“Buy Now Pay Later” (BNPL) lets consumers break down purchases into smaller installments, either for free or with a charge. Sounds familiar? BNPL isn’t a new concept. Your credit card is essentially the OG of BNPL. When you put a big purchase (like a mattress or a new smart TV) on your credit card, you can spread out the outstanding balance into smaller chunks over a few months. If you make prompt payments every cycle, there will be no finance charge or late fees. Otherwise, you’ll incur penalties which can be fairly expensive as credit cards’ APR is usually in the high teens or the 20s.

What is the difference between BNPL and credit cards then? While credit cards can be convenient, securing approval isn’t always easy, especially for low FICO customers. Even though possession of a credit card can boost one’s FICO in the long term, upon an application for a new card, consumers will likely receive a hard FICO pull which hurts their standing in the short term; the price that some customers are reluctant to pay. Furthermore, it can take a couple of weeks for consumers to receive their plastics. With BNPL, consumers can receive a decision from BNPL online in a few minutes and there is only a soft FICO pull that doesn’t hurt their credit standing in the short term. As Covid-19 forced businesses to move from brick-and-mortar to online and it placed significant financial constraints on consumers, it created a perfect environment for BNPL to thrive.

Who are the main players and what do they offer?

- Afterpay is among the biggest BNPL lenders in the US. Hailing from Australia, the company only entered the US market in 2018. Remarkably, the US has quickly become the biggest contribution to the company’s revenue in only 3 years. Afterpay doesn’t charge interest. Consumers make the down payment at the time of the purchase and have to pay off balance in 6 weeks (a payment every 2 weeks) to avoid late fees.

- Klarna is a Swedish startup that offers payment and financial services, including BNPL. It entered the US market in 2015. Klarna allows consumers to make interest-free installments within 30 days or 6 weeks. It also offers high-interest financing options that spread out payments in a longer term.

- US consumers should be very familiar with Paypal. The company launched its BNPL offering last August. Paypal’s BNPL is similar to Afterpay’s, allowing consumers to break down purchases into 4 interest-free installments.

- Affirm was founded by ex Paypal, Max Levchin in 2012. Its model is slightly different from other BNPL lenders’ in a sense that Affirm doesn’t charge consumers usage or late fees. Payment options include monthly interest-free installments in 3 months or installments with interest over a longer period.

These startups have played an important role in popularizing BNPL. Now, banks joined the party. Amex launched its BNPL a couple of years ago, but on a fairly limited basis. Since then, it has opened it up to more customers. Chase also introduced its own version called “My Chase Plan”. These banks let consumers make interest-free installments with a monthly fee equal to a percentage of the purchase’s amount. This gives borrowers incentive to pay off their balance as soon as possible, because the longer the plan is, the more fee they will have to pay. Amex even lets its customers combine multiple purchases into one BNPL plan. Unlike startup BNPL providers, these banks impose a minimum requirement of $100 per purchase, along with other criteria, to ensure that customers aren’t overextended.

| Interest | Installment Frequency | Fee to use BNPL | Late fees | |

| After Pay | 0% | Every 2 weeks | None | Yes |

| Affirm | 0% – 30% | Monthly, up to 12 months | None | None |

| Amex | 0% | Every month | % of each eligible plan’s total amount. | Yes |

| Chase | 0% | Every month between 3-18 months | % of each eligible plan’s total amount. | Yes |

| Klarna | 0% – 19.99% | Every 2 weeks or in 30 days for 0%Every month up to 36 months with APR | None | Yes |

| Paypal | 0% | Every 2 weeks | None | Yes |

| Quadpay | 0% | Every 2 weeks | None | Yes |

| Amex | Chase | |

| How many plans can an account have? | 10 active plans at a time | 10 active or pending plans at a time |

| Minimum purchase requirement | $100 | $100 |

| Penalties for paying off plans early | No | No |

| Rewards on BNPL purchases | Yes | Yes |

| Are refunds/returns automatically applied to an account’s balance? | No, customers must call the issuer | No, customers must call the issuer |

| Can authorized users set up plans? | Only card owners or Authorized Account Managers with Full Access can set up a plan | Only card owners can set up a plan |

What do merchants and consumers get from BNPL?

