Uber announced their Q2 2020 earnings today. Overall, the business was significantly affected by Covid-19. Net loss to the company was $1.8 billion while total bookings were down 35% YoY, and net revenue slumped by 33%. There were on average 55 million monthly active customers, down from 99 million in Q2 2019. The number of trips was down 56% YoY as well.

Zooming in at a deeper level, there are two starkly different stories concerning their Ride and Delivery businesses. Ride gross bookings were down by 75%, contributing to the 66% drop in Ride revenue. Nonetheless. the segment was still the only profitable one at Uber with $50 million in adjusted EBITDA. To get a sense of how Covid-19 affected their Ride business, here is a chart that the company provided in their latest presentation

Even with the rise in Eats gross bookings which I will touch upon later, the gross bookings overall were down significantly after 9th March 2020. According to Uber CEO, the company saw recovery in Asia and Europe. Bookings in New Zealand and Hong Kong even exceeded the pre-Covid level at times. Of course, it doesn’t help that the situation in the US where several of their key markets are located is still dragging out.

Uber Eats

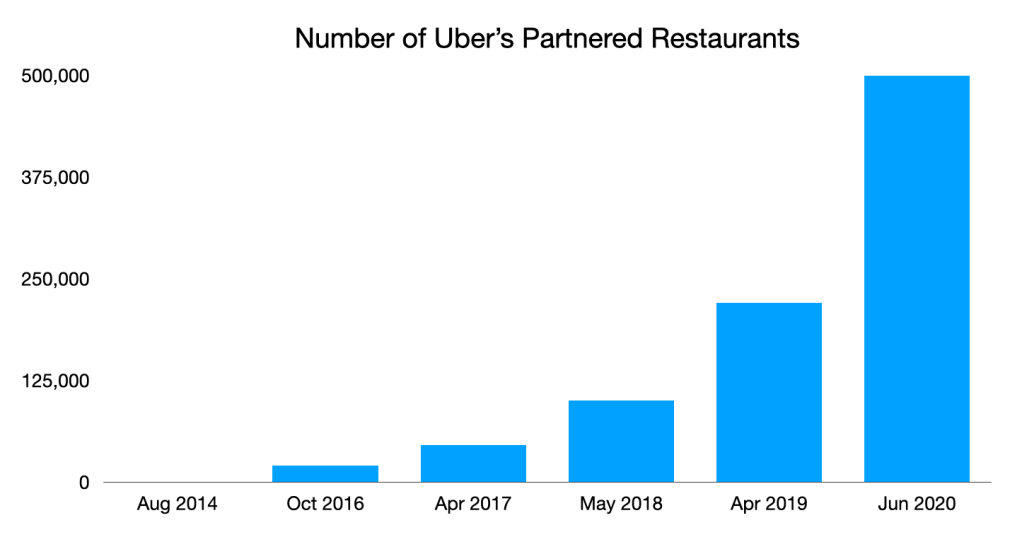

Gross bookings from Uber Eats grew by 106% in Q2 2020, resulting in 162% increase YoY in Eats net revenue. While the segment still recorded $232 million loss in EBITDA, it saw a 19% improvement to a year before. The segment now has over 500,000 partnered merchants on its platform. There are also more than 10,000 active merchants that offer grocery, convenience, prescriptions and pharmacy products. Uber reported 3 millions trips completed for Uber Connect since Mid April in 170 cities. Uber Connect allows consumers to send small packages.

Name change for segments

The company renamed their two main segments: Ride to Mobility and Eats to Delivery. The move signals a strategic shift in strategy. Mobility covers a lot more than just Ride. Uber doesn’t just want to provide a car ride to consumers. It wants to be associated with all kinds of mobility and transportation. There is already Uber helicopters. Uber has been trying to offer consumers public transportation options on their app as well.

With regard to Uber Delivery, I wrote about how Uber wants to move into the delivery service space with their acquisition of Postmates. Currently, there is also Uber Connect and a new service that allows delivery of groceries. Therefore, Delivery is a more apt name for the segment than just Eats.

If Uber’s ambition wasn’t clear before, it should be now.

