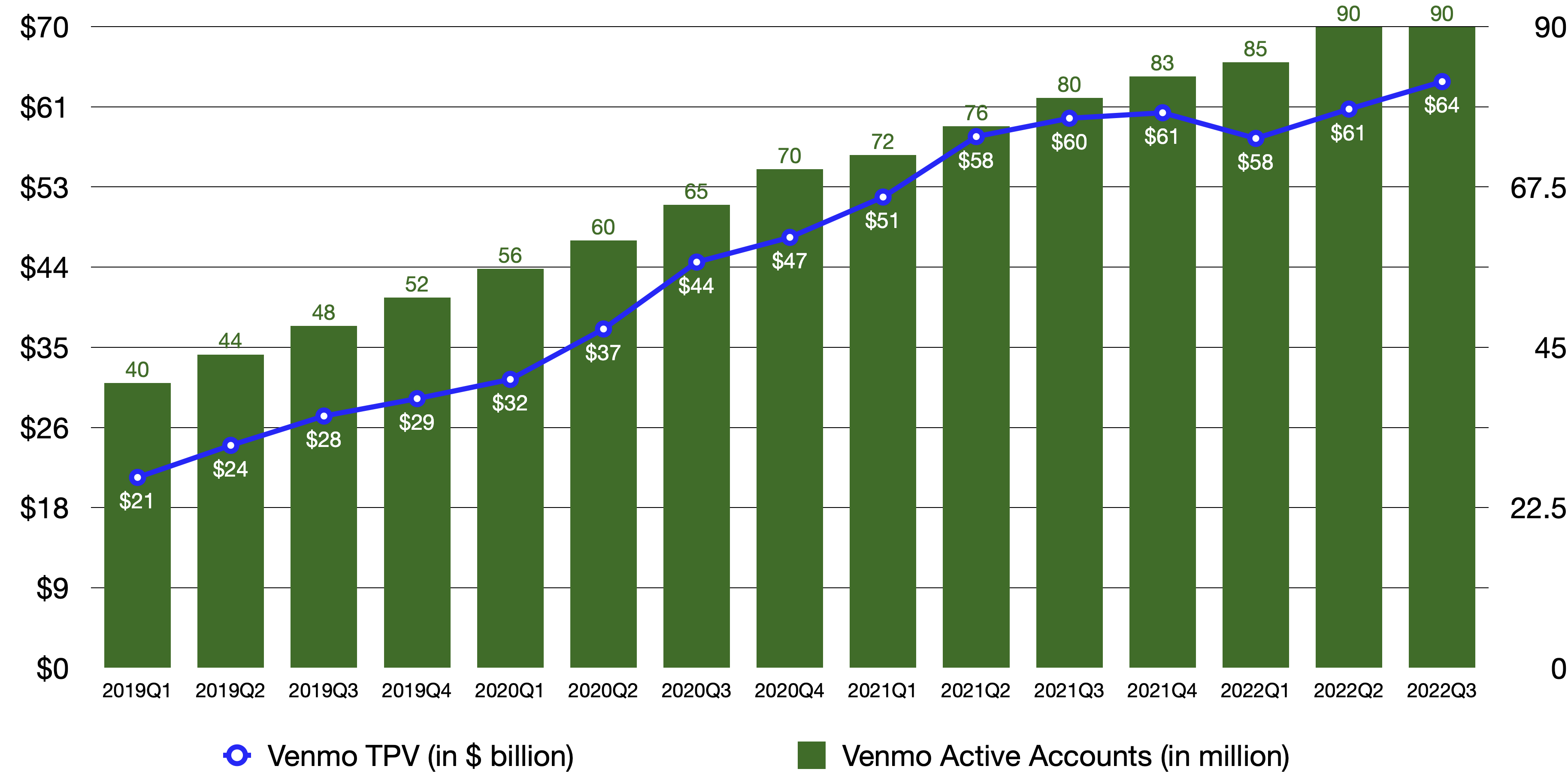

The past three years has seen a breathtaking growth of Venmo. The number of active accounts grew from 40 million in Q1 2019 to 90 million in Q2 2022. Its Transaction Processing Volume (TPV) almost tripled in the same period of time, reaching $61 billion in Q2 2022. However, growth has been hard to come by in the last two quarters, especially in Q3 2022. TPV growth was only single digit in the last two earnings reports. The number of active accounts plateaued at 90 million. Available only in the US, where there are about 230 million consumers, one has to wonder how much room there is for Venmo to continue to expand domestically.

Going overseas sounds like a straightforward answer, but operationally, it is anything but. It would require a lot of investments in localizing the product, marketing to acquire customers, customer management to maintain engagement and compliance to stay on the good side of lawmakers. There must be a reason why PayPal hasn’t taken Venmo outside of the US. Given the missteps that the management has taken over the last few years, it’s not impossible that restricting Venmo to the US is a mistake. Personally; however, I can see why they haven’t.

If growth in TPV and user base slows down, what about monetization? PayPal reported that Venmo earned $250 million in revenue in Q4 FY2021 and $900 million in FY2021. Since Venmo processed almost $61 billion and $230 billion in TPV in the same periods respectively, Venmo’s take rate is about 0.4%. To put that take rate into context, let’s compare it to Cash App

| Venmo | Cash App | Note | |

| Monthly Active Accounts (in million) | 57 | 49 | the Cash App number is the number of transacting accounts in September 2022 |

| Transaction Volume (in $ billion) in the quarter ending Sep 30th, 2022 | 64 | 4.3 | |

| Revenue (in $ million) in the quarter ending Sep 30th, 2022 | 270 | 118 | Venmo’s revenue is my estimate based on the $250-million figure reported for Q4 2021 while Cash App’s revenue only includes transaction-based revenue |

| Take-rate | 0.42% | 2.7% |

The comparison shows that Venmo is seriously under-monetized compared to Cash App. PayPal has a valuable asset in Venmo that resonates with a lot of consumers in America, especially the younger crowd, but they don’t seem to be able to benefit from said asset. And don’t take my word on it as the CEO of PayPal is not entirely happy either