For shoppers, BNPL lets them spread out a big purchase into smaller interest-free installments quickly and without a credit card. As mentioned above, the convenience and speed that BNPL brings are even more attractive during Covid-19, especially to younger shoppers who may not build their credit yet or may not have a credit card. Klarna and Afterpay claimed that 90% of their transactions were with debit cards, and 72% of those customers had enough balance on their checking account to cover 2-5x the purchase amount. To lock in customers, BNPL providers such as Klarna and Afterpay launched loyalty programs respectively with additional benefits for their most engaged customers. Klarna’s rewards program Vibe was launched first in the US in June 2020. The no-fee program allows customers to earn 1 point for every dollar spent. The points can be later redeemed for gift cards. Klarna reported that the program exceeded more than 1 million members. On the other hand, Afterpay’s loyalty program Pulse offers a different set of benefits. Registered members in the program can opt to pay nothing up front, choose to reschedule up to 6 payment dates and buy Afterpay gift cards. With Amex and Chase, shoppers accrue points to their bank rewards accounts and can be redeemed later.

However, there are risks for consumers when using BNPL services. A study found that many shoppers incurred late fees, not because they couldn’t make payments financially, but because they lost track of their payment schedule. While this prospect is real, BNPL providers are taking steps to make it easier for shoppers to pay on time. Klarna lets customers set up automatic payments and send out notifications. In the long term, it will be better for BNPL providers to rely too much on late fees. The second risk lies in the consumer protection or lack thereof and the difficulty when it comes to refunds/returns. Credit card issuers have to stop payments when they are disputed. With other BNPL providers, consumers first have to contact sellers, get credit and then proceed to the next steps with the lenders and the outcome is less guaranteed.

From a merchant’s perspective, BNPL brings more customers as the service providers spend a lot of money on marketing and user acquisition. Regardless of whether borrowers make payments on time, merchants get paid in full up front and they don’t have to bear the risk of chargebacks or fraud. In return, though, merchants have to relinquish a fee for each transaction to BNPL providers that can be multiple times higher than what they usually pay in interchange. Plus, merchants risk losing their relationship with customers. I wrote about the importance of owning your relation with your customers. If shoppers feel more attached to BNPL providers than merchants, in the same way shoppers feel more attached to Amazon than the sellers on Amazon’s website, merchants run a risk of losing bargaining power.

BNPL adoption

Because it brings flexibility in payments, BNPL became a hit with shoppers in 2020. Klarna reported that at the end of 2020, it had 14 million registered consumers, 3.5 million monthly active users and 60,000 downloads in December 2020 alone. As of Feb 2021, Affirm had about 4.5 million users that had at least one transaction in the last 12 months, up from 3 million users from one year prior, an increase of 50% YoY. Likewise, Afterpay had 8 million active users as of Feb 2021, up from 5.6 million in June 2020, and the US is now its biggest market. Paypal introduced its “Pay in 4” product in the US market in August 2020 and said that it was the company’s most successful launch ever.

The rise of BNPL also benefits merchants. In December 2020 alone, Klarna drove 22 million lead referrals to more than 6,000 US retailers. Reportedly, Sephora’s in-store and online orders through Klarna in the US saw an increase in average order value by 65% and 35% respectively. Additionally, Afterpay delivered 45 million lead referrals to its partners globally in December 2020. As the US is Afterpay’s biggest segment and the world’s biggest retail market, it likely made up more than half of those referrals. Over the last 12 months, Afterpay reported a 141% increase in the number of active merchants in the US, from 7,400 in Dec 2019 to almost 18,000 in Dec 2020. Furthermore, Affirmgrew its merchant network by 39% during the last 6 months of 2020, to almost 8,000.

