FICO

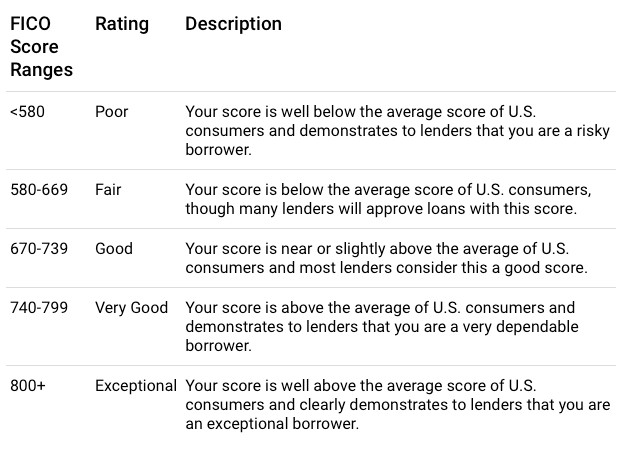

Most of the US consumers should be familiar with FICO. Credit score is a metric that tells lenders how likely you are going to pay back loans. The score is widely used by banks or lenders in the country for credit cards, mortgages and other types of loans. The most popular score is FICO and it’s developed by a company called Fair Isaac & Company. Take the initials of those three words and you arrive at FICO. Typically, FICO ranges from 300 to 850. The higher your FICO is, the more trustworthy you are in the eyes of lenders and hence the lower interest rates may be.

The current version FICO is FICO10, but there may be other clients that are still using legacy FICO9. According to FICO, the new score was developed off of FICO9 and offered significant benefits

We also announced some innovations in our Scores business, the release of the FICO Score 10 suite. The suite has 2 new scores. FICO Score 10 relies on credit bureau data and is consistent with previous FICO score versions that are in the market today. It reflects a normal model development cadence, extending features that were introduced in FICO Score 8 and FICO Score 9. FICO Score 10 is designed to be backward compatible with previous Score versions. FICO Score 10T incorporates a broader set of credit bureau data, including trended data, which captures unique aspects of the consumer’s financial profile over time. While the blueprint design is similar, it uses new characteristics to enhance predictive power. Both FICO Score 10 and FICO Score 10T demonstrate greater predictive power over all previous versions of the FICO score and were developed on recent data sets. By adopting the FICO Score 10 suite, a lender can reduce the number of defaults in its portfolio by as much as 10% among newly originated bank cards, 9% among newly originated auto loans compared to using FICO Score 9. The reduction in default is even higher for newly originated mortgage loans at 17% compared to the version of the FICO score used in that industry. These improvements in predictive power can help lenders safely avoid unexpected credit risk and better control default rates, while making more competitive credit offers to more consumers.

Source: FICO’s Q1 2020 Earnings Call

FICO is pretty popular among consumers and lenders. According to a presentation by FICO in 2019, 90% of the US credit lending decisions involved FICO scores and 90 out the largest 100 US lenders use FICO scores. 300 consumer accounts have access to free FICO scores

Fair Isaac & Company

In 1956, an engineer named Bill Fair and a mathematician named Earl Isaac founded a company together on the belief that data could improve business decisions, if used properly and wisely. They were ahead of their times, weren’t they? In 1992, FICO risk scores were made available to three major reporting agencies: Equifax, Experian and TransUnion. In 1995, Fannie Mae and Freddie Mac recommended the use of FICO in evaluating mortgage loans. (Source: FICO)

