81% | 7.68% |

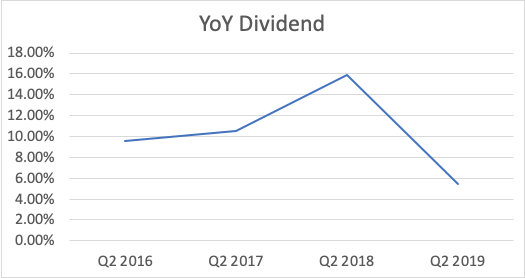

Dividend growth decreased compared to last year

My thoughts

Though revenue went down compared to last year, it’s not that bad in my opinion. It is almost on the same level as Q2 2015 when iPhones made up 70% of the total revenue. Services, iPad and Wearables seem to be able to make up, at least for now, some of the lost revenue from iPhones. The continued drop of Gross Margin is concerning and so is the almost 3% decline in net margin.

As customers prefer keeping and using their phones longer and Apple is losing ground in China, a major market for the iPhones, I think the iPhone share in the revenue pie will become smaller while Services will be more important to the company’s health. Tim Cook wasted no time on emphasizing that this is the best quarter for Services as it made up 20% of the total revenue and 1/3 of the total gross profit. Much time was spent on a whole range of services. I look forward to seeing the remaining two quarters of the year and the first of the next year after many services announced last month debut.

I actually prefer the trade-in initiative to lowering the prices as the initiative will likely not dilute the brand value as much as price cuts, especially for a luxury brand such as Apple. It’s promising to see the response to the new trade-in program.

While it’s interesting to see a significant growth in the App Store search ad, I am concerned about what it would do the image of a privacy-focused brand such as Apple. Ads and privacy don’t actually go hand-in-hand.

Disclaimer: I owned Apple stocks. This post is a practice exercise and stems from my curiosity. It’s not intended to be investment advice or anything of the sort. I am not that good lol.

Sources:

https://www.apple.com/newsroom/pdfs/Q2%20FY19%20Consolidated%20Financial%20Statements.pdf

https://investor.apple.com/investor-relations/financial-information/dividend-history/default.aspx

Leave a comment