DoorDash is a food delivery service which, after receiving an order, will deliver the order to the customer’s door. The service has three main stakeholders: merchants (restaurants), customers who order food and delivery partners whom DoorDash call “Dashers”. The business started in 2013 as three Asian Americans wanted to help local restaurants. The CEO, Tony Xu, migrated to the US at the age of 5 and worked in his mom’s kitchen in his earlier years. It is that background that inspired him to start this business. 7 years later, these entrepreneurs and their team are about to reap the fruits of their labor after the business has grown leaps and bounds and is on the verge of going public. Let’s take a look at how DoorDash makes money

How DoorDash makes money

This is the graphic DoorDash included in its S-1 to explain where its revenue comes from

As you can see, DoorDash generates its revenue from charging customers fees which include typically include delivery and service fees, as well as taking a cut from the merchant side. In 2018, DoorDash introduced DashPass, a subscription that is worth $9.99/month. The subscription will remove per-order delivery fees and reduce service fees for customers. At the same time, DoorDash hopes this subscription will help increase the stickiness of the service and keep the customer churn low.

DoorDash has gone a long way and become increasingly…less unprofitable

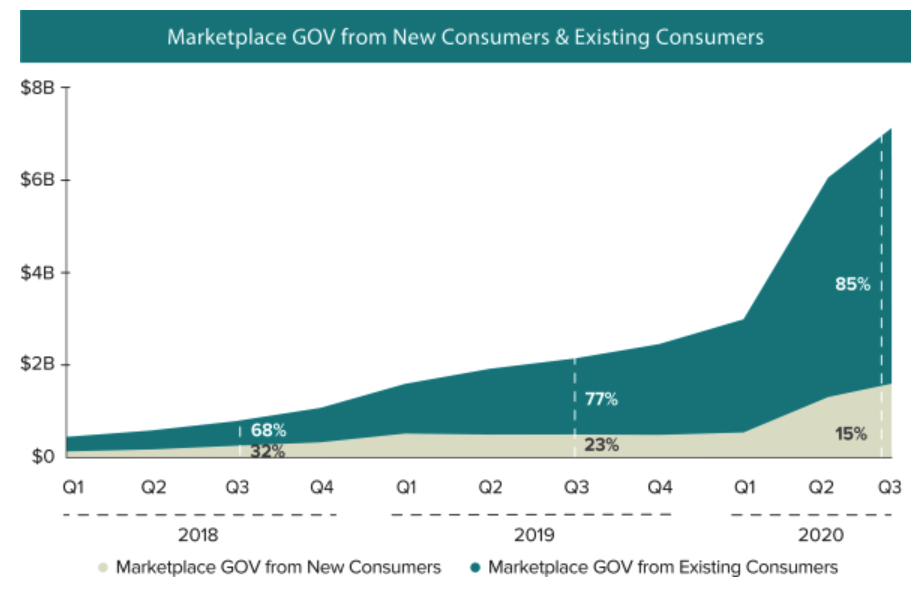

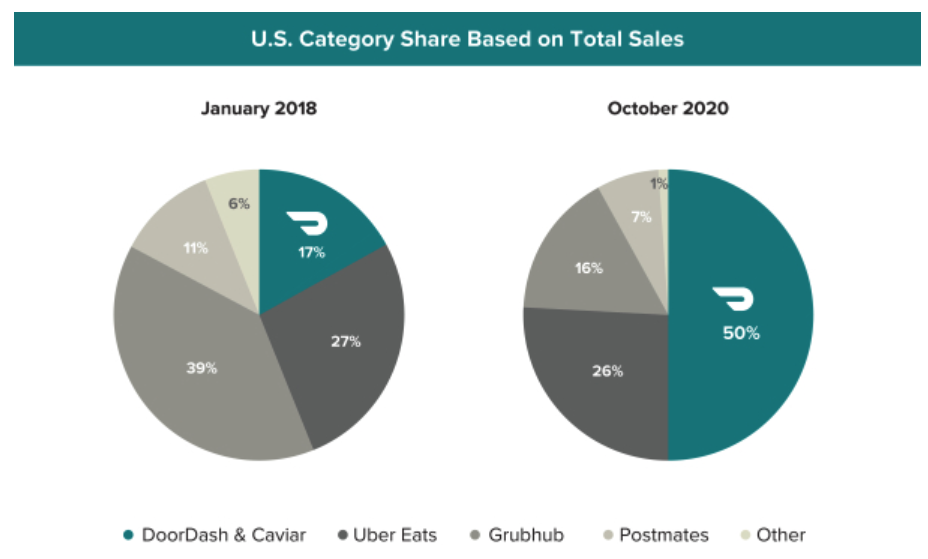