I am pleased with Venmo’s progress but I am not thrilled with all the progress that we’ve had. I just want to be up front with that. I feel like we can do a lot more with that asset than we have been able to do so far. There is a ton of potential there. The people who use Venmo, our customers love Venmo. It is a beloved brand. They use it all the time. You can tell from our monthly active users [of 57M]. The monthly active users are up by ~85% in the last 2 years or so. So, a lot of progress there. But I feel like there can be more progress.

These are some big merchants that are implementing Pay with Venmo and I think we will see more. We are going to revamp the card strategy, we started to begin to do that. We think that is one place that Cash App has done particularly well on, and there is no reason why we should not with our scale and size be able to really tap into a revamped card functionality. Over time, we will also begin to see more basic financial services there, savings and other things come into the Venmo wallet. There is focus on things that have to get done right now. Amazon and Apple are big opportunities, we want to make sure we take full advantage of those. We’ve got some basic hygiene work to do there. Good progress, but I wouldn’t call it great progress right now. In terms of revenue growth, we had anticipated that we would be about 50% revenue growth [for FY’22] and that is where we are year to date. Q4, like the rest of the business, is going to be weaker than we expected. That will probably take Venmo revenue growth into the 40%’s [year over year growth for FY’22]. That is probably a good place for you to assume it will end

Source: PayPal Third Quarter 2022 Buyside Call

Platforms like Venmo and Cash App monetize by charging sellers on every transaction and the majority of retail sales still takes place in stores. To facilitate in-store transactions, cards are the most successful medium. PayPal put a lot of efforts into QR Code during the pandemic, but they abandoned that push and have since switched focus to cards. Venmo credit card doesn’t require a Venmo balance, but it’s not available to every consumer, especially Gen Z users whose lack of credit history prevents them from qualifying for a credit card. I wouldn’t be surprised if Venmo credit card users constituted only a small percentage of Venmo active base.

