In this post, I’ll touch upon briefly the definition of a Super App, give a few examples and talk about the business implications of these apps.

The term Super Apps is generally credited to Mike Lazaridi, the founder of Blackberry, who defined it as “a closed ecosystem of many apps that people would use every day because they offer such a seamless, integrated, contextualized and efficient experience”. In laymen’s terms, a Super App is an application that offers various services on one interface. While the mix of services offered by Super Apps varies from one to another, the common denominators of these apps are 1/ they are all two-sided networks popular with both merchants and consumers and 2/ they all began their journey by being excellent in one function before branching out to others. Merchants need to have access to a lot of consumers to join a network while consumers only find the network useful when there is a lot of utility, namely plenty of merchants. The chicken and egg problem of a two-sided network is hard. Therefore, the singular focus on a vertical in the beginning makes sense as start-ups can’t afford to solve this issue in multiple verticals. No-one can build a Super App right from the get-go. Once an app excels and makes a name for itself in a vertical, why not leveraging existing traffic and offering users more reasons to stick around longer?

Examples of Super Apps

WeChat started out as a messenger app. An engineer named Allen Zhang alerted his employer Tencent on a threat of other competitors taking away its market share and app engagement. To stay competitive, WeChat transformed itself into an app on which users could do everyday things on a single interface including payments, social media, e-commerce, doctor appointments, hotel reservation or ride-hailing. The pivot was a hit as the new services surpassed even the apps that inspired WeChat in the first place.

Facebook and its founding story need little introduction. Over the years, Facebook has added several services to make itself stickier as a platform. Nowadays, users can shop on a marketplace or Facebook-native stores; create new connections with Facebook’s own Tinder version; make payments with Facebook Pay or consume exclusive content from creators. With its ambition and virtually limitless resources, it won’t be a surprise that Facebook or Meta will expand its offerings in the future.

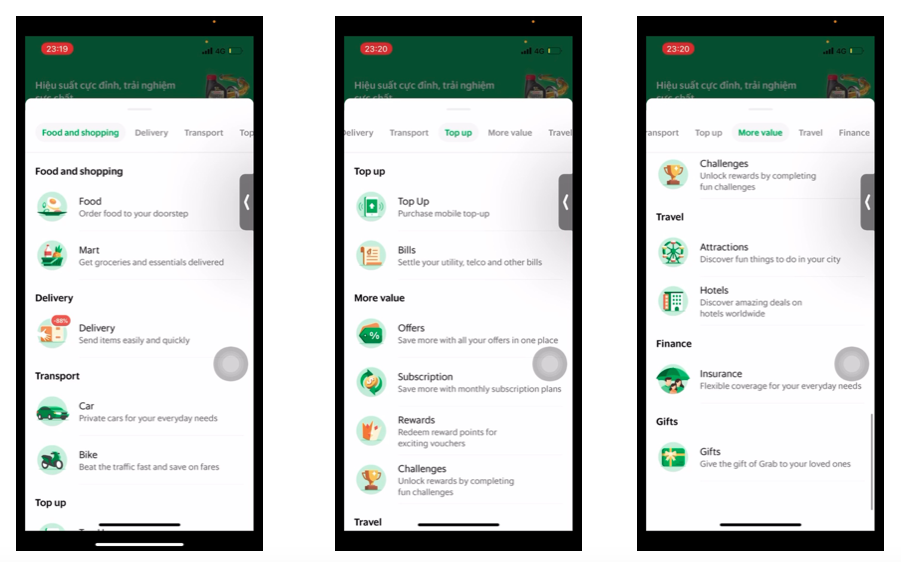

Grab

The title of grab.com reads “Grab: The Everyday Everything App”. Its status as one of the biggest Super Apps in Southeast Asia is so different from its humble beginning. Grab was founded as a taxi-hailing business in Malaysia in 2012 by two Harvard graduates. The company gradually expanded into other areas, such as other modes of ride-hailing, food delivery & nonfood delivery, travel bookings, bill payment and financial services. In Vietnam, almost everyone in big cities uses Grab for daily tasks from food delivery, ride-sharing or bill payments.