According to its S-1 filing, DoorDash grew its market share from 17% in January 2017 to a market-leading 50% in the US in October 2020, besting other contenders such as Uber Eats, Grub Hub and Postmates. Compared to the same period last year, DoorDash tripled its order count and the Marketplace Gross Order Value (dollar amount of all orders) in the quarter ended September 2020. In Q3 2020, the delivery company generated more than $7.2 billion in GOV and received 236 million in total orders. In the last two years, an average order on DoorDash has stayed largely consistent at $30. Since these numbers were recorded after the introduction of DashPass, I wonder what has been the effect of the subscription on the average ticket.

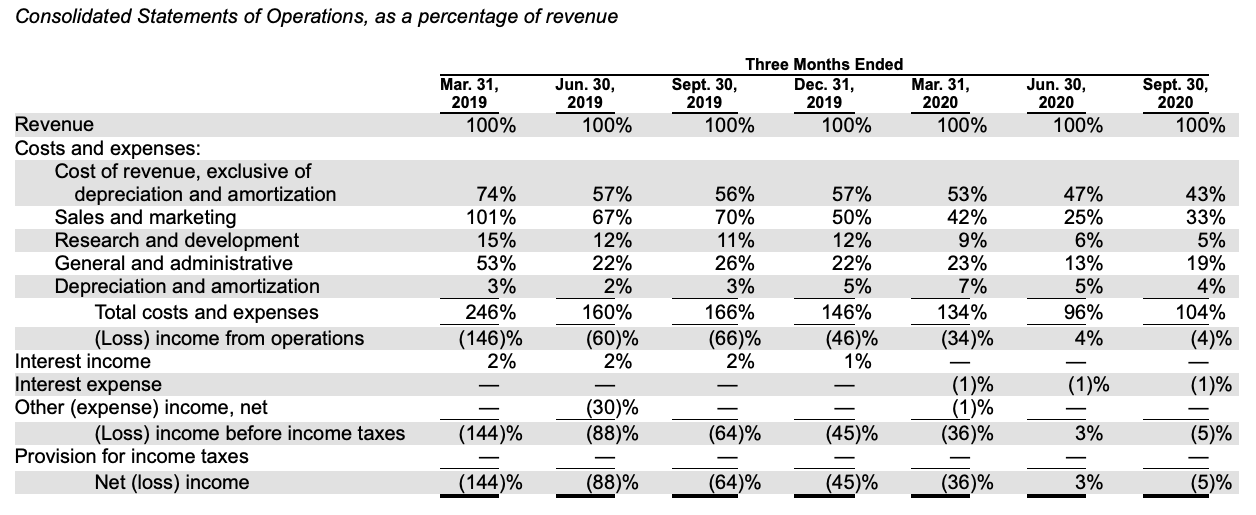

The company grew not only on the top line, but also on the profitability side. Gross margin has steadily increased from 23% in Q1 2019 to a sweet 53% in Q3 2020. Contribution margin, which represents the result when you divide the difference between revenue and variable costs by revenue, went up from -74% in Q1 2019 to 24% in Q3 2020. In other words, for each order, DoorDash didn’t had to spend as much on acquisition and promotion as it had had. In fact, DoorDash reported that existing customers on the platform have increasingly made up the majority of the business, reaching an overwhelming 85% of the total GOV. This is a very good sign for DoorDash as it shows customers love what they sell and stick around more. In business, we often say it costs 5-6 times more to acquire a new customer than to retain one.

