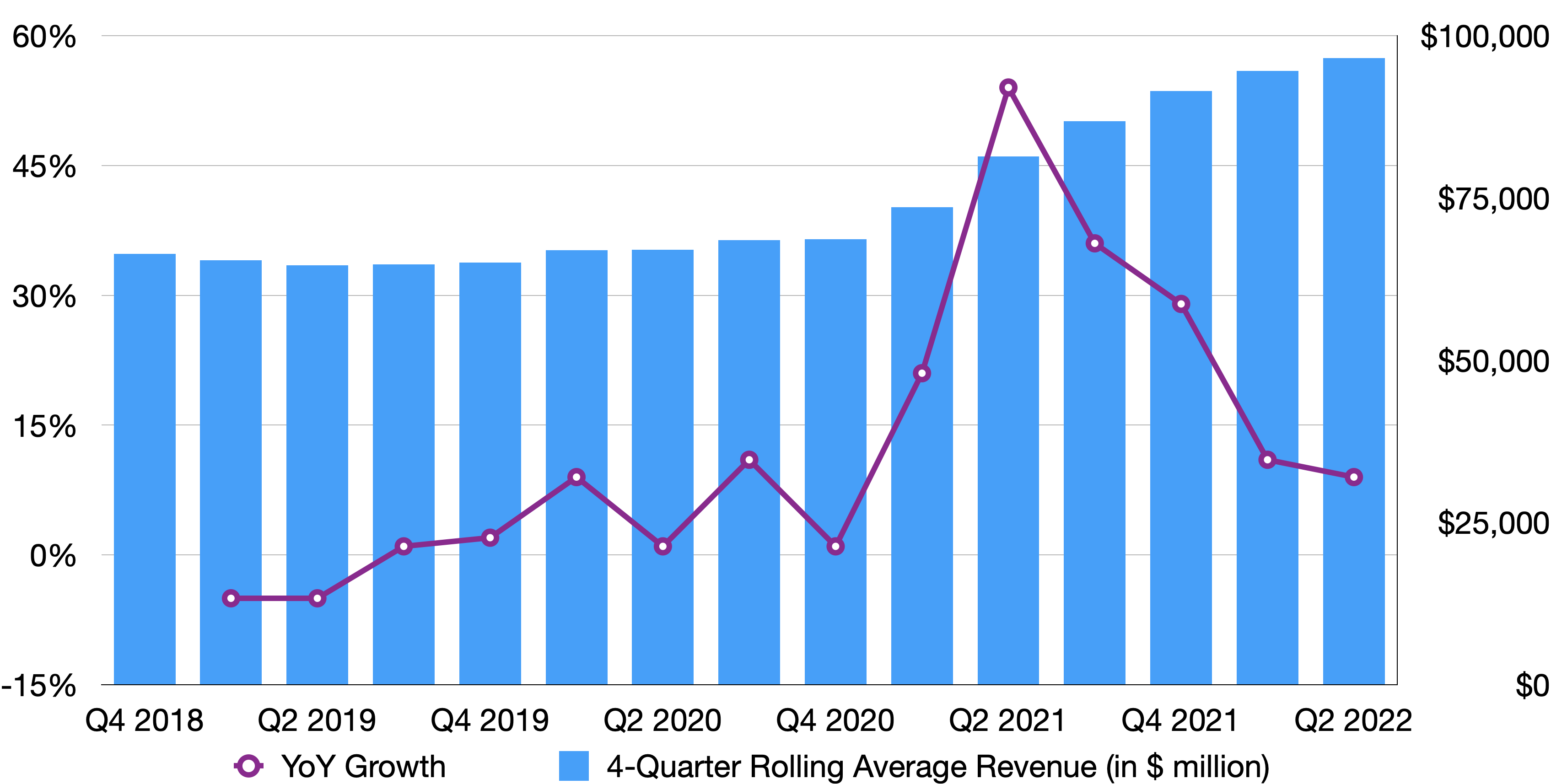

On Thursday, Apple announced the results of their Q2 FY 2022. Overall, the company recorded almost $97.3 billion in revenue the last 90 days, a record for Q2 in Apple’s history. That means they generated more than $1 billion a day. The 9% YoY growth is already on top of the 54% growth last year. To put it a bit more in perspective, only 26 companies in the S&P 500 had more revenue in the whole year of 2021 than what Apple made in this quarter. It’s also worth noting that these numbers were affected by the supply chain constraints. Just really spectacular! While YoY growth rates have been declining, it’s not a surprise given the rule of big numbers. Plus, this year will see some hardware upgrades that can catapult Apple’s revenue to new heights.

While Services still only makes up 20% of the company’s revenue, its gross margin is a spectacular 73% due to higher sales from advertising, the App Store and cloud services. I suspect this trend will continue in the future. It costs Apple little to offer cloud storage and how many Apple device owners who love taking photos and videos yet are limited by the free storage don’t have an iCloud subscription? Apple Care is a warranty program that gives a bit more assurances to device owners. Given that Apple products last a very long time and most customers are careful with their devices, Apple Care is a very profitable service for the company. The iconic tech giant recently launched Apple Business Essentials, which is similar to Apple Care, but for small businesses. The new service has a lot of potential and will be a great contributor to the company’s margin. Last but not least, advertising. It’s not a coincidence that every popular platform wants to have an ads solution. The demand is always there and the margin is high. Apple is still in the early stage of monetizing traffic to the App Store; therefore, will undoubtedly fine-tune its ads operations so that it will keep raking in profitable dollars.

In the last quarter, supply chain constraints still badly affected iPad, making it the only major business segment of Apple without a YoY growth. Wearables and Services haven’t had a down quarter in the last three years. In fact, growth has been in double digits. Mac showed an impressive 15% growth on top of a 70% increase last year. According to Apple’s CFO, “we had a March quarter record for upgraders, while at the same time, nearly half of the customers purchasing a Mac were new to the product”. iPhone, led by the iPhone 13 line-up, grew by 5% after recording 66% increase last year. The company estimated that the lockdown in Shanghai will impact revenue by $4-8 billion in Q3. Hence, the winning streaks of some segments may likely come to a halt in 90 days, but since demand is very strong for Apple products, the company has reasons to be confident in the long-term health.

Regarding geographic segments, Americas is a bright spot with YoY growth of 19%, better than management’s expectations. Europe was adversely impacted by the pause in Russia for a month. China is still Apple’s 3rd biggest segment, but the company warned that Covid-related restrictions would affect demand, at least for Q3 FY2022. Japan and Rest of Asia Pacific felt the impact of unfavorable foreign exchange rates.

Overall, it is another great quarter from Apple despite all the macro challenges. It is proof that the underlying strengths of the business are still intact and goes to show the calm and competent leadership of the management. Zoom out and you will see that there is no other company that can rival Apple in terms of product and service portfolio, the global scale and the customer loyalty. There are challenges and uncertainty ahead, including the war between Russia and Ukraine, Covid-related restrictions in China, the supply constraints, especially silicon shortages, and unfavorable exchange rates. Nonetheless, I am confident Apple will navigate through such challenges deftly and come out stronger.

Disclaimer: I own Apple stocks in my portfolio

Leave a comment