Apple announced their Q4 earnings today. Below are my notes of the earnings report.

Before we go to the financial analysis that I did, here are some noteworthy remarks from the investor call (Source: Seeking Alpha)

- This Q4’s revenue is the highest ever. The tailwin in foreign exchange was estimated to be around $1 billion

- iPhone 11 has been the best selling phone since the launch

- Services saw record growth in revenue in all five geographic segments

- “For Apple Pay, revenue and transactions more than doubled year-over-year with over 3 billion transactions in the September quarter exceeding PayPal’s number of transactions and growing four times as fast. Apple Pay is now live in 49 markets around the world with over 6,000 issuers on the platform. We believe that Apple Pay offers the best possible mobile payment experience and the safest, most secure solution on the market. We’re glad that 1000s of banks around the world participate.”

- Customers will be able to purchase new iPhone and pay for it with Apple Card over 24 months with zero interest

- Wearables saw record revenue in all tracked markets

- Record revenue was recorded in the U.S., Canada, Brazil, the UK, Germany, France, Italy, Poland, Korea, Malaysia, the Philippines and Vietnam

- “Our active installed base of iPhone continues to grow to a new all-time high in each of our geographic segments. And in the U.S., the latest survey of consumers from 451 Research indicates iPhone customer satisfaction of 99% for iPhone XR, XS and XS Max combined. Among business buyers who plan to purchase smartphones in the December quarter 83% plan to purchase iPhones.”

- 450 million paid subscriptions compared to 330 million over a year ago

- “We generated an all-time revenue record for Mac in the US and in India and a fourth quarter revenue record in Japan. More than half of the customers purchasing Macs during the quarter were new to Mac, and the active installed base of Macs again reached a new all-time high.”

- “iPad revenue grew in all five of our geographic segments with a Q4 revenue record in Japan. In total, over half of the customers purchasing iPads during the September quarter were new to iPad, and the iPad active installed base also reached a new all-time high. The most recent surveys from 451 Research measured a 95% customer satisfaction rating for iPad from consumers and 97% from businesses. And among both consumers and businesses who plan to purchase tablets in the December quarter more than 80% plan to purchase iPads.”

- Cash and marketable securities stand at $260 billion. Net cash stands at $98 billion

- ″In terms of hardware as a service or as a bundle, if you will, there are customers today that essentially view the hardware like that because they’re on upgrade plans and so forth. My perspective is that will grow in the future to larger numbers. It will grow disproportionately”

The following financial analyses are what I compiled from 2014 to now. For YoY comparison, there won’t be any figure for 2014. 2014 still appears on the charts, but only because it will take me too much time on my computer to remove it. Please bear with me.

Operating Margin, Top and Bottom Line Observations

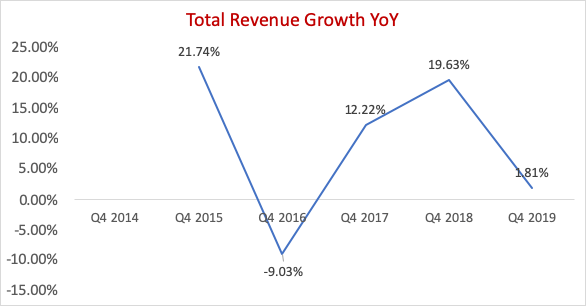

Revenue reached all-time Q4 high even though the growth is modest compared to the two previous years.

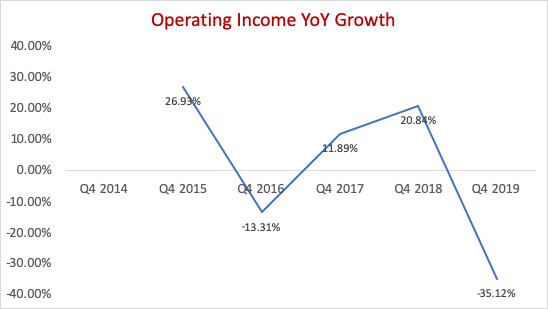

Operating income actually dropped quite significantly as the cost of sales increased, lowering both margin and the net income growth.

Product Segment

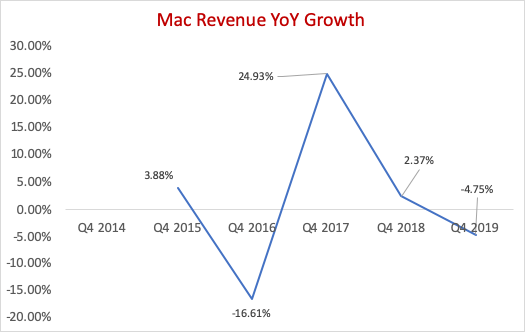

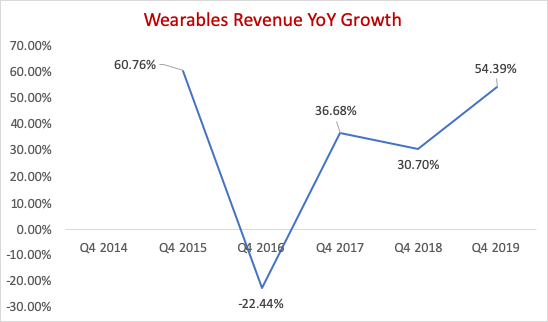

As you can see below, Mac and iPhone declined year over year. The decline was offset by growth in iPad, Services and Wearables.

iPhone still makes up more than half of Apple’s revenue, but its influence has been waning over the past years. Meanwhile, Services and Wearables have been on the rise, with the latter now bigger than iPad. Services in Q4 almost made up 20% of Apple’s total revenue.

Transition to a higher margin Services-focused company

Apple has reported figures for Product and Services for the past two years. Product segment made up 80.5% of Apple’s total revenue, down from 83% from a year ago. It was offset by the rise of Services, up to 64% from 61% a year ago. It’s a good trend if you look at gross margin. Services carries twice as big gross margin as Products.

Regional Segments

Americas is still the dominant geographic segment for Apple. China has been slightly declining, standing at around 17% of Apple’s total revenue. Rest of Pacific has been increasing, even though its size is relatively small compared others’.

However, in terms of gross profit as % of revenue, America ranks last while Japan tops all geographic segments

Operating Expense as % of Revenue

Apple has been spending more as % of Revenue on Research and Development.

Overall, it seems like a good quarter for the company with increase in revenue despite the drop in the iPhone segment. Services is on the rise and so is Wearables. Airpods Pro hit the stores yesterday and I have seen plenty of positive coverage

It’s a bit concerning that cost of sales increased this quarter, which I suspect is due to price cuts. It will be interesting to see how the upcoming quarters will be. The transition to Services and what the company has done have been positively received by Wall Streets

Disclaimer: I own Apple stocks in my personal portfolio

Leave a comment