Last week, PayPal announced its Q2 FY2022 results, its forecasts and some important personnel changes. Here are the headlines:

- Net revenue hit $6.8 billion, a 9% YoY growth

- International revenue declined by 1.7%, to $2.9 billion, while US revenue was $3.8 billion, a 19% growth YoY

- Operating cash flow and free cash flow grew to $1.5 billion and $1.3 billion respectively, meaning that FCF margin is 19%

- Total Payment Volume increased by 9% to $340 billion

- Total payment transactions of 5.5 billion

- US TPV grew 16%, to $219 billion, while International TPV and Cross Border TPV decreased by 1.6% and 11.8% respectively

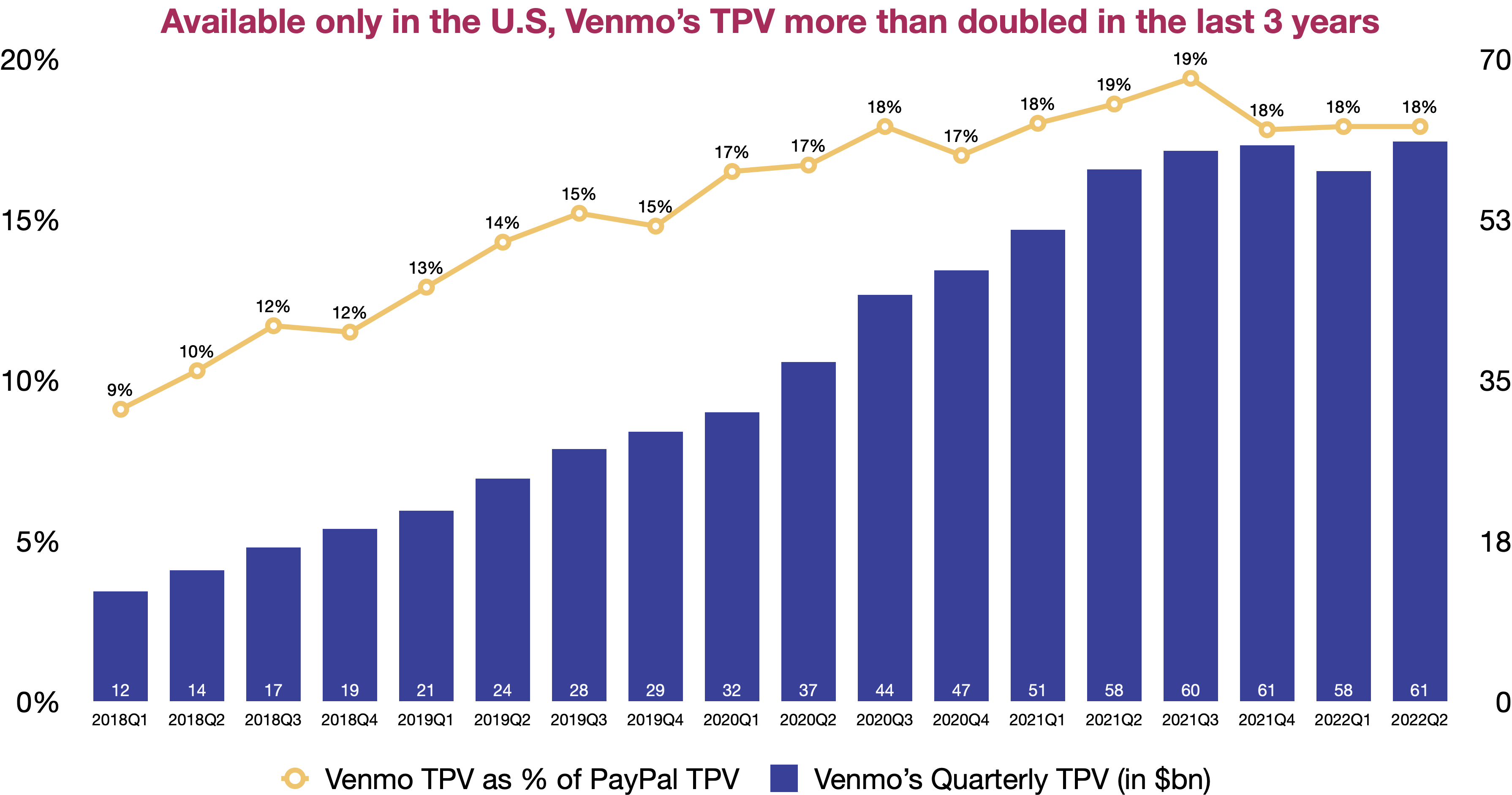

- Venmo recorded $61 billion in TPV, an increase of 5.2%, and 90 million active accounts

- Total active accounts went flat sequentially at 429 million with 35 million active merchants

- While the company welcomed a new CFO, it’s now looking for a replacement for their CPO, who is retiring at the end of the year