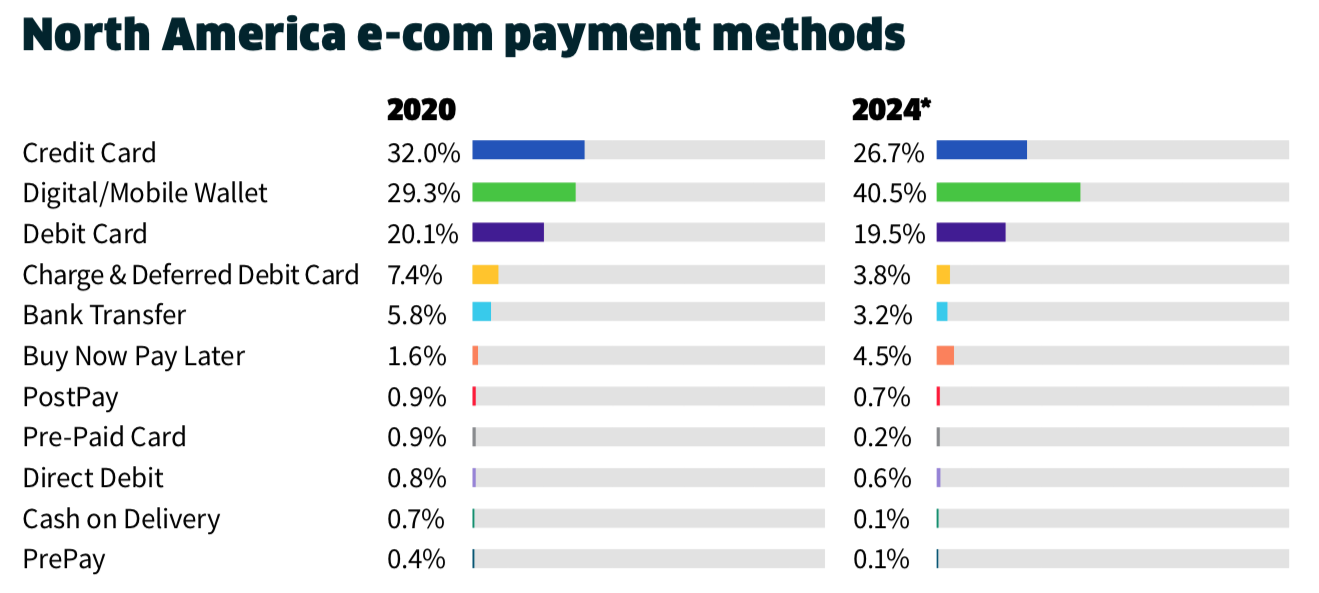

According to the latest Global Payment Reports by FIS, BNPL will make up 4.5% of North America’s eCommerce in 2024, up from 1.6% in 2020.

How do BNPL providers make money?

For providers that have an option to charge interest up front like Affirm, interest income can be a significant source of revenue. In fact, it’s Affirm’s second biggest revenue stream. Late fees can be another stream, though, as I already mentioned, they should constitute a small percentage of a provider’s income. Afterpay’s late fee only makes up 7% of the company’s revenue. Most of these providers make money from a fee that merchants have to pay them on every transaction. This fee helps BNPL providers offset the cost of fund placed on the balance allocated to shoppers, the interchange fee that these providers later have to pay to card issuers when shoppers make payments and operating expenses. As BNPL lenders become more popular, I suspect they will eventually launch advertising services whose revenue is high margin, compared to their current margin structure. For banks such as Amex and Chase, a minimum purchase requirement of $100+ means a higher interchange revenue. Plus, they charge customers a monthly fee to use their BNPL service. On the other hand, banks have to incur more expenses as they are much more regulated.

In short, BNPL is a trend born out of unaddressed needs of consumers and accelerated by a special market environment (Covid-19). It’s similar to something that once you saw, you can’t unsee. Once consumers experience it and come to like it, as evidenced by the rapid growth of BNPL providers, I don’t see how it will go away in the future. It will be interesting to see 1/ how these providers work to be more efficient, grow their machine learning capabilities so that they can minimize their losses, and acquire users and 2/ how lawmakers catch up to what’s going on in the market and what ramifications potentially new laws would bring.

Leave a comment