Last week, Uber announced the earnings results of Q1 FY2022 and the numbers show that its operation continues to recover well after Covid-19 disruptions. Here are the highlights:

- Gross Bookings: Gross Bookings increased by 35% to $26.5 billion

- Mobility & Delivery Gross Bookings: Mobility saw 58% in Gross Bookings while Delivery had a 12% YoY growth

- Revenue: Revenue rose by 136% to $6.8 billion. Total revenue was boosted by the acquisition of Transplace. Nonetheless, Mobility and Delivery revenue grew by 195% and 44% respectively

- Net loss: While net loss was an astounding $5.9 billion, $5.6 of which came from the loss in value of equity investments in other companies. Loss from operation stood at $482 million, down from $1.5 billion a year ago

- Free Cash Flow: FCF for the quarter was -$47 million, up from -$682 million a year ago. Uber’s operation cash flow was $15 million, up from -$611 million in Q1 FY2021

For Q2 FY2022, forecast Gross Bookings is between $28.5 to $29.5 billion, resulting in growth of 30% to 35%, on top of the 114% growth booked in Q2 last year. The company also expects to generate positive free cash flow for the full year of 2022. Investors and analysts must love the forecast by Uber as the drop in its stock price last week was much less severe than Lyft’s. And they should like what they see from Uber, especially when we dig into the numbers a bit more.

As mentioned above, revenue growth outpaced gross bookings growth in both Mobility and Delivery. Mobility take-rate hit 23.5% in Q1, back to the pre-pandemic levels, and it’s still short of the long-term target of 25% set on Investor Day 2022. Delivery has seen a steadily increasing take-rate for the past 3 years, reaching 18% in Q1 FY2022, which is already higher than the target of 15%. Delivery is a highly competitive space with the presence of heavyweights such as DoorDash or Instacart. I wonder if this heightened take-rate will remain stable or if Uber will reduce its cut to attract and retain merchants.