While accessible to many more people, Venmo debit card requires a Venmo balance. The question then becomes: how can Venmo get users to park money on a Venmo account? Users only maintain a balance when there is enough utility, whether it’s rewards or accessibility at a variety of merchants. Cash App has been successful so far in this regard. Cash App reported that it had $2 billion of direct deposits in September 2022. Paper direct deposits into Cash App which was launched nearly a year ago cumulatively crossed $3.5 billion. These figures indicate how much Cash App users value the platform and how much they want to use it. This is something that Venmo has to, at least, replicate and there certainly is work to be done.

Cash App users can paper-deposit funds into their accounts at some retail stores, but Venmo doesn’t have this feature. Checks deposited electronically into Cash App will be available on the platform the next business day at no additional cost. With Venmo, users may have to wait up to 10 days to receive funds from an electronic check unless users pay a small fee to expedite the process. Any additional friction to the deposit process will deter users from bringing cash to the platform, so obviously I’d love to see Venmo at least get feature parity with Cash App.

Moreover, Venmo also needs to be available at more checkout pages. The partnership with Amazon which enables customers to add their Venmo account as a payment method will likely boost the perceived utility of Venmo. But there should be more partnerships like that. PayPal powers payments for some of the largest merchants in the US, whether it’s the branded PayPal or the unbranded platform Braintree. They should look into leveraging such an advantage to make Venmo more prominent. If a user could pay for Uber, Amazon or Instacart with their Venmo balance, that would obviously make Venmo more useful and appealing.

There is also a side benefit from having more customer funds. The more funds the likes of Venmo or Block have, the more interest income they can earn. In Q3 2022, PayPal’s Other Value Added Services revenue increased by $37 million year over year. One of the main drivers of such an increase was higher interest income on customer funds due to higher interest rates. Block itself made $7 million in revenue from customer funds as well.

Next, rewards is a great tool to keep consumers engaged. Consumers love to earn rewards and redeem them for other purchases. PayPal recently revamped their rewards program that unifies all PayPal products and offers consumers more ways to earn and redeem. However, since Venmo and PayPal are still two independent platforms, the new PayPal Rewards does not feature Venmo. If consumers are expected to use Venmo for payments, they will expect to be rewarded for such loyalty. Besides Venmo credit card’s rewards, Venmo offers cash back at qualifying merchants on Venmo debit card, but information on that is scant. Venmo needs to make the program more attractive and prominent. Yes, the low interchange rate on debit card transactions makes it expensive to fund rewards, but it’s also expensive, if not more, to acquire new customers and fend off Cash App and a host of other competitors.

Here are a couple of things that Venmo can do. First, link the credit card with the debit card, Any credit card rewards can be turned to cash on Venmo account that can be used to pay friends or purchase at stores with the Venmo Debit Card. This concept is not something new. It’s similar to what Apple has with Apple Card and Apple Cash. By making the credit card rewards immediately available, Venmo would give users a reason to use the Venmo app and debit card.

Second, because Venmo Credit Card is a co-branded card issued by Synchrony, Venmo must receive some compensation, either as share of interest and/or interchange income and finder’s fee for every new account. Financial reports by PayPal indicate that the compensation could run in the millions. Use that money to run marketing campaigns with a celebrity. I’d love to see Venmo try to do what Capital One did with Taylor Swift. Capital One generated a lot of accounts, interest and awareness with this campaign.

In short, Venmo is an incredible asset that PayPal has at its disposal. Investors place a premium on the company’s ability to monetize Venmo, but even the CEO is not happy with what they have done. Compared to Cash App, it’s under-monetized. PayPal needs to start making more progress soon because their competitors don’t stand still for them to catch up.

Leave a comment