US Bank recently announced a new exciting addition to their personal credit card line-up and it’s called US Bank Shopper Cash Rewards Visa Signature Credit Card. Here is what you will get with this card:

- $250 bonus after spending $2,000 or more within the first 120 days of account opening

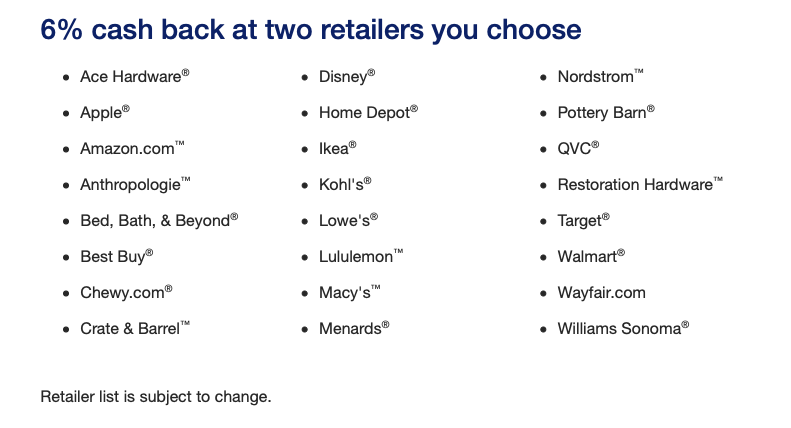

- 6% cash back on your first $1,500 in combined eligible purchases each quarter with two retailers you choose. Every quarter, you’ll have to opt in and choose two retailers, up to 5 days before the quarter ends

- 3% cash back on on your first $1,500 in eligible purchases on your choice of one everyday category (like wholesale clubs, gas and EV charging stations, bills and utilities)

- 1.5% cash back on all other purchases. In the event that your spend exceeds the $1,500 threshold at the chosen retailers and accelerator categories above, any additional spend will earn $1.5%

- $95 in annual fee with the first year’s fee waived

- Ability to use Real-Time Rewards, which allows cardholders to turn purchases into rewards and redeem rewards on purchases in real time

- Ability to use US Bank Extend Pay, which is the bank’s Buy Now Pay Later feature, for a monthly fee of around 1.6% of the balance

From a cardholder perspective, this is a seriously good card. The list of eligible retailers is impressive, featuring the most popular stores for the majority of people in America. For the sake of simplicity, let’s talk about what I think will be the most common scenario: groceries at Walmart. Spending $500 a month on groceries at Walmart is common for a family of four people. If a household’s children are all adults and everybody shares one card, it will be even easier to clear the threshold. At 6% cash back, cardholders can get back $90 on $1,500 spend every quarter or $360 every year. Even if you are a single user and spend around $1,000 on groceries at Walmart, it will still result in $240 in annual cash back. Either way, the rewards easily clear the annual fee of $95.

In addition, if you spend $200 on bills & utilities and $100 on gas every month, you can get back $9 a month or $108 a year in cash back. I drive a sedan and don’t rack up mileage, so I spend like $40/month on gas. But to truck drivers or SUV owners, this card presents a great saving opportunity. In short, with all the rewards combined with the $250 bonus offer, a cardholder can earn at least $500 in the first year with this credit card.

From a perspective of somebody who works in the credit card industry, I am excited about this new product and I would love to know how US Bank could make money from it. Let me explain. The 6% cash back category is surely a money loser for the issuer because there is no consumer interchange rate that exceeds even 3.5%. The magnitude of the loss depends on which merchants cardholders pick. Amazon and Walmart typically have an interchange rate of 0.7%, meaning that US Bank would lose $5.3 in rewards on every $100 transaction. Other retailers have high interchange rates, but they will be around 2-2.5% at the most. While EV Charging has an interchange rate of 3%+, meaning that US Bank will break even or generate some marginal revenue on this category, wholesale clubs, gas and utilities are all low-interchange categories. All other purchases that earn 1.5% in rewards should have, on average, negligible net revenue/loss for US Bank. Throw in the one-time $250 bonus offer and you can see why US Bank will definitely lose money on rewards.

The issuer hopes to negate some of the impact with the annual fee of $95, but like I explained above, it will not cover all the rewards if customers are savvy enough. The real driver of revenue and profit for US Bank will be the interest income on APR of up to 28.24%. In the credit card industry, we use the term “Transactors” to describe consumers that pay off their balance regularly and do not revolve. US Bank will get no luck from them. I suspect that the bank will try to acquire as many non-Transactors as possible, hoping that cardholders will appreciate the benefits and spend more than they can afford. To this end, there are three factors that will determine the success of this credit card:

- Keep cardholders from churning before the first annual comes up. There will be a lot of gamers who sign up for rewards and bonus before leaving to avoid having to cough up $95 in annual fee

- Educate cardholders on the benefits and how they can have a net gain despite the annual fee. That’s why there is a rewards calculator embedded on US Bank’s product page. But they should do more. Use influencers. Make the use of this credit card as relevant as possible to an average Joe. Explain to them why they should pay an annual fee to get this card instead of other cards with 5% cash back and no annual fee

- Control charge-off

I already saw online comments saying that the $95 annual fee was a dealbreaker. I totally understand the sentiment, but from an issuer perspective, the annual fee is what brings this card from “impossible to make money” to “having a chance of profitability”. As a consumer, I probably won’t sign up for this card any time soon as I don’t have a big-item purchase lined up and because my spending profile will not benefit me. As somebody who works in the credit card industry, I am excited to see what unfolds next for this product. I haven’t seen anything like it on the market for a while. It’s refreshing and definitely gives us some thoughts on how to construct our portfolio.

Leave a comment