What is this company about?

Every business needs data to be competitive nowadays. The challenges related to data are daunting. First, data grows exponentially every day. Companies need to invest and maintain the right infrastructure to store a large amount of data. Second, the data infrastructure needs to support the business use cases. It must enable data staff to access data quickly and efficiently in order to build data-driven applications as well as carry out data analytics. As business leaders have to make quick decisions as a response to changing environments, it requires fast and accurate analytics.

For instance, I work at a bank and at the beginning of the pandemic, we needed to build monitoring dashboards quickly so that the management team could make quick decisions and have a finger on the pulse of the business. It was a challenge because our data warehouse’s structure made it so time-consuming to complete complex queries. And when multiple users tried to execute queries at the same time, the problem was exacerbated. I often had to work late at night to make sure my queries could finish faster. Our bank is just a regional one. I imagine that our data problems would be magnified if we had a bigger operation.

Snowflake is built to solve data problems. It offers cloud-based data storage and analytics services through which businesses can have a single truth of data, consistency, resiliency, flexibility and fast access to data. Snowflake products work on major public cloud providers such as AWS, Azure or GCP. On top of Snowflake, companies can build out a proper data warehouse, enable data analytics, power data applications and facilitate data exchange with other entities.

As a Software-as-a-Service, Snowflake allows customers to pay only for the resources and services they use. Since Snowflake relies on public cloud providers, their unit price mirrors that of such providers as in that prices change depending on which region you are located. Snowflake’s customer base is impressive. They count as clients corporations such as Akamai, Capital One, Neiman Marcus, AXA, McKesson, Hubspot. In terms of technology partners, Snowflake’s website lists 17 major partners, including GCP, AWS, Azure, Salesforce and Looker.

How has the company been doing?

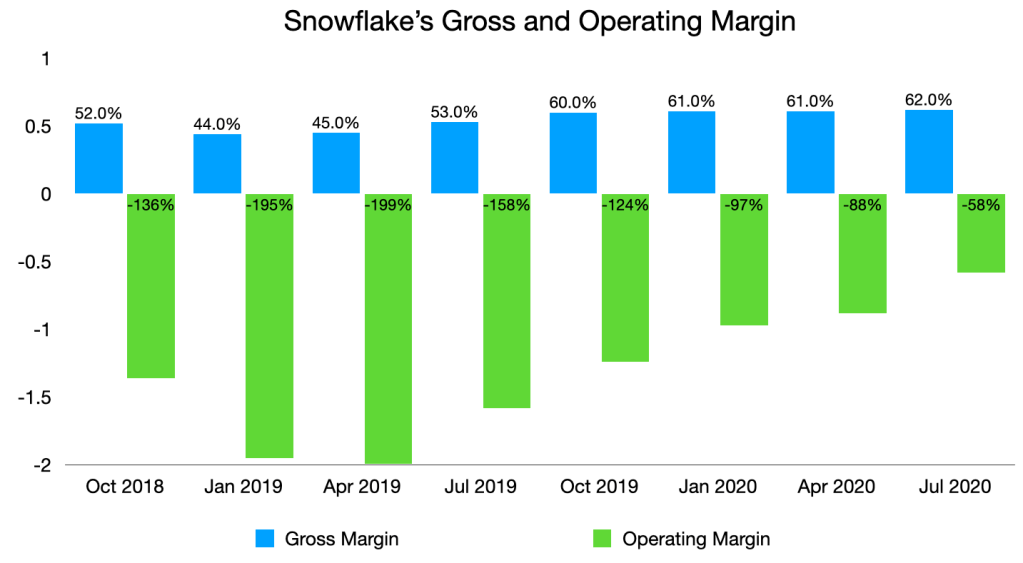

In S-1, Snowflake revealed its financials all the way back to the quarter ending in October 2018. The company hasn’t been operationally profitable as it recorded losses in every quarter. Revenue increased from $29 million in October 2018 to $133 million in July 2020. Operating loss stood at $78 million in July 2020. Before Jan 2020, Snowflake’s operating loss was even bigger than its revenue every quarter, but since then the loss has gone down while revenue has accelerated.

