Netflix earnings

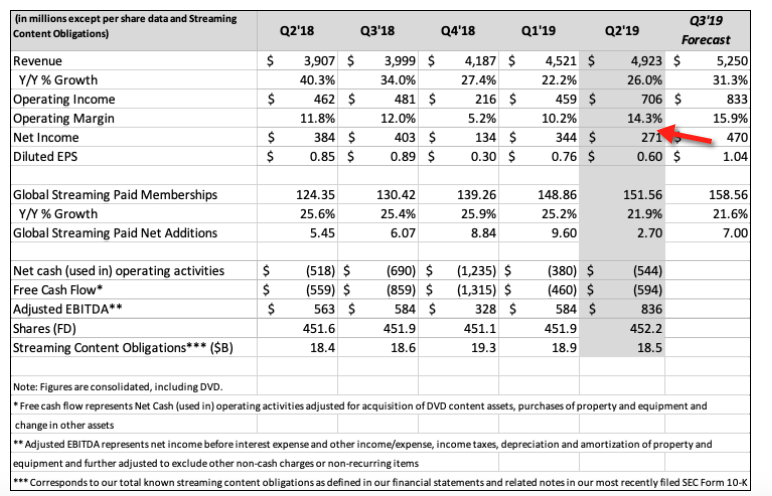

Netflix’s earning gave the bears something to boast about as the streamer reported the first domestic subscriber decline in years and also the biggest miss against forecast ever. Though the missed forecast was felt in all regions, it was even more so where there was a price hike. It begs the question: how much wriggle room does Netflix have to increase its prices?

As the company invested so much money in original content and gave significant discounts to sign up users in markets such as India, squeezing out users in established and lucrative markets can be a solution. Yet, if anything, this quarter showed that it might not be a straightforward solution for the household brand.

Throw in the future fierce competition in Disney, HBO or NBC and the loss of staples such as Friends, The Office or Future Marvel Blockbusters. It’s not unreasonable to cast some doubts over Netflix’s future.

With that being said, it’s not really certain that Netflix’s doom is under way. It is still the biggest streamer out there with 151 million paid memberships worldwide. It is a household name that is familiar with consumers around the globe.

Thought the growth slowed this quarter, adding net 2 million subscribers in 90 days with improved Operating Margin and Contribution Margin is not bad at all.

The huge subscriber base will play to Netflix’s advantages as the more users it has, the more its costs, especially fixed ones such as licensing fees, production or infrastructure, are spread. Netflix’s future competitors such as Comcast, Warner Media or Disney will have to build up their user base from scratch and the cost per user in the beginning will be much higher than that of Netflix.

As the streaming war drags on, will the new services have enough resources or stomach to be in the game? Especially given the expensive investment in releasing quality content regularly and the risk of losing subscribers from price hikes. Of course, one can argue that Netflix can just be patient and play the long game, but on the other side, most of its competitors have resources to spare and other revenue streams to chip in.

I honestly don’t know how Netflix will fare in the future. There is merit on both the bears and the bulls. Because of that, it’s interesting to follow the company.

CrowdStrike Earnings

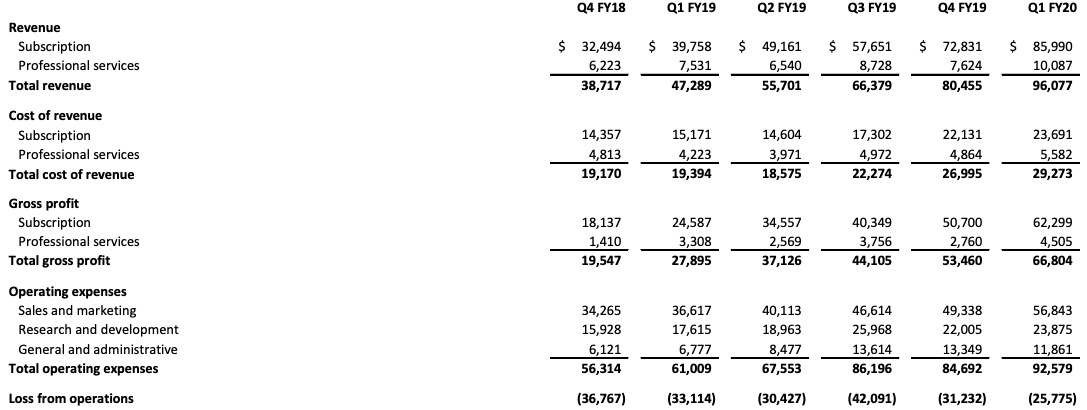

The cybersecurity firm achieved 100% YoY growth in revenue this quarter. Gross margin increased to 70% in Q1 2020 from 59% in Q1 2019. Subscription revenue, as the more profitable segment, made up 90% of total revenue this quarter, compared to 85% one year ago. Operating loss as % of revenue was -27% in Q1 2020, compared to -70% in Q1 2019.

The company’s annual recurring revenue and subscription count growth are still in the 3-digit territory. Operating cash flow is already positive. One concern is that free cash flow is still negative, though it can be attributed to the investment in equipment

A few notable points from their earning call

Next, I will highlight a win that represents our tremendous opportunity to expand within our customer base. This customer is in the public sector, which also speaks to our growing success in that segment of the market. We initially engaged with this large U.S. city back in 2016 on a small deployment of 15,000 endpoints to replace a fossilized AV vendor that was failing to provide protection and value. We replaced that vendor with our combined EDR next-gen AV offering plus OverWatch.

Based on the success of the initial deployment, we expanded our footprint to over 250,000 endpoints the following year. And I’m pleased to report that in Q1 of this year, we have increased coverage to 400,000 endpoints and sold additional cloud modules, including Falcon Discover for IT hygiene, Falcon Device Control, Falcon Spotlight for vulnerability management, and Falcon X for integrated threat intelligence. This is a great example of how we can land a new customer and expand that relationship by adding endpoints and modules over time. Our Falcon platform is one of the most strategic security purchases they have made in many years.

SeekingAlpha

In addition to winning new customers at a rapid pace, we’re also focused on expanding our relationship with existing subscription customers by deploying additional cloud modules and protecting more of their endpoints. Our dollar-based net retention rate speaks to the efficacy of our solution in our successful land and expand sales model. As of January 31, 2019, we had a dollar-based net retention rate of 147%. While this metric can fluctuate quarter-to-quarter, our benchmark is 120% or above, which we again exceeded in Q1.

SeekingAlpha

While professional services carry a lower gross margin that our corporate average, it is a small portion of our revenue base and we view it as strategic. We have been able to derive an average of about $3 of subscription ARR for every $1 spent on an initial incident response for proactive services engagement. To be clear, these are customers that are new to CrowdStrike.

In terms of geographic breakdown, approximately 75% of first quarter revenue was derived from customers in the U.S. and 25% from international markets.

SeekingAlpha

The first post IPO quarter of CrowdStrike looks like a successful one. Really look forward to the company’s future performance in a competitive space.

Leave a comment