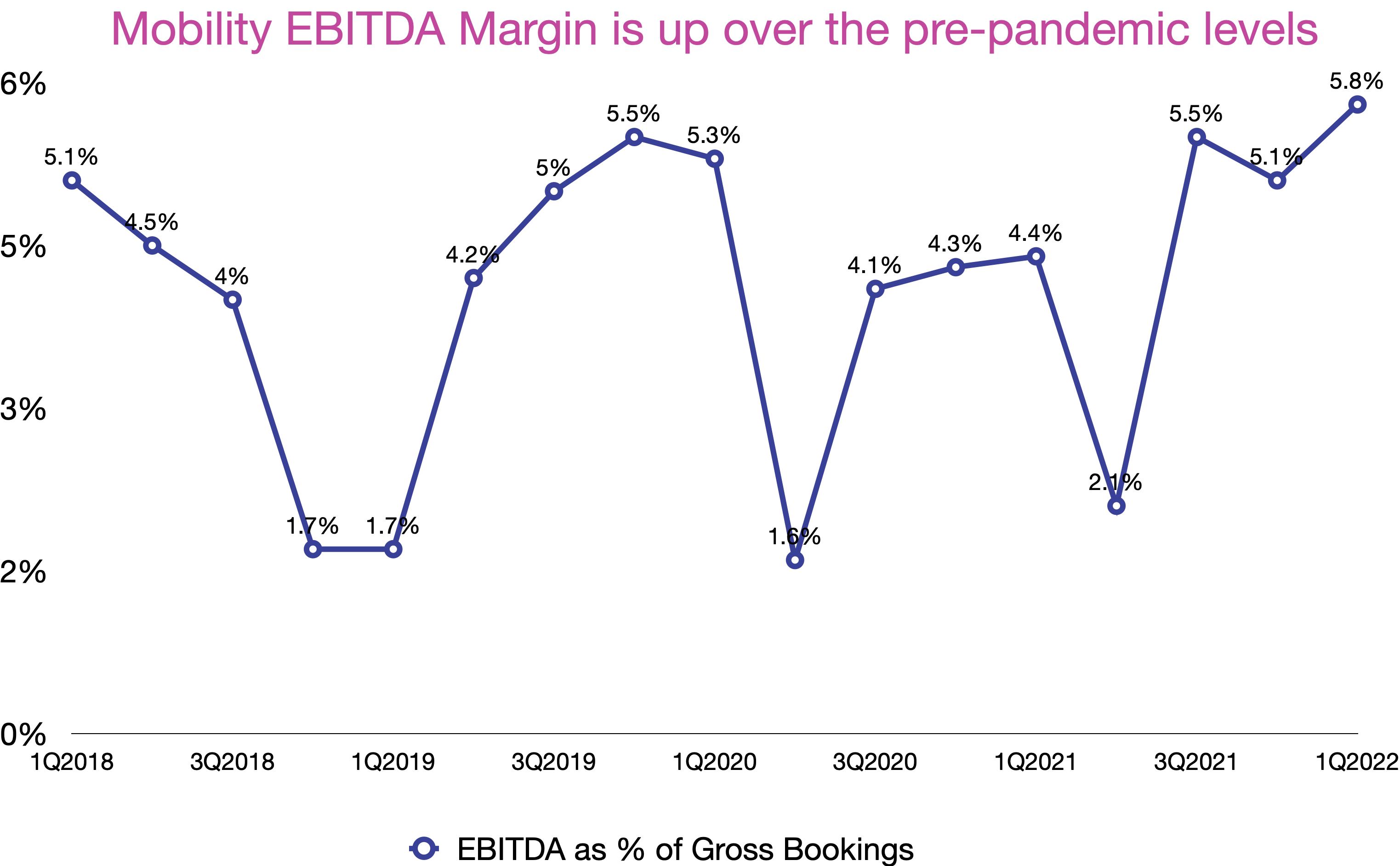

The good news for Uber is that such an increase in revenue didn’t come at the expense of profitability. Mobility’s adjusted EBITDA margin came back to the 2019 levels while Delivery’s was positive for two consecutive quarters in a row. Last quarter saw Freight become adjusted EBITDA profitable for the first time in the company’s history. Since the management team forecast to have positive FCF for the whole year, this trend seems to become a norm moving forward, rather than a fluke. Furthermore, the Fed plans to have more rate hikes in the coming months to curb inflation. At a time like this, companies will do well to demonstrate to investors that they can generate profits. To that end, Uber is in the pole position to reach profitability in an industry whose unit economics have long been questioned.

There are a few levers that can help Uber grow both the top and bottom lines. First, airport rides. Rides to and from airports used to account for 15% of Mobility Gross Bookings. From the low during 2020, share of airport gross bookings have grown to 13% of Mobility. There is still room to get back and probably exceed the pre-pandemic levels. Additionally, the same goes for Mobility as a segment. Its Gross Bookings is still down by compared to the 2019 levels. Total GBs for Mobility in 2021 trailed that in 2019 by $14 billion. Once that gap is closed, the higher take rate from this segment can only help with the bottom line. Additionally, the next lever is ads. The ads business is growing healthily as annualized run rate rose to $225 million in Q1 FY2022, more than double what was reported a year ago. Almost one out of four Delivery merchants is an active advertiser on the platform. As Sponsored Video Ads is available on a pilot basis, we should see more merchants advertise and more ads revenue. Last but not least, new verticals. These verticals have been doing about $4 billion in annualized run rate every quarter in the last few months. That’s less than 10% for all Delivery GBs in 2021. Given the latest developments such as the deepened partnership with Albertson, the expansion of Eats in Germany, the new deal with BP, the collaboration with Rakuten and Amazon Prime in Japan, and the introduction of group ordering, I expect new verticals to grow substantially soon.

In summary, I find the earnings report positive. Uber stock has been battered for months as its price dropped by 44% in the last year. Folks are concerned about the business model and they have reasons to be. Uber functions as a middleman working with a lot of important stakeholders: consumers, drivers, merchants and lawmakers. Maintaining those relationships on a global scale in different cultures and political agendas is extremely difficult. For good measure, competition is fierce with deep pockets as well. To invest in the company means that one believes in flawless strategy AND execution. One down quarter wouldn’t do as much damage to Apple as it would to Uber because the former has a dominant market share and is in a much better position than the latter. With that being said, Uber management navigated a pandemic by pivoting to Delivery, which changed the business forever. Could another management team have done better? Possibly, but we never know. The fact that Uber now has a friendlier image than it did, that its Delivery business is an equal of Mobility and that it has other levers to pull is a testament to the work of the management. Just look at Lyft. Even though its revenue is smaller than Uber Americas, its revenue growth rate hasn’t recovered as quickly. That’s due to Delivery, because as mentioned above, Uber Mobility’s business is still down compared to the 2019 levels. That goes to show how important it was for Uber to react and execute effectively during the pandemic. While it’s highly challenging to stay competitive and create profit in this industry for factors mentioned above, it’s precisely such factors that can make Uber’s moat robust if they can get execution right. A big if, indeed. I get where the skeptics come from, but personally, I am still on the believer side, for now.

Disclaimer: I own Uber stocks in my portfolio.

Leave a comment