- Cost-saving initiatives are expected to save the company $900 million by the end of 2022 and $1.3 billion next year

- $15 billion in share buybacks was authorized, $4 billion of which will be realized by the end of 2022

- PayPal expects operating margin expansion in FY2023

Despite the tough macro challenges and fierce competition, PayPal’s TPV increased by 9%, on top of the 30% and 40% YoY growth in the last two years. That’s pretty solid because Visa grew payment volume in the same quarter by 12%, even with its duopoly market power. The divorce from eBay is entering the final stages as the famed marketplace now makes up only 3% of PayPal’s TPV and is projected to have negligible impact in the future. Losing a household name like eBay isn’t great, but because the partnership was exclusive, PayPal couldn’t work with any other retailers or marketplaces. Hence, the separation paved the way for deals like the one with Shopify or Amazon, and would benefit PayPal more in the long term.

Another bright spot is the US market. PayPal’s home soil saw a 16% increase in TPV and a 19% expansion in revenue. Considering that the US is home to other payment alternatives, including some fierce direct competitors, those US numbers showed resilience and a formidable market presence of PayPal. Because the company barely added new active accounts, given the lack of full disclosures, my guess is that PayPal managed to increase usage among existing users.

Among the factors that contribute to the domestic success, I want to call out Venmo. Popular among young consumers, Venmo boasts 90 million active users, double from what it had three years ago. In the same time frame (from Q2 2019 to Q2 2022), Venmo TPV grew by 150% from $24 billion to $61 billion. Despite this growth, Venmo still has a lot of grow to monetize. The three main levers are debit card, credit card and the partnership with Amazon. While I suspect that PayPal will have to make some financial concessions to be on Amazon’s marketplace, this will undoubtedly help grow both revenue and margin. Meanwhile, the management team has high hopes for what the Venmo debit and credit card can bring onto the table. If PayPal can monetize Venmo more, the company will become so much more secure and attractive in the eyes of investors. In case you forgot, despite the massive scale of adoption, Venmo is still only available in the US.

Gabrielle Rabinovitch

I’d also point out the card strategies for Venmo are important, as well. The debit and credit cards continue to grow their volumes and those are really important for habituation. They reinforce all the in-wallet spend with offline spend, as well.

Dan Schulman

Yes, I totally agree with that. If you look at Cash App, their big growth is off of their debit card. We have a lot of room in our debit card and credit card to grow too.

Source: PayPal’s Sell-Side Analyst Conference

Moreover, I am very pleased with the switch of focus onto increasing efficiency. I used to receive a bunch of promotional offers from PayPal. $5 here, $10 there for low-impact activities. Now, the company is willing to let go low-engagement customers and focus marketing dollars on driving usage from active users. Efficiency is also apparent in the product development side as well. Although stock trading was on the plan last year, PayPal decided to put a halt on its development. The push for in-store QR code is now replaced by efforts to promote card usage. These decisions obviously led to surplus in headcount and dismissals, where necessary. Due to its enormous scale, PayPal managed to negotiate more favorable contract terms with suppliers. The management team believes that these efforts will drive ROI and yield higher results for the organization. Concretely, they are estimated to bring $900 million in cost savings for the rest of FY2022 and $1.3 billion next year.

These cost savings are likely the main reason why the management forecasts operating margin expansion next year. Low-margin businesses such as BNPL, Venmo and Braintree are expected to grow in the near future. It’s unclear to me, reading their reports, where the margin will come from the revenue side of things. Hence, the gains must come from being a leaner organization with reduced expenses.

On the other hand, it’s not all smooth and rosy with PayPal. I am concerned about the uncertainty that changes at the top level will bring. They have a brand new CFO, who was chosen among at least 14 candidates. By next year, they will have a new Chief Product Officer. These changes may bring about new ideas and positive results, but they may also delay the progress as new hires need time to acclimate themselves to the new work settings.

While it’s good that a business wants to be laser-focused and mindful of expenses, it remains to be seen whether PayPal is doing too much. After riding to new heights amidst Covid, PayPal’s stock got clobbered, down from more than $300 to $90, due to abandoned forecasts and slowed growth. Then, the narrative switched to higher efficiency and more focus. I get it. The leadership wanted to present a nice story to investors to stop the bleeding. They may even genuinely want to set the company on a better course for the future. But they also have a history of botched plans and forecasts. Who is to say that they are not being too aggressive at the moment? What if the cost cuts hurt the business in the process? We already have three consecutive quarters of decline in International. PayPal competes on multiple fronts and their competitors are fierce. Can they right-size their capital allocation to avoid disasters?

Overall, this is not a disastrous quarter. There are some bright spots, including Venmo, solid growth overall, the US market, the cost-cutting initiatives (at least for now) and the buybacks. However, there are also things that give me pause for concern. As bullish as I want to be on the company’s outlook, I’ll wait for another quarter or two so that by then some of my concerns will be hopefully eased.

Appendix

Leave a comment