The story of Paypal started in 1998 when Max Levchin, Peter Thiel and Luke Nosek founded Confinity, a digital wallet company. They later merged Confinity with X.com, launched by Elon Musk, and altogether rebranded the new entity as Paypal. In 2002, the company went public under the ticket $PYPL. Later in the same year oof its IPO, it was acquired by eBay and became the prominent payment option on the famous marketplace. In 2015, Paypal left the eBay family to become a separate and independent entity. Six years later, it is now one of the most trusted brands in the world, available in more than 200 countries and valued at almost $300 billion.

At the core, Paypal provides payment and financial services to both consumers and merchants. Originally, it used to be one of the primary methods of person-to-person (P2P) transactions. Over the years, Paypal has transformed itself into a more expansive platform. Consumers can now use Paypal to send and receive money from others as well as to pay merchants, whether the transactions are online or in stores with debit cards, credit cards, tap to pay and QR Codes. On the merchant side, Paypal offers a host of solutions, including payment processing, marketing tools and financing options.

As a two-sided platform, Paypal needs one side to feed the other. From the consumer perspective, they only find Paypal useful when they have friends and families on Paypal network. Additionally, Paypal must be accepted at various merchants, whether transactions take place in physical stores or on websites. Otherwise, what would be the point of having a Paypal account? From the merchant perspective, Paypal’s value propositions lie in their payment solution and the brand name as well as trust cultivated with consumers. If consumers didn’t trust or use Paypal, there would be plenty of other alternatives. But that’s also one of their three moats. It’s super hard to be a two-sided platform because of the chicken-and-egg problem. Not only did Paypal have to solve that problem between consumers and merchants, but they also had to deal with it within the consumer space.

Another moat of Paypal is that the company has cultivated trust in consumers and merchants alike with its track record of security. Even though security breaches are almost inevitable to any company, so far Paypal hasn’t recorded too many incidents. When it comes to handling people’s money, security should be at the top of any company’s agenda. I mean, anyone can boast that they can exercise two hours in a row. I don’t doubt it. But it’s a completely different challenge to exercise two hours a day for 30 days in a row, let alone for years. To replicate such a track record, a competitor needs to invest in security and more importantly, it needs time. No matter what a newcomer says about its own security, only time can seed the trust in the constituents of its network. Unfortunately, time isn’t something that human brains or money can buy. And while a newcomer or existing player builds up its track record, Paypal is not likely to stand still. Just look at their M&A activities in the last few years: Venmo & Braintree (2013), Xoom (2015), iZettle (2018), Honey (2019), GoPay & Happy Returns (2021).