While its competitor Uber Eats never sniffs profitability, DoorDash achieved the feat in Q2 2020. While its revenue grew almost 7 times between Q1 2019 and Q3 2020, DoorDash’s operating loss has shrunk 6 times during the same period. To highlight the increased efficiency of the business, Sales & Marketing, which is usually the biggest expense for a multi-sided platform like DoorDash, has been lower than Cost of Revenue for 4 straight quarters through Q3 2020 and stood at 33% in the lastest quarter.

As the business grows, so does DoorDash’s legal trouble. The company spent a few pages only on legal lawsuits, most of which concern its labeling Dashers as independent contractors, instead of full-time employees. The company repeatedly warns investors in its filing about regulations which could adversely harm its business. That’s because if DoorDash has to change its classification, it would mean the company has to pay higher wages and employee benefits. California introduced AB5, a legislation that would force gig economy companies like DoorDash to alter its operating model and classify workers as employees. However, DoorDash got a victory when Californians passed Proposition 22, which essentially stayed AB5. However, I don’t think the legal challenges will end there for DoorDash and they are something that prospective investors should pay attention to.

My thoughts on DoorDash

Clearly, things have been going well for DoorDash. The past few months have seen a substantially positive impact by Covid on the business. More order, more business and higher odds at profitability. Even though DoorDash indicates that their customer base makes up only 6% of the US population, I am pretty doubtful whenever companies cite the Total Addressable Market. First of all, not all the US population will use DoorDash. Second of all, the company has fierce competition from the likes of Uber Eats, Postmates and Grub Hub. I am confident that DoorDash will grow its top line in the next year or two, but the magnitude that the company hints in its filing is not really realistic. On the other hand, DoorDash can grow internationally. The company recently debuted in Canada and Australia. There is no doubt it will make inroads into Uber Eats’ market share, but at the same time it will require more resources from the management.

Recently, we have seen DoorDash strike partnerships that are not food related such as the one with Walgreens to deliver drugs and health products. In the future, I expect to see DoorDash develop to be a delivery platform, not just a food delivery machine. The logic is simple: the more orders there are, the more revenue DoorDash can generate and the happier it can keep customers and drivers. I didn’t see this piece much from the filing, but don’t be surprised if it comes up more in the next couple of years.

Additionally, some people wonder the sustainability of this model as restaurants have to relinquish a significant amount of margin to DoorDash. In the example above, restaurants have to give up 18% ($4 out of 22%) to the delivery service, while it was reported that in some case, the commission could go up to 30%. While it is indeed concerning as some restaurants may resist working with DoorDash and lawmakers may intervene, the fact and the matter is that a commission rate of 15%-20% seems to be the industry standard. Plus, restaurants may find that developing their own delivery muscle and marketing ability won’t be that much cheaper. As we are going through the worst phase of this pandemic so far and the weather is getting colder and colder, diners may favor delivery to in-dining, a huge tailwind for DoorDash.

Some interesting facts from DoorDash’s S-1

- Dashers’ age ranges from 18 to 55. 45% of Dashers are women

- As of September 30, 2020, there are 5 million DashPass subscribers

- DoorDash has 390,000 merchants, 18 million customers and 1 million Dashers on its platform

- “In 2019 alone, merchants as a whole experienced 59% year-over-year same store sales growth”

- DoorDash’s list of 3rd party partners include AWS, Stripe, Salesforce, Twilio, Wavefront, Snowflake, Olo, Salesforce, Twilio, Wavefront, Snowflake, Olo and Google Maps

Leave a comment