Every year, Pulse, a Discover company, publishes a Debit Issuer Study, which covers the debit card landscape in the U.S. This year’s version is the 16th annual edition of the study and comprises of data from 48 financial institutions of different sizes in the country. If you are interested in the payments as well as financial services world, you should have a look at this study. Below are a few things that stood out the most to me, accompanied by some of my own comments

Debit spend per active account increased as growth in ticket size more than offset the decline in transactions

Unsurprisingly, stay-at-home orders last year curtailed debit transactions as stores were closed and folks were forced to remain at home. As a result, 2020 saw a decline of 2.5% in the number of debit transactions, the first contraction of the industry ever. Most of the damage took place in Q1 and especially Q2 before the use of debit cards recovered in the back half of the year. Compared to 2019, last year saw an increase in debit spend per active account, from $12,407 to $13,550. The increase resulted from 10.5% growth in ticket size despite the drop of 1.3% in the number of monthly transactions per active card.

Whether issuers are subject to the regulated interchange cap determines their unit economics

For issuers with $10 billion in assets or more, they are subject to regulations that cap debit interchange rates. Before we move forward, let’s take a step back to revisit what interchange rate is. Every time a transaction takes place, the merchant involved has to pay a small fee to the bank that issues a debit/credit card that the consumer in question uses. The fee is calculated as % of the transaction value and usually determined by networks like Visa, Mastercard, American Express or Discover. In this case, the Federal Government caps the interchange rate for big issuers that have $10 billion+ in assets. According to the 2021 Debit Issuer Study, exempt issuers earned 42.5 cents every transaction, compared to 23.7 cents for regulated issuers. Due to this difference, exempt issuers generated almost twice as big as regulated issuers in annual gross revenue per active debit account ($132 vs $71).

This is one of the reasons why neobanks can offer debit cards with rewards and no fees. Neobanks or challenger banks are usually technology startups working with exempt issuers to offer banking services. The startup in this partnership takes care of the marketing and the product development while the exempt issuer rents out its banking license and deals with all the banking activities such as underwriting, regulatory compliance or settlement. Because the exempt issuer earns higher interchange rates, it can afford to share part of that interchange revenue with its startup partner which, in turn, uses that revenue to fund operations and generate profit. However, I wonder if it’s really fair when a neobank or a financial service company becomes so big while still taking advantage of this “loophole”. Take Square as an example. It’s a $120 billion publicly traded company. It works with Marqeta and by extension Sutton Bank, which is exempted from the regulations over interchange rates, to offer Cash App. Is it truly fair for Square to be able to leverage this loophole when it has a much bigger valuation than many banks with more than $10 billion in assets?

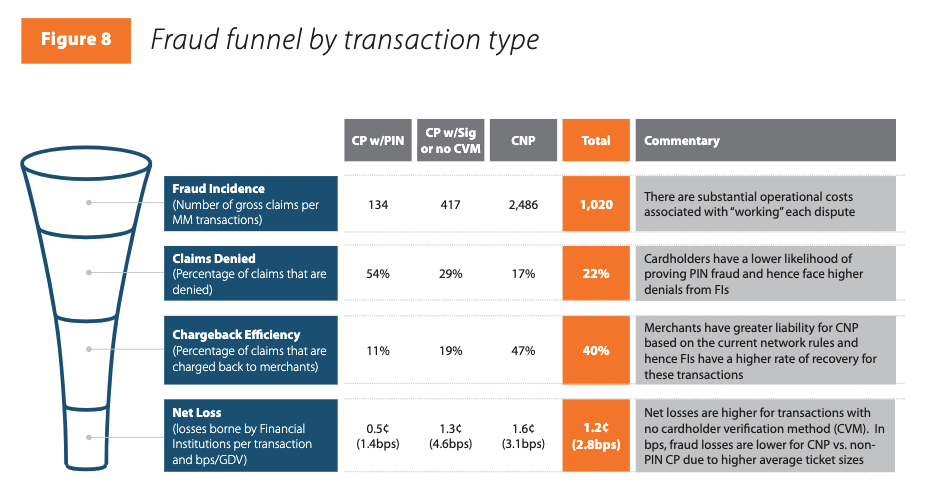

The rise of Card-Not-Present transactions means the rise of fraud threats

When stay-at-home restrictions were in effect, consumers didn’t shop at the stores and instead switched to digital transactions. Consequently, Card-Present (CP) transactions per active card fell by 10% last year. On the other hand, Card-Not-Present (CNP) per active card increased by 23% and made up for one-third of all debit transactions.

Because CNP transactions are less secure than CP ones (due to lack of customer verification), the growth of CNP during the pandemic led to more fraud incidents. CNP and CP with PIN transactions both made up 34% of debit transactions in 2020. However, while the latter made up only 5% of the total fraud claims, the former were responsible for 81% of the claims. Among the CNP fraud claims, 47% were successfully recovered, meaning that consumers had their money back and merchants lost some revenue.

Whenever a fraud claim happens, it brings an unpleasant experience to both the cardholder and the merchant in question. Hence, issuers may want to focus on ensuring that fraudulent transactions don’t even happen in the first place, especially with CNP.

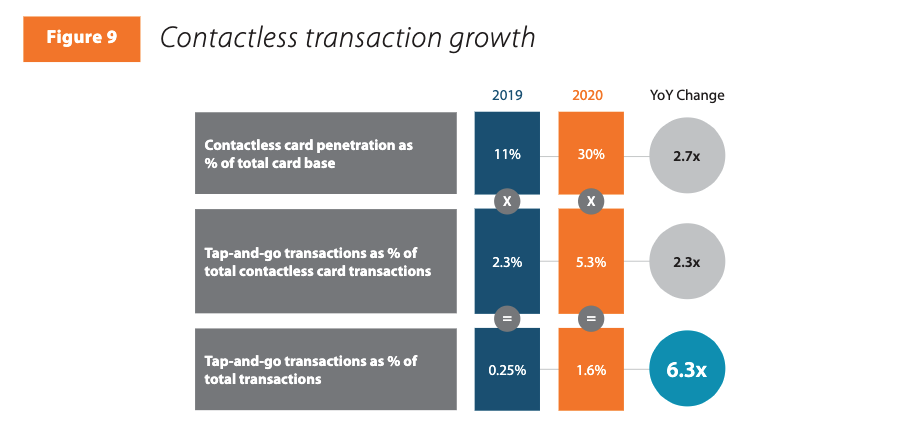

Contactless and mobile wallet transactions are on the rise

According to the study, contactless is projected to be available on 64% of all debit cards by the end of 2021, up from 30% in 2020, and 94% by 2023. Even though contactless volume grew by 6 times in 2020, it still made up only 1.6% of total debit volume. As consumers become increasingly familiar with contactless and the feature is available on more cards, I expect the share of contactless volume to keep that impressive growth pace for at least a couple of years.

Meanwhile, mobile wallet transactions funded debit cards through three major wallets (Apple Pay, Samsung Pay & Google Pay) reached 2 billion in 2020, around 2.6% of the total debit volume, with the average ticket of $23, up 55% YoY. 57% of this mobile wallet volume were made in-app and the rest took place in stores. If we look at the competition between the aforementioned wallets, Apple Pay is the outstanding performer in every metric. In fact, Apple Pay had an overwhelming 92% share of all mobile wallet transactions using debit cards.

Starting 2022, Visa will put in place new interchange rules that are aimed to encourage more tokenized transactions such as mobile wallets. Hence, I expect that when we read the 2023 edition of this study or beyond, we’ll see a more prominent role of mobile wallet transactions in our society.

Leave a comment