Clear Secure made its debut on the stock market this week at around $4.5 billion in valuation. I read its S-1 and wanted to talk about some of my notes.

What is Clear Secure about? In essence, the company is all about using biometrics for security. Think about how, in movies, people use retinas or fingerprints to unlock valuable assets in a vault or a safe. CLEAR gives customers access to services that they already paid for. With CLEAR, partners can be assured that customers are who they say they are and elevate the customer experience due to expedited verification process. On the other hand, instead of waiting for a long time in lines, customers can have a more pleasant experience with dedicated CLEAR kiosks, applications and lanes. Below is an example of how it works at airports.

CLEAR makes money from two sources: partners and end users. Partners that use CLEAR technology compensate the company based on the number of users or transactions. Even though there is no mention of a standardized contract structure in the prospectus, usage-based pricing means that once CLEAR is established, the more popular and used it is by end users, the more revenue the firm generates. In addition, CLEAR also makes money from CLEAR PLUS, its flagship subscription. With CLEAR PLUS, users can save time at airports by using dedicated CLEAR lanes to quickly verify their identity and travel credentials before entering the physical security check. CLEAR PLUS is priced at around $175/year and if you enroll at airports, you can get one month free trial. In January 2020, CLEAR announced that it was selected by TSA to handle both renewals and new subscriptions for TSA Check. As part of the agreement, CLEAR will be allowed to sell a bundled subscription for both TSA Check and CLEAR PLUS. While both services are essentially the same, TSA Check has a much wider coverage in the U.S. The program is expected to go live in the back half of 2021 and will be a new revenue source for CLEAR. Apart from the aforementioned services, CLEAR also offers end users free access to other services such as Home To Gate, Health Pass or CLEAR Pass for CBP Mobile Passport Control. These freebies serve as an acquisition channel for CLEAR, but the company reported that in-airports are still the most popular one.

CLEAR has plenty of room for growth. Its kiosks are available in major airports nationwide, but there are still a lot more to cover. The company said in the prospectus that its footprint as of the end of May 2021 only covers 57% of the TSA departure volume in 2019 while the total signups to CLEAR PLUS reached only 4% of the potential market. If you think about it, what CLEAR offers can be useful to companies in many verticals. Hospitals or healthcare firms can access confidential information quickly without a slew of forms. Hospitality players can check in and out guests more quickly with CLEAR. Sports events can handle the inflow and outflow of spectators more efficiently. Plus, CLEAR is available only in the U.S now. Right now, CLEAR already has a commercial agreement with Wal-mart, MLB, NBA, Delta Airlines, United Airlines, 67 Health Pass-enabled partners and 38 airports. International expansion is a tricky yet lucrative opportunity. Given the increased publicity from its IPO, I suspect that CLEAR will have an easier time than before talking to new partners.

According to the S-1, CLEAR information security program received the highest designation according to the Federal Information Security Modernization Act from DHS. It is also certified as Qualified Anti-Terrorism Technology under the Support Anti-Terrorism by Fostering Effective Technologies Act of 2002 (“SAFETY Act”). U.S Customs and Border Protection also uses CLEAR to let U.S citizens and permanent residents enter the country more expeditiously. Additionally, it will help TSA handle new subscriptions and renewals for TSA Pre Check. The acceptance and certifications that come from the federal government are a robust competitive advantage for CLEAR. It’s not easy at all to win these designations and work with the government, especially when it comes to security. The longer CLEAR is in the market, the more weight and trust the CLEAR brand will carry, making it exceedingly difficult for any challenger to compete. In the world of security, trust and brand names are of utmost importance. Those can take a long time to gain yet seconds to lose. So far, CLEAR has done a very good job of building its credentials. Any challenger will have to take time to go through the same process and no money in the world can speed up the process. Meanwhile, CLEAR can continue to expand its footprint & verticals and use more usage data to improve its technology platform and strengthen its lead further.

