As a student of business, I find Uber an interesting business. It is interesting because there are a lot of aspects that go into the operations of this ride sharing player, including geographical segments, different lines of business with different margins (Eats, Rides, Freights), add-on services to improve profitability (Rewards, Credit Card), exiting marketings where it is losing money and focusing on the ones where it is a dominant player, and different stakeholders (riders, drivers, restaurants, corporate customers and authorities).

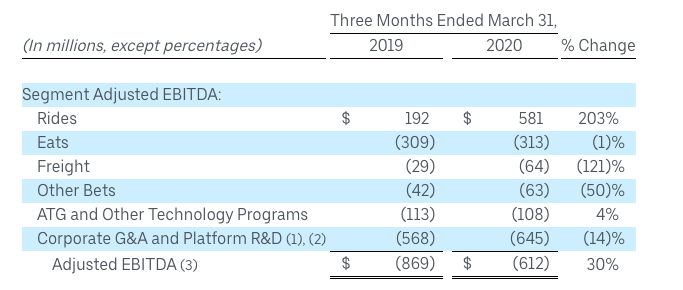

Like many other companies, Uber had its operations seriously disrupted by the Coronavirus. Rides bookings had a YoY growth of 20% in the first two months through February before plummeting to a decline of 40% and 80% in March and April respectively when the lockdown took hold. Eats, on the other hand, had a 54% YoY growth in bookings and 124% YoY increase in net revenue with take-rate of 11.3%, not too far from their long-term goal of 15%. Eats, for this quarter, remains the biggest loss-making segment, even though Freights’ loss growth is significantly bigger while Rides is still the only profitable business

Uber shed a bit of light on the effect that Covid-19 had on its business. Airports make up 15% of Rides bookings and 16% of its EBITDA. Obviously, when traffic to airports declined substantially, that significant chunk of business was gone. In terms of cities and countries, Uber provided the following

Last week, we saw 9% [indiscernible] growth and 12% gross bookings growth globally weak-on-weak. We believe the U.S. is of the bottom. U.S. gross bookings were up last week by 12% overall week-on-week, including New York City up 14%, San Francisco up 8%, Los Angeles up 10%, and Chicago up 11%. Perhaps more interestingly, gross bookings in large cities across Georgia and Texas, these are two states that have started opening up significantly, are up substantially from the bottom at 43% and 50%, respectively. Hong Kong is back to 70% of pre-crisis gross bookings levels.

Second, at a time when our Rides business is down significantly due to shelter-in-place, our Eats business is surging. We’ve seen an enormous acceleration in demand since mid-March, with 89% year-over-year gross bookings growth in April, excluding India.

Source: Uber’s Earnings Call

According to the quarterly filing, Eats bookings annual run-rate was about $18.8 billion. However, on the Earnings Call, the CEO said: “And just last week, Eats crossed the $25 billion gross bookings annual run rate”. If I understand that statement correctly, it meant that for the 3rd or 4th week of April, Eats bookings was around $480 million. Given that it reported the annual run-rate around $18,8 billion for the first three months through March, the increase to $25 billion only in April was extraordinary. Plus, Uber seemed to be confident that this level of growth in Eats would be sustainable, moving forward. So it’ll be interesting to see how it is 3 months later.

As for now, it’s an encouraging sign for Uber that their economies of scale seem to go in the right direction as revenue increased disproportionally compared to the driver incentives required.

Picking their battles

Uber commented on the recent exit of 8 Eats markets:

Uber Eats: On Monday, consistent with our long-term strategy, we announced a change to the geographic footprint of Uber Eats operations affecting 8 markets. We will discontinue Uber Eats in the Czech Republic, Egypt, Honduras, Romania, Saudi Arabia, Uruguay and Ukraine, and will transfer Uber Eats operations to our Careem subsidiary in the United Arab Emirates. The discontinued and transferred markets represented 1% of Eats Gross Bookings and 4% of Eats Adjusted EBITDA losses in Q1 2020.

Source: Uber

For what it’s worth, the management team deserved credits for exiting unprofitable markets, especially some that bled them dry such as China or Southeast Asia. In their presentation as of 31 Jan 2020, Uber presented their footprint map like this. Obviously, it’s better than being in more markets, yet with smaller presence

Some other interesting points

- As of Q4 2019, Uber for Business made up around 9% of Uber’s Rides bookings

- Uber reported in Q1 2020 that there were 31 million members of Uber Rewards Program. Given that they have 103 million monthly active users, that means out of 3 active users, one is a Rewards member. It’s promising and interesting especially because Rewards had been available in 5 markets only, with France recently added to the fold

- In Q4 2019, an average Rides trip was $9.5. Uber reported in the same period that an average Eats order was 50% bigger than a Rides order. That means an average Eats order in Q4 2019 was about $14.25

- “Eats insurance costs as a percentage of Gross Bookings are <1/5th that of Rides”

- Uber claimed that 46% of US national vehicle trips were less than 3 miles. It can be an opportunity for micro-mobility. However, it’s worth noting that scooter companies like Lime or Bird are notoriously not profitable. Lime recently saw its valuation plummet to around $510 million after previously being valued at $2.4 billion

- “Finally, we expect that shared Rides will be less important in the near-term. This was historically sweet spot for a primary competitor in the U.S. with around a 50% category position on shared Rides.”

- 23% of our Rides Gross Bookings from five metropolitan areas—Chicago, Los Angeles, New York City, and the San Francisco Bay Area in the United States; and London in the United Kingdom” – Source: Uber 2019 annual report

- In 2019, cash-paid trips accounted for approximately 11% of Uber Global Gross Bookings, about $7.5 billion.

Leave a comment