While the company hasn’t been profitable, the good news is that its gross and operating margin have been improving. If the company can continue to keep its gross margin and increase operating leverage (spend less on acquiring customers & be more efficient), it’s slated to be profitable in the near future. The sign is already there. 94% of the company’s revenue in 6 months ending July 2020 was from existing customers that expanded their usage. That implied a customer stickiness, satisfaction with the products and cost savings in acquiring new customers to increase the top line.

The past 12 months were positive for Snowflake. The company doubled its customer base from 1,547 in July 2019 to 3,117 in July 2020, as well as the number of customers whose trailing 12-month product revenue was greater than $1 million increased from 22 to 56 in the same time frame. Remaining Performance Obligation (RPO), which is a performance metric that includes unrecognized revenue in the near future, grew from $221 million in July 2019 to $688 million a year later. Net revenue retention rate has been always higher than 150%, with the latest quarter seeing 158%. Snowflake expects this rate to decrease in the near future.

Regarding platform usage and customer acquisition, Snowflake has been fairly impressive. Its platforms are used by 7 of the top Fortune 10 (4% of revenue in July 2020) and 146 of the top Fortune 500 (26% of total revenue). In the month of July 2020, the company reported an average of 507 million daily queries, compared to 254 million daily queries in July 2019. Net Promoter Score (NPS), a metric that indicates how willing a customer is to promote a brand, stands at a very good 71.

Capital One is an important client for Snowflake. The bank made up 17% ($16 mil) and 11% ($29 mil) of Snowflake’s annual revenue in fiscal year ending Jan 2019 and Jan 2020, respectively. While its share of revenue was less than 10% in the quarter ending July 2020, it still made up 22% of Snowflake’s account receivables ($33 mil). The trend lowers risks for Snowflake and investors as the company is now less reliant on this one particular customer.

What are the tailwinds behind Snowflake?

In its S-1, Snowflake reported a Total Addressable Market of $137 billion for the company as of 2020. Given the annual run rate of just $520 million in revenue, Snowflake has a lot of room to grow in the future. Furthermore, 12% of the company’s revenue came from customers outside the US. That indicates a big opportunity internationally for Snowflake. Since the company is built on top of public cloud providers whose infrastructure spans the globe, it already has the base infrastructure to expand internationally.

More importantly, the digital transformation that is underway in the corporation world is positive for Snowflake. As companies become more agile and digital, they need data to make informed decisions and be competitive. Hence, products and solutions that live in the cloud like Snowflake’s are well-positioned to capture this trend. From a personal perspective, my company is still hosting data on legacy infrastructures which present a bottleneck to our data analytics and operations. I can’t tell you how many times I had hours off as our data warehouse went offline. I can’t count how many hours I wasted because it took too long for complex queries to run. My developer colleagues reported happiness with the upcoming transition to Snowflake. Hence, this gives me a bit of confidence in the company as I know that my employer isn’t the only one running on legacy data infrastructure.

Risks

Among the risk factors listed in its S-1, there is one that I think stands out for Snowflake: its reliance on public clouds. Here is what it wrote:

We currently only offer our platform on the public clouds provided by AWS, Azure, and GCP, which are also some of our primary competitors. Currently, a substantial majority of our business is run on the AWS public cloud. There is risk that one or more of these public cloud providers could use their respective control of their public clouds to embed innovations or privileged interoperating capabilities in competing products, bundle competing products, provide us unfavorable pricing, leverage its public cloud customer relationships to exclude us from opportunities, and treat us and our customers differently with respect to terms and conditions or regulatory requirements than it would treat its similarly situated customers. Further, they have the resources to acquire or partner with existing and emerging providers of competing technology and thereby accelerate adoption of those competing technologies. All of the foregoing could make it difficult or impossible for us to provide products and services that compete favorably with those of the public cloud providers.

Source: Snowflake’s S-1

This is really a genuine concern. I don’t see Snowflake will build out its own underlying infrastructure in the near future. Mirroring the scale and sophistication of these public providers, especially if they want to expand overseas, will be expensive and resource-consuming. While such a reliance presents a risk, particularly when all AWS, Azure and GCP have competing products with Snowflake, the company also brings a lot of revenue to these cloud providers. So it creates an interesting dynamic in which I also suspect the Big Three will do anything to harm its startup customer.

In summary, my personal experience gears me towards investing in this company. I also observed some folks lauding the business on Twitter. The company itself has seen impressive growth and has a lot of room to grow as well as tailwinds. I personally look forward to the IPO debut of Snowflake.

Leave a comment