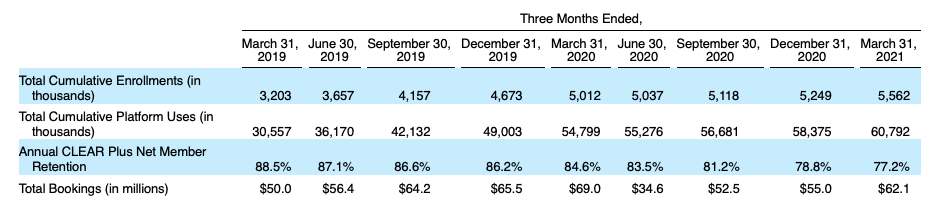

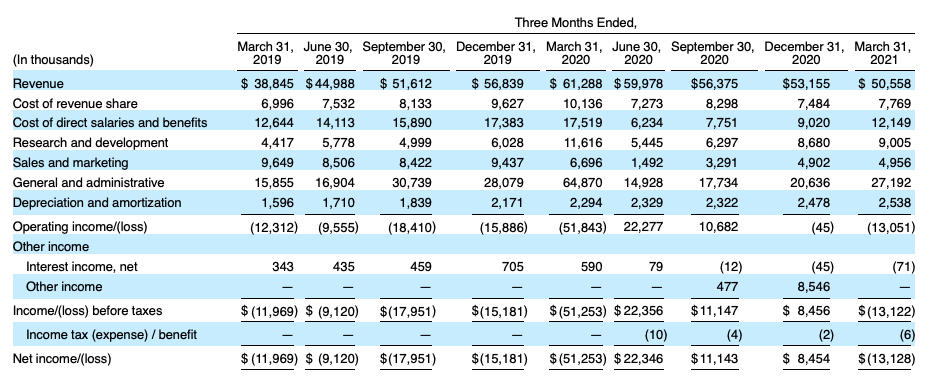

Let’s dig into the numbers. Compared to March 2019, enrollments, uses and total bookings in the quarter ending March 31, 2021 were up meaningfully. If you question why retention rate has been trending down and why the explosive growth often seen in IPOs is absent here, it’s worth noting that Covid-19 severely limited in-person events as well the travel industry; therefore, it is not surprising to see such a great adverse impact on CLEAR’s business. With that being said, as the country is opening up, travel is getting back to 2019 level and in-person events are relatively safe again, do expect to see these numbers go up in the next few quarters.

In the last two years, CLEAR had positive operating income only in two quarters, at the height of Covid. What concerns me isn’t the lack of explosive growth many may expect. It is the lack of economies of scale. Compared to 2019 quarters, the quarter ending March 31, 2021 didn’t seem to show that CLEAR gained much more efficiency. Granted, the impact of Covid-19 is undisputed and the company did seem to transfer some marketing expenses to R&D; which is a positive sign for a technology platform. Yet, the two biggest expense line items in Direct Salaries and G&A, mainly stock-based compensation, still dominate their cost structure. That makes me wonder when this trend will end, given that historical data in the last two years indicate otherwise.

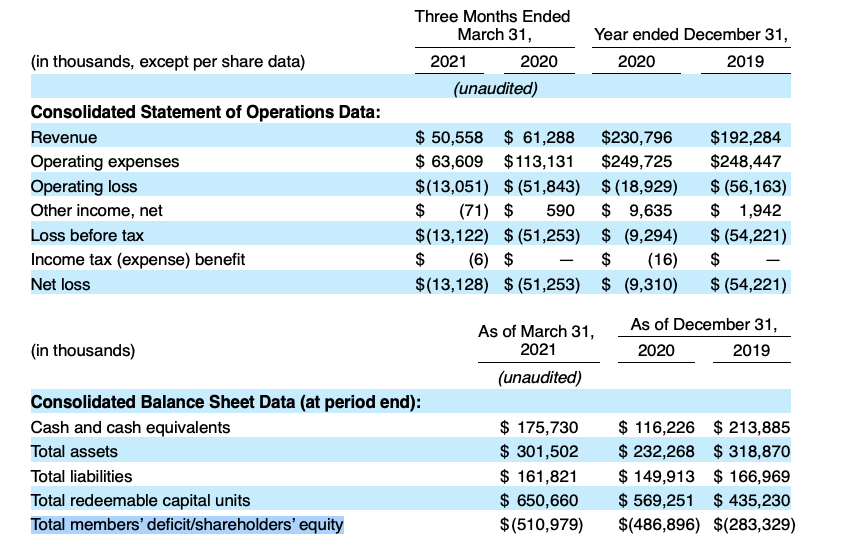

Another red flag is that the company has a shareholder deficit. Total shareholder equity is the difference between total assets and total liabilities. A deficit means that CLEAR’s liabilities are larger than its assets and that it has been losing more money than what investors put in so far. While a deficit may be the short term pain in exchange for the groundwork for future success and the IPO should give CLEAR a big windfall, investors shouldn’t gloss over this fact.

I like the potential growth and the competitive advantages that CLEAR has while being a bit concerned about how the company is currently managed. I put the company on my watchlist and will monitor it in the near future to see if it makes sense for me to take a position.

Leave a comment