Today, the security startup CrowdStrike filed to go public and the numbers look impressive in my opinion.

Company background

Founded in 2011, CrowdStrike is a cybersecurity startup that offers their services mainly on a subscription basis. The primary offerings include endpoint security, vulnerability management, threat intelligence and a PaaS solution for cybersecurity.

Growth

- Subscription customer base grew from 1,242 at January 31, 2018, to 2,516 at January 31, 2019 – a 103% increase

- Customers include 44 of the Fortune 100, 37 of the top 100 global companies, and nine of the top 20 major banks

- Total revenue grew from $52.7 mil in 2017 to $119 in 2018 and $250 mil in 2019, an increase of 125% and 110% respectively

- Subscription revenue grew from $38 mil in 2017, to $92.6 mil in 2018 and $219.4 mil in 2019, an increase of 144% and 137% respectively

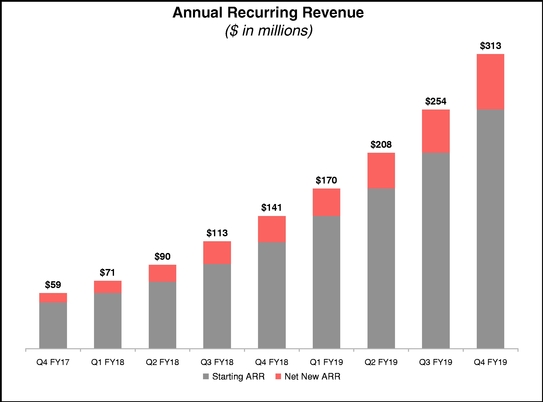

- ARR growth is impressive as shown below

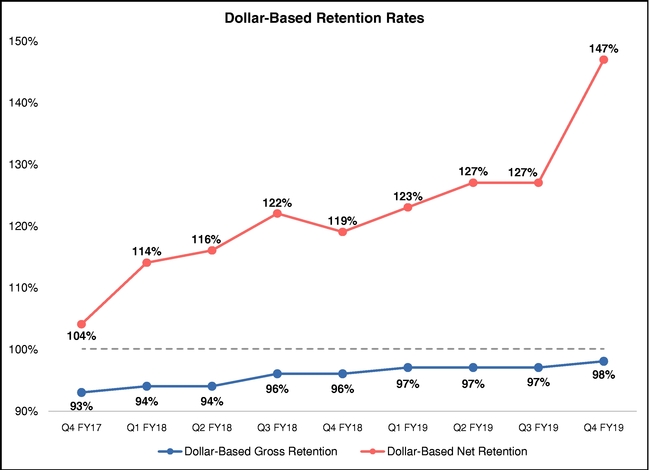

- Dollar-based net retention rate grew from 104% in Q4 2017 to 147% in Q4 2019

- 23% of the company’s revenue came from customers outside of the US in 2019, up from 13% in 2017

Partner & Customers

- CrowdStrike is deployed on AWS GovCloud after receiving FedRAMP recently

- Dell & SecureWorks use CrowdStrike’s endpoint security solution

- Customers include AWS, HSBC, ADP, Hyatt Hotels, The Pokemon Company

Listed Competitors

- McAfee, Symantec, Palo Alto Networks, FireEye, Cylance and Carbon Black

Financials

- The company grew the top line significantly while the operating loss had a much smaller increase

- The increasingly profitable subscription that already has higher gross margin than professional services makes up a bigger piece in the revenue while expenses are better leveraged

Thoughts

The company claimed to have a TAM of $24.6 billion and $29.2 billion in 2019 and 2021 respectively. It is a huge market and as companies go digital and have increased exposure due to more endpoints, more data, more cloud environments and more applications, the cybersecurity need will be there. With that being said, it is also a competitive market. Not only are there quite tough competitors such as Palo Alto Networks, McAfee, Symantec, FireEye, but there are also some smaller ones and on top of that, public clouds such as AWS or Azure also have their own security offerings.

I don’t know how they will compete moving forward, but the numbers look pretty good so far. Like many enterprise SaaS companies filing to go public, the company hasn’t been profitable operationally yet, but the situation looks promising with increased revenue and leveraged expenses. Their growth in ARR, negative churn and customer base is impressive. At least, there is a reason to believe that they are heading to the profitability land.

The partnership with Dell, I think, will be very helpful moving forward.

Leave a comment