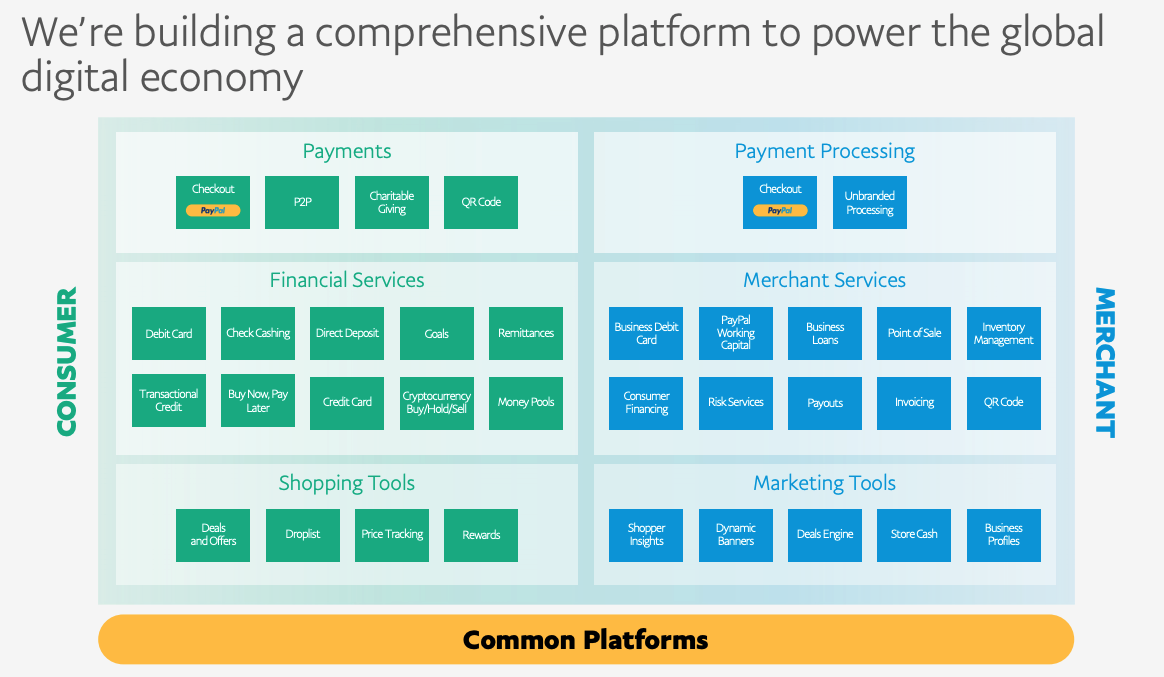

Finally, Paypal is operating at an enormous scale. In Q1 FY2021, it processed $285 billion in transactions, growing at 49% YoY. That annualizes to more than $1 trillion. As you may know, scale is the magic in business. Paypal’s gigantic scale should give the company a cost advantage over competitors. Plus, the breadth of Paypal offerings poses a daunting challenge to anyone wishing to match them. Just look at Figure 1 to see how many services are available, not to mention the acquisition of Happy Returns. It’s hard to spread resources and make investments on multiple fronts when you are on the back foot in terms of unit costs. Just to give you an example of what the scale of Paypal’s existing active account base and its brand name can do, let’s take a look at the rollout of Buy Now Pay Later and QR Code. Paypal introduced its Buy Now Pay Later only in August 2020. As of Q1 2021, its Pay in 4 already had over $2 billion in TPV globally, of which $1 billion came from the US. Pay in 4 also had 5 million unique customers. In addition to its popularity and reach, Paypal offers the service to merchants without charge. Normally, merchants have to pay BNPL providers several times the normal interchange, but Paypal is willing to subsidize merchants to gain market share. Also, the company enabled pay by QR Code some time in the latter half of 2020, but it already amassed 1 million merchants as of Q1 2021 that used the service, up from 500,000 two quarters prior.

How does Paypal make money?

We generate revenues from merchants primarily by charging fees for completing their payment transactions and other payment-related services.

We generate revenue from consumers on fees charged for foreign currency conversion, optional instant transfers from their PayPal or Venmo account to their debit card or bank account, interest and fees from our PayPal Credit products, and other miscellaneous fees.

Source: Paypal’s latest Annual Report

In short, Paypal charges merchants on every processed transaction and for other additional services. On the consumer side, P2P transactions don’t yield much revenue, but if consumers want to have instant deposits or have an outstanding unpaid balance on their credit cards with Paypal or Venmo, then the company earns additional fees and interest on the balance.

Take-rates which indicate what Paypal gets in revenue over the transaction volume depend on the kinds of transactions. Normally, bill payments and P2P transactions have low take-rates. Transactions funded using debit or credit cards are more expensive to process than those funded using bank accounts or balance within Paypal or Venmo. Commercial transactions such as those on eBay or cross-border transactions that require a foreign exchange are more lucrative. Obviously, Paypal would love to maximize revenue and profits, but there is necessarily a balancing act to be had here. Although bill payments and P2P have a low yield, they are sticky. They are what keeps users engaged and in the network. Payments is a highly contested industry. Any transactions processed by legacy banks, other providers such as Square or Apple Pay and fintechs are transactions that Paypal loses. Hence, I think for the time being, it’s better for the company’s future that they are prioritizing the growth of the active account base and engagement.

In short, I am bullish on Paypal. The company has a brand name known and trusted in many countries around the globe. It has the expertise after spending more than two decades in the industry and the ability to transform itself into a more expansive and competitive entity. It has a nice track record of acquiring other businesses to add needed capabilities. Currently, Paypal is the only Western company with 100% ownership of a Chinese payments company after it acquired 100% stake in GoPay. Additionally, it announced the acquisition of Happy Returns with the aim of offering merchants as well as shoppers convenient return services. As payments are pretty fragmented, I believe Paypal will not have any trouble from regulators with regard to future M&A. Yes, competition is plenty and stiff, but as you may already see at this point, there are reasons to like Paypal and what they are doing.

Disclosure: I have a position on Paypal.

Leave a comment