Overall

Netflix recorded a tad below $8 billion in revenue, a 9% growth in revenue compared to the same period a year ago. It’s scarcely believable that a company formerly selling DVDs pivoted to online streaming and is now generating $32 billion in annual income. Because of some one-time expenses and the adverse impact from unfavorable exchange rates, Netflix’s operating margin was about 20%, down from 25.2% in Q2 FY2021. The company lost 1 million subscribers globally, an improvement over the loss of 2 million subscribers as forecast 90 days ago. Free Cash flow (FC) in the quarter tallied up to $13 million, significantly higher than -$175 million in FCA recorded in Q2 FY2021. These results were received well by investors as the stock has been up since the announcement.

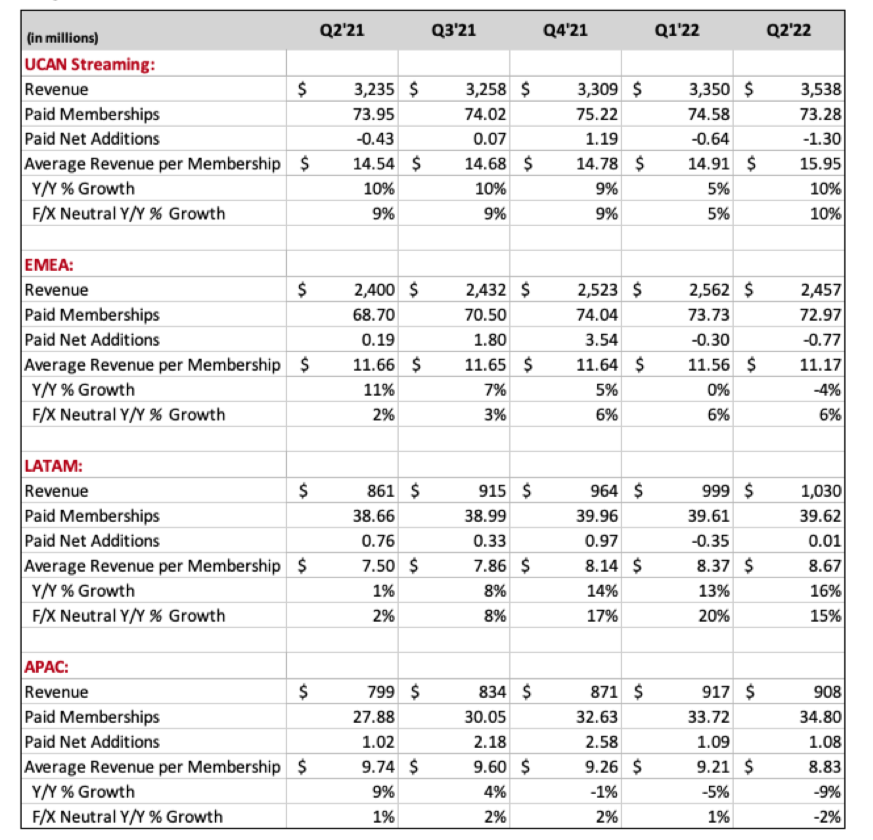

Subscriber loss in US and Canada

Netflix losing 1 million subscribers globally deserves some headlines, but I think it’s more telling that they lost 1.3 million in the most lucrative market UCAN (US and Canada). Such a decline is biggest in the last 5 years, if not ever. Even though the loss in UCAN was offset by the growth in APAC, Netflix is trading some of the most profitable members for some of the least. This happened despite the resounding success of Stranger Things Season 4. Needless to say, it is not what either the management or investors want to see.

The loss of subscribers in UCAN seems to coincide with the growth in subscription fees. Regular price hikes, coupled with inconsistency in content delivery, definitely impacts churn. I don’t think Netflix will lower their prices, especially when they are going to launch an ads-supported tier next year. While the company forecasts a net add of 1 million subscribers for Q3, who is to say that the losing streak in UCAN will abate? Are we going to see another slide in 3 months’ time?

The missing Net Add chart and the use of dubious data

Netflix used to have a chart (Figure 3) showing net adds by year. 2020 was really impressive due to the stay-at-home orders across the country. 2021 was lower than 2018 and 2019 due to the pull-forward effect. This chart was seen last in Q4 2021 earnings. Since then, it has been missing. The company doesn’t want investors to look at the net adds in the first two quarters of 2022.

I get that. Any company wants to put their best foot forward in earnings as long as the information is accurate. Withholding some unfavorable data is a common practice. What is funny; however, is that Netflix uses cumulative engagement on Twitter as a metric to show how dominant Stranger Things 4 was, against Obi-Wan Kenobi and Top Gun. I don’t know about you, but I’d take Top Gun’s $1.3 billion in box office any day of the week and twice on weekend, over some ambiguous engagement metrics. This is NOT the first time Netflix uses some misleading data in their letters. Back in January 2020, they turned to Google Trends data to demonstrate that their Witcher series was more popular than Mandalorian, Jack Ryan or the Morning Show. The key here is that Witcher is a popular game as well. Without isolating the category that keyword is in, it’s not fair to compare Witcher to the unique name of other shows. I explained here in more details.

Occurrences like these lost some of my confidence in the company

Ads-supported tier and the binge model

I have to give credit to Netflix’s management. They stuck their guns with the binge model (releasing all episodes at once instead of dripping one per week) despite what many claim contributes to the lack of engagement around their content. Their stock has been hammered hard in the last few months. I am sure that spurred a lot of meetings at the highest level. Still, they chose to be who they are and what they are known for. I can only give them props for that.

However, this binge model puts a lot of pressure on Netflix to deliver quality content consistently and regularly to reduce churn. Series like Sex Education, Stranger Things or Ozark released all at once certainly will draw subscribers, But to keep them on the platform, given Netflix being the most expensive streamer out there, is another matter. They will need great content every month. I watched The Gray Man, which is Netflix’s most expensive film ever and has arguably the most advertising from the company. The flick stars some of the most famous actors such as Chris Evans, Ryan Gosling and Ana de Armas, and the directors of Avengers: End Game. The action is definitely entertaining, but the plot leaves so much to be desired. That’s the pattern with Netflix. I don’t think that they are as good as Apple or HBO in producing original content. That’d be fine if their price point was not the highest or if they didn’t follow the binge model. But because it is and they do, it makes me quite bearish on the company.

An ads-supported tier will help Netflix expand the clientele and appeal to those low-income households that consider Netflix a luxury. Folks that are on the fence about leaving the streamer can instead choose the new tier so that they can preserve access while paying less. The benefits of this plan are straightforward, but how Netflix will execute it is a totally different matter. Key questions are:

- What will the ads look like? How will they affect the customer experience?

- How will Netflix enhance the targeting while protecting customers’ privacy?

- How long will it take for the company to fine-tune all the workflow details and become well-versed in the world of advertising?

- Are the ads going to help brands drive awareness only? If there is a call to action and such action leads to a website outside of Netflix’s domains, will Netflix be able to report reliable attribution?

Originally, I was concerned about Netflix and its ability to delivery content consistently. Not just any content. Great content that can get viewers hooked. Then, I was drawn into taking a very small position on the company because I mistakenly followed some on Twitter and didn’t believe my own intuition. Till now, I am still concerned about Netflix’s outlook as an exclusive SVOD company. Their venture into the advertising world is exciting, but it poses a lot of questions and frankly uncertainty. Until such questions and certainty are squared away, I will stay away from this stock.

Leave a comment