Profitability

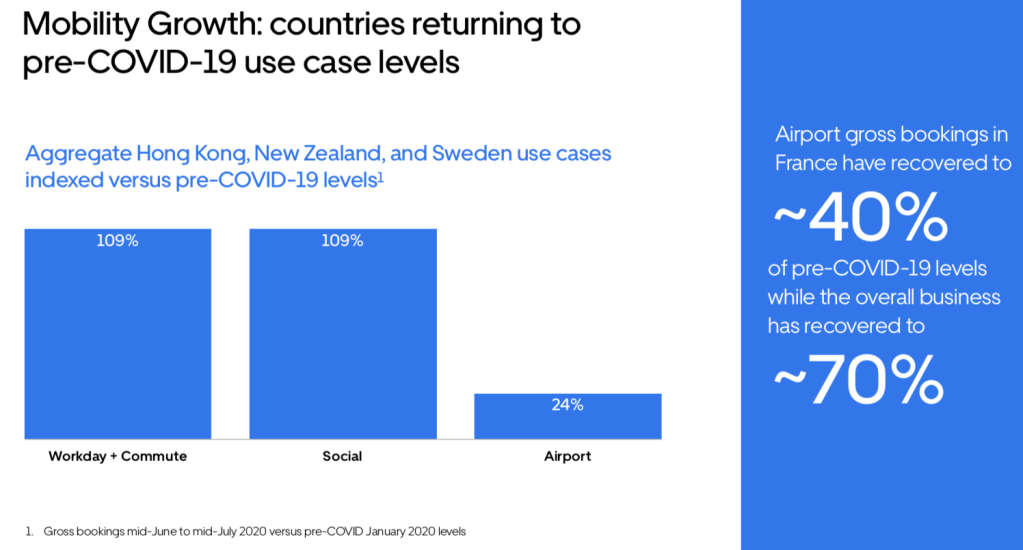

Personally, I think Uber’s struggle with their Mobility segment is just temporary. Once Covid-19 blows over or a vaccine is available, it will come back to what it was before, a revenue and profit machine for the company. Post Covid-19, as consumers are likely reluctant to use public transportation due to fear of being crammed in a closed space with strangers, there will be likely more demand for Uber’s ride hailing business. In fact, there is already some evidence to support the argument. Aggregate data from Hong Kong, New Zealand and Sweden markets showed some recovery on Mobility bookings compared to pre-Covid levels.

Additionally, even though Delivery has been highly unprofitable, Uber is pretty confident in its ability to achieve its long-term target. Here is what Uber CEO had to say on that:

Yes, Ross. As far as the debate goes, we stand firmly on the belief that pure-play delivery companies can and will be profitable. And we think it’s a pretty easy answer, but we don’t think that debate is worthwhile, so to speak. It’s only a question of when and it’s only a question of what question of when and it’s only a question of what those long-term margins will be. We have laid out a long-term margin profile of 15% of ANR and about 33% of EBITDA. We wouldn’t be doing it unless we felt confident there.

To be clear, Belgium is actually one of our smaller countries internationally, and we had said that we’re profitable in 2 of our top 5 international countries. And there are a number of other confident there. countries that that we are also profitable in, but we also wanted to make the point with investors that we’re profitable in countries that count. So it’s not just France and Belgium. It’s other countries.

But when we look from a structural basis or the margins of the business, you fast forward a couple of years now, we think we will be profitable in the vast majority of the countries in which we operate. If we’re not profitable, it’s specifically because we’re trying to achieve something strategically, whether it’s a growth target or we’re trying to expand the number of categories that we’re in, et cetera. So we land firmly on one side of the debate, and we have a lot of data internally and very very high confidence in the teams to win that debate.

Source: Uber Q2 2020 Earnings Call

Despite decimating Uber’s Mobility segment, Covid-19 has been a boost to its Delivery segment as it restricts trips outside of home. Driver incentives in Q2 2020 was only 27% of revenue, down significantly from 43% in Q2 2019. Furthermore, the grocery delivery space Uber is entering isn’t without fierce competitors. Behemoths like Amazon, Walmart or Target all invested in their grocery delivery services. When they announced the acquisition of Postmates, I wasn’t sold on their profitability in the short term. They proved me wrong when their net loss improved from $3 billion in Q1 2020 to $1.8 billion in Q2 2020. If and when Mobility segment returns to its full strength and if Uber can keep their momentum with Delivery, it will be even better for the company.

Bull case for Uber

Uber is now a household name. Years of hype and fast growth around the world while it was still a unicorn startup have made the brand very popular among consumers. It is a competitive advantage that poses challenges to any company that wants to enter the space. Plus, Uber’s global footprint gives it a leg up to those restricted to only one market. Even though a bigger footprint comes with a higher level of risk exposure, it does allow cross-market subsidies and more learning of consumers’ behavior. Uber has been conducting small tests in other markets before bringing new features to a bigger audience. In a business where consumer insight is so valuable, transfer of learning from one market to another is a luxury. To have the same luxury, Uber’s competitors would need to invest in multiple markets and be willing to take the same level of higher risks like Uber does.

Uber competes not only for consumers, but also for drivers. The company’s list of services available to drivers makes it a more attractive option than competitors. In my previous post, I wrote:

Furthermore, it can be a boon to drivers as well. To facilitate all the delivery services it wants, Uber needs drivers. Drivers have limited resources in the number of hours in a day and just one vehicle to drive. Hence, they will prefer working with a partner who can help them maximize revenue as much as possible. With a variety of delivery opportunities, Uber can sell drivers on that promise. In the future where Uber does indeed become an on-demand delivery platform, if a driver is without a Ride customer, he or she can either deliver food, grocery or basically an item ordered by another customer. Minimizing dead time and maximizing income can be an attractive value proposition to drivers.

To compete for drivers with Uber, any new rival would need to offer the same earning opportunities, in the form of either different services or a huge incentive. And that would require a lot of capital and years of investment.

With a variety of services thrown at consumers, Uber wants to establish a connection and relationship with users by being front and center in their lives, whether it’s ordering a ride, wanting to get some food from a restaurant, looking up a public transportation schedule, sending stuff to loved ones or fetching groceries. Once a connection is established, it will be a massive challenge for its competitors to overcome.

All Uber has been doing is to build its innovation stack. The more layers of the stack there are, the bigger their competitive moat is. However, execution is key, especially when it keeps moving the goal post in terms of profitability timeline and amid cash flow pressure.

Leave a comment