Uber

Uber was founded in 2009 by Travis Kalanick and Garrett Camp as a ride-hailing alternative to taxies. The company’s meteoric rise saw it become a global phenomenon, but the company today is more than just a ride-hailing app. In 2014, Uber launched a food delivery service called Uber Eats, which was later rebranded under Delivery. While Covid-19 decimated the Mobility segment (ride-sharing) as riders were restricted by stay-at-home orders, the pandemic was a catalyst for the transformation of Uber as a whole. Delivery has been growing substantially due to consumers ordering food and grocery deliveries. Its gross bookings have repeatedly surpassed Mobility’s and now reaches Mobility’s pre-pandemic level. Second, the company has made strategic acquisitions to expand beyond food delivery. In June 2020, Uber acquired Cornership, a popular grocery delivery service in Latin America. A few months after, it added Postmates, which is very competitive in coastal cities and offers delivery-as-a-service for non-food items. In October 2021, Uber took over an alcohol delivery startup called Drizly. The company has been tinkering with marijuana delivery in Canada and waiting for the green light from the federal government before launching it in the U.S. Powered by the new capabilities, nonfood categories make up around 5-6% of Uber’s overall gross bookings and are expected to grow more in the future. Uber’s ambition is very simple: be the go-to app when consumers have a transportation need.

PayPal

PayPal first made a name for itself by being a secure digital wallet and online payment system, especially as the primary checkout option on eBay. Since its spin-off from eBay in 2014, the company has added plenty of services to its mobile app and become a formidable two-sided network, due to relentless acquisitions and product development. End users can access various services on the current PayPal app, including paycheck deposit, high-interest savings, bill payment, remittance, credit cards, debit cards, in-store & online payment, BNPL, PayPal Credit, P2P payment, shopping deals and investing. PayPal’s end goal is to be the go-to Financial app for its users.

Cash App

Cash App started out as a P2P payment app in which users could transfer funds to anybody in the U.S. Nowadays, users can pay for purchases in stores and online with Cash App debit card and Cash App Pay; invest in stocks and cryptocurrency; or make deposits into checking accounts. In November 2020, Square bought the tax filing division of Credit Karma and subsequently added to its flagship app the ability to file taxes and receive tax refunds. In August 2021, Square paid $29 billion for Afterpay, one of the major BNPL players in Australia and in the U.S. It’s just a matter of time before Cash App turns on BNPL for its users and merchants. Cash App’s ambition is similar to PayPal’s; which makes it interesting to see how the two compete in the future.

Pros and Cons of partnering with Super Apps

Merchants stand to gain an additional payment option as well as more sales from Super Apps, but the story isn’t all rosy. Too much reliance on Super Apps means that merchants’d risk ceding the control of direct customer relationships. In business, few things are more valuable than that. Take Apple and Amazon for instance. Apple’s customer base is so loyal and attached to their brand that almost all developers or other brands take the back seat in negotiations . Amazon’s scale and iron grip on the valuable Prime base allows them to dictate terms over merchants. When you buy from a merchant on Amazon, do you feel more related to the former or the latter?

For banks, Super Apps can have adverse impact in a couple of ways. First, services such as PayPal in 4, Afterpay, PayPal Credit or PayPal/Venmo credit cards can reduce issuers’ credit card spend and subsequently balance as well as revenue. Secondly, it’s in their interest to have users maintain an in-app balance and keep funds away from banks’ checking accounts. Think about it this way: would you feel more poised to use PayPal when your PayPal balance was $20 or $0? That’s why Venmo credits dormant users $10 for downloading and logging into the app again or why Square wants users to keep tax refunds in Cash App balance. The reduction in deposits can raise banks’ cost of funds as well as threaten to cut off the most fundamental relationship with customers.

On the other hand, Super Apps present a battleground for financial institutions vying for wallet share. Once the connection between checking accounts or debit/credit cards and these Super Apps is established, users often don’t want to go through the inconvenience of updating their default payment method. Hence, every financial institution wants to be the primary source of funds for consumers on these Super Apps to have a leg up over the competition. In this sense, Super Apps offer a business opportunity.

In summary, as you can see above, there are multiple paths towards the Super App status, whether an app’s starting point is to be in messaging, digital wallets or ride-sharing. I think all successful consumer-facing apps have ambition to gain the Super App status. If not, they’d do something wrong. It’ll be interesting to see how these Super Apps compete for mindshare as feature parity is established (meaning they all offer similar features). For merchants, working with Super Apps can be a double-edged sword. While the benefits these apps bring are very tempting, merchants need to keep in mind the risk of losing customer relationships. Like people usually say: don’t miss the forest for the trees.

Leave a comment