CFPB just released a report on Buy Now Pay Later (BNPL) which I think is pretty comprehensive. The report covers a lot of ground using data between 2019 and 2021 from five surveyed lenders. If you are interested in consumer financial products or BNPL in particular, you should have a read. Below are some of my takeways

BNPL grew furiously in 2020 and 2021

According to the report, the number of loan originations from BNPL lenders in the US grew by 227% per year, from almost 17 million in 2019 to 180 million in 2021. The amount of BNPL loans grew even faster, by 245% per year, from $2 billion in 2019 to $24.2 billion in 2021. In the same period, the average loan size increased from $121 to $135. I suspect that this is due to the popularity of Peloton in 2020 and early 2021 at the height of Covid and the urge to go back to travel late 2021. The growth in average loan size is exactly what the lenders will sell to merchants: come to us, pay us the merchant fees and we will bring you more business.

BNPL usage rate and the number of BNPL super fans continuously rose

Per CFPB:

The quarterly usage rate has steadily increased over the past three years, reaching a high of 2.8 loans per unique borrower in Q4 ’21. In Q4 ’21, four of the five lenders surveyed had a usage rate between 2.9 and 3.2 per quarter, while the fifth had a usage rate below 2

In short, the last three years saw an increase in quarterly usage to about one loan per month per average user. This increase was slower than that seen in the upper ends of the spectrum. Specifically, the share of users with at least 5 or 10 loans per quarter reached 15.5% and 4% at the end of 2021 respectively. It’s quite surprising yet interesting to me that 4% of BNPL users used the product more than 3 times a month. I am suspecting that these high-usage users concentrate more in the young generations. With BNPL, users must be underwritten on a transaction basis. The fact that some ignore the inconvenience of filling an application 3 times a month instead of getting a credit card indicates that they cannot get a credit card. On the other hand, a debit card is always available, even to these thin-file consumers. Hence, it is a little worrying to see this kind of behavior, when there is a debt-free alternative out there.

Young consumers like BNPL and they tend to default

The surveyed lenders’ demographics data backs up my suspicion above over the credit-trapped young consumers. BNPL skews heavily towards younger generations. Even though we see more older and presumably wealthier consumers over 40 years of age, almost 50% of BNPL users are 33 years old or younger. Compared to the 2020 Census Bureau data, these young consumers are over-indexed.

Worryingly, it is consumers aged 33 or younger where we found default or charge-off most frequently. According to the surveyed lenders, 5.7% of BNPL users aged 18-24 had at least one default or charge-off in 2021 while 4.8% of users aged 25-33 had a derogatory BNPL trade. No other age group had higher than 4%. These data points show that any credit issuer wanting to underwrite thin-file consumers need to do their homework carefully in order to manage risks. This population is too big and valuable to ignore, but they are very risky!

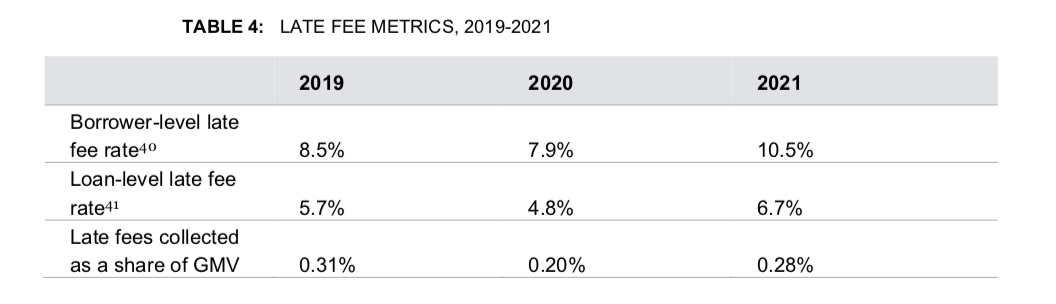

One in ten borrowers was charged a late fee in 2021

We can deduce the amount of overextension from borrowers by looking at late fees. According to the report, the borrower-level late fee rate in 2021 was 10.5%. That’s surprisingly high to me given that all BNPL lenders enforce autopay and Affirm doesn’t charge late fees. Because autopay is virtually required on every loan and 89% of all payments in 2021 came from debit cards or checking accounts, the fact that one in ten borrowers got penalized shows that many users didn’t have sufficient funds for their purchases in the first place.

Leave a comment