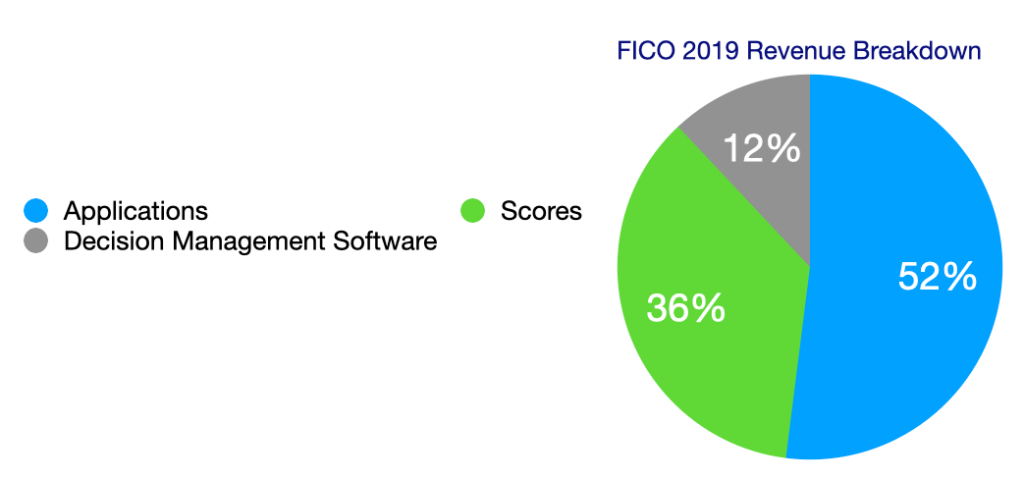

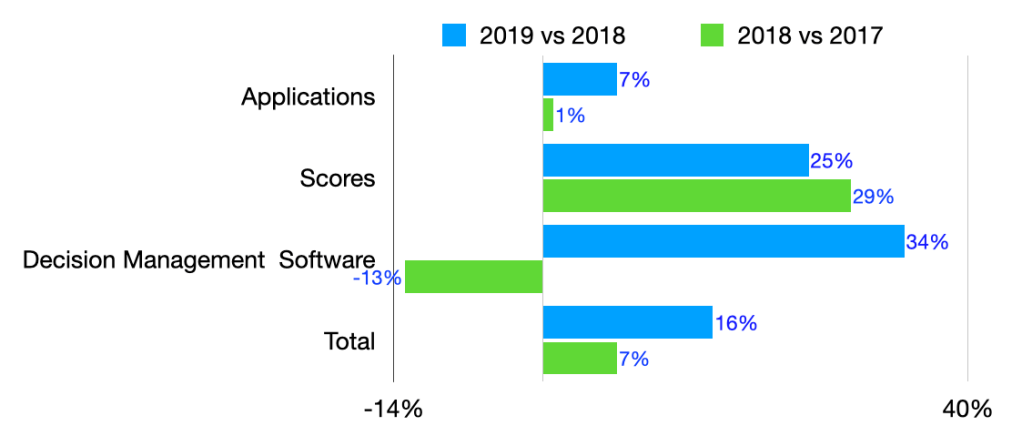

The company generates revenue from both consumers and corporate clients, but most of the pie comes from the latter. In addition to the popular scores, Fair Isaac & Company also offers other services such as Applications and Decision Management Software (DMS). While the names may indicate the same services, there is a major difference. Applications refer to FICO’s packaged software that meets specific-industry needs whereas DMS consists of tools that clients can use to build tailored apps that have the same function as applications. In 2019, Applications and DMS combined for 64% of FICO revenue (52% and 12% respectively) while Scores was responsible for the other 36%. In terms of YoY growth, the company recorded 16% growth in 2019, compared to 7% in 2018. Applications revenue was about $605 million, a 7% growth. Scores notched about $421 million in revenue, a 25% growth, while DMS brought home approximately $134 million, a 34% growth.

Under the three main segments, there are three sub-segments: transactional & maintenance, professional services and license. Transactional & Maintenance Bookings are on transaction basis. The more transactions there are, the more revenue FICO has. Professional services refers to “he estimated number of hours to complete a project multiplied by the rate per hour” while “Licenses are sold on a perpetual or term basis and bookings generally equal the fixed amount stated in the contract.”

The composition of the main segments differs from one to another. Transactional & Maintenance made up the most revenue for Scores in 2019 while Professional Services and License occupied 33% and 29% of DMS’s revenue. Growth behavior of each sub-segment under the main segments also varied. While license recorded the biggest expansion across all segments, Scores’ 2nd biggest growth came from Transactional & Maintenance and that of DMS came from Professional Services

| Applications | Scores | Decision Management Software | |

| Transactional & Maintenance | 6% | 25% | 8% |

| Professional services | -4% | 14% | 38% |

| License | 47% | 62% | 86% |

| Segment Total | 7% | 25% | 34% |

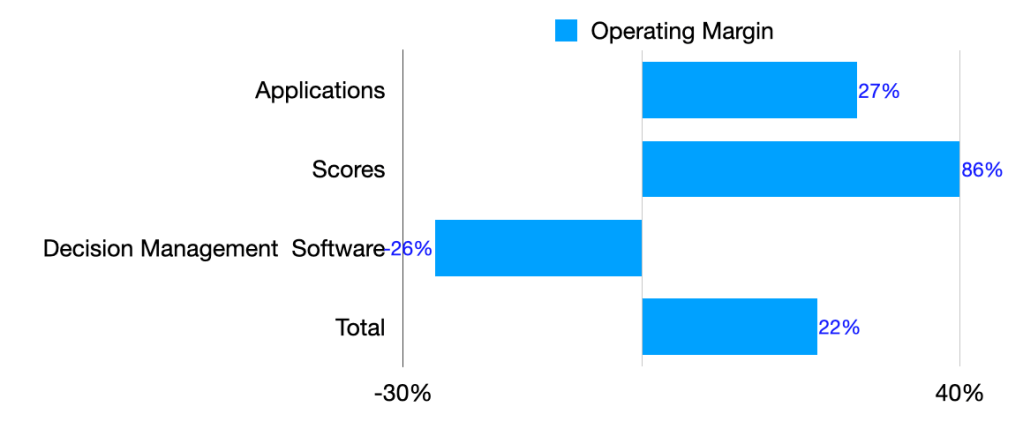

Although FICO doesn’t break down operating margin for the sub-segments, it does provide operating margin for the main business lines. Scores is the most profitable while DMS is the only unprofitable line. Looking at the composition of the lines, it’s not surprising that is the case. Transactional & Maintenance should have low marginal costs. FICO only generates more revenue and operating income as it signs up more clients and records more transactions. As Professional Services tend to have low gross margin due to high labor costs and Professional Services makes up a third of DMS’s revenue, it’s entirely possible that high SG&A and Sales & Marketing expenses sunk the segment’s profitability.

A few other notable stats:

- 34% of FICO revenue came from outside the US

- Banking industry is responsible for 87% of its 2019 revenue

- Commercial agreements with the three main reporting agencies made up 29% of FICO’s revenue (13% from Experian)

As a customer myself and somebody who works at a bank, FICO is instrumental in not only risk management, but also marketing. Given the popularity of the FICO risk scores and the proprietary nature of those scores, the company should be able to reap benefits for a foreseeable future. With regard to its solutions, FICO has some stiff competition and frankly, I have no idea how it will fare in the future. I like to get to know different types of business because that’s part of my investment effort and because I am just curious. I hope this post offers you a helpful primer on a company that is under-radar, yet plays a role in our life.

Leave a comment