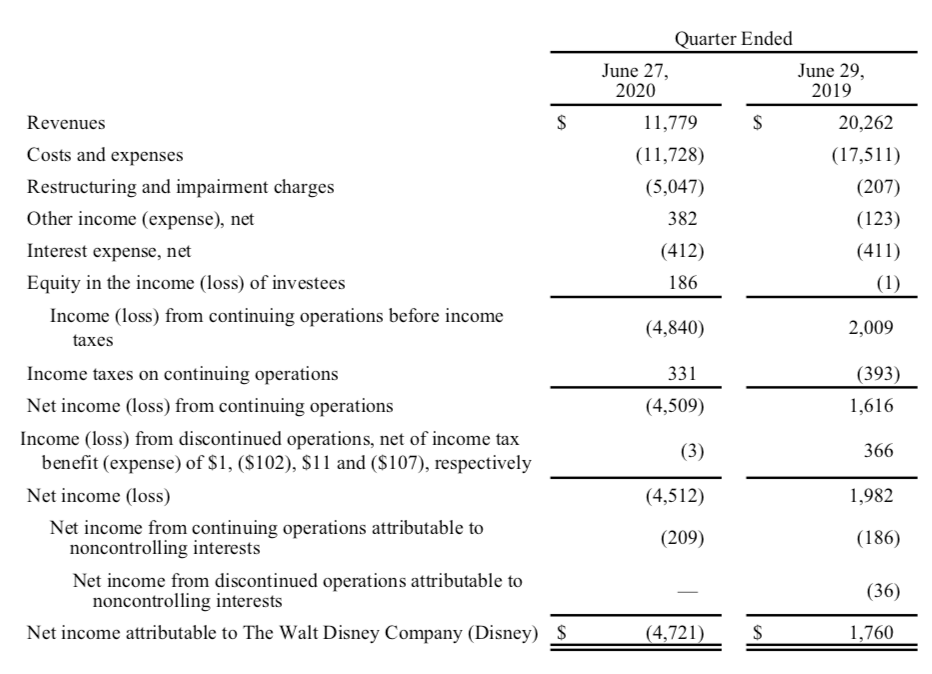

In Q3 2020, Disney reported a drop in revenue of more than 8$ billion, down 42% YoY due to the negative impacts from the Coronavirus. Most of the revenue loss came from Parks, which is historically a reliable source of revenue and profit for Disney. In the most recent quarter, Parks brought in a little less than $1 billion in revenue, compared to $6.6 billion in the same quarter last year. As a consequence, Parks recorded a loss of approximately $2 billion, compared to $1.8 billion in profit in Q3 2019. Despite the challenges that Covid-19 brought onto Disney’s operations, the company actually had a small profit from its operations, if you exclude the $5 billion in impairments.

Disney reported that as of 27th June 2020, there were more than 100 million paid subscribers on their platforms, including 8.5 million for ESPN+ (up from 2.4 million from a year ago), 35.5 million for Hulu (up from 27.9 million from a year ago) and 57.5 million for Disney+. On the earnings call on 4th August 2020, Disney’s CEO revealed that the subscriber base for Disney+ rose from 57.5 million 5 weeks ago to 60.5 million. The updated figure means that Disney already surpassed its lower target for 2024, a full four years ahead of schedule. While it’s definitely a good sign, it can be argued that Disney is usually conservative in its forecast and that Covid-19 has been an unexpected boost to its streaming service. It’s also worth pointing out that Disney+ Hotstar, launched in India only up to Q3 2020, made up 25% of Disney+ subscriber base at the end of the quarter.

A major announcement regarding content for Disney+ is the upcoming rollout of Mulan. Disney will make the movie available to Disney+ subscribers at an additional price of $30, meaning that you first have to have an active subscription and pay another $30 on top of it as a one-time fee to see the movie.

This one-off strategy is an interesting move in my opinion. Due to the impacts of Covid-19, Mulan’s schedule premiere has been postponed a couple of times. As the US is still struggling to handle this pandemic, folks won’t visit cinemas any time soon. Hence, Disney either would have to keep delaying the movie’s debut or put it on its streaming service. If the latter is the better option, what is the reason for the additional charge?

Bob Chapek, the CEO of Disney, labeled this move as a test and I tend to agree with him. There are three likely reasons behind Disney’s decision:

- The company wants to see how much a movie like Mulan can attract new subscribers or entice existing ones to pay more. Making it free on Disney+ is an easy and straightforward decision. Why not using this as a test and getting more revenue, given the situation that we’re in right now?

- A subscription can be shared with 5-6 people and as we still stay at home most of the time, it’s likely that a movie that charges $30 will be watched by more than one person. Disney is probably testing to see how the $30 price point is accepted by consumers. I mean, if 4 people watch the movie with a new subscription, that’s roughly $10 for each person, almost a movie ticket and they can still have access to Disney’s library for a month. Another point is that consumers are likely to react more positively to a price drop than to a price hike. If $30 is too high and Disney wants to repeat this test in the future at $20, it will likely be better than increasing the test price from $20 to $30.

- One can argue that Disney is angling for a future permanent one-off strategy as in the one-time charge will give subscribers exclusive early access to blockbusters. However, there are a couple of challenges with that. The first is that Disney has to convince subscribers to pay extra for every blockbuster. A movie such as Endgame may have the drawing appeal, but not every movie will be like that. The second challenge is how Disney would work with theaters once Covid-19 blows over. If Disney’s finest could only be found exclusively on Disney+, what would draw in moviegoers? Movie distribution brings in a significant sum of revenue for Disney. Hence, the company may likely have to deal with this question mark if it decides to pursue a one-off strategy.

In the near future, Disney will be one of the companies wishing for things to go back to normal as quickly as possible. Their streaming service should be fine. They have a lot of geographical footprint to grow into, boosted by a formidable library content, legendary marketing prowess and a household brand name. What they really want to add is feet inside theaters and the walls of their branded parks, hotels or resorts. That’s why they opened up parks in the US to some extent despite the Covid-19 warnings; which I fervently disagreed with. Given how the situation has progressed for the past few weeks, I won’t be surprised that it will take them at least a couple of quarters to regain the Parks business. Nonetheless, the business has shown resilience and I think the bull case for them is stronger than a bear case.

Disclaimer: I own Disney stocks in my portfolio.

Leave a comment