McKinsey just released a long yet insightful report on global payments. If you haven’t decided whether to spend time on reading it fully, here are my notes

Asia’s payment revenue is half of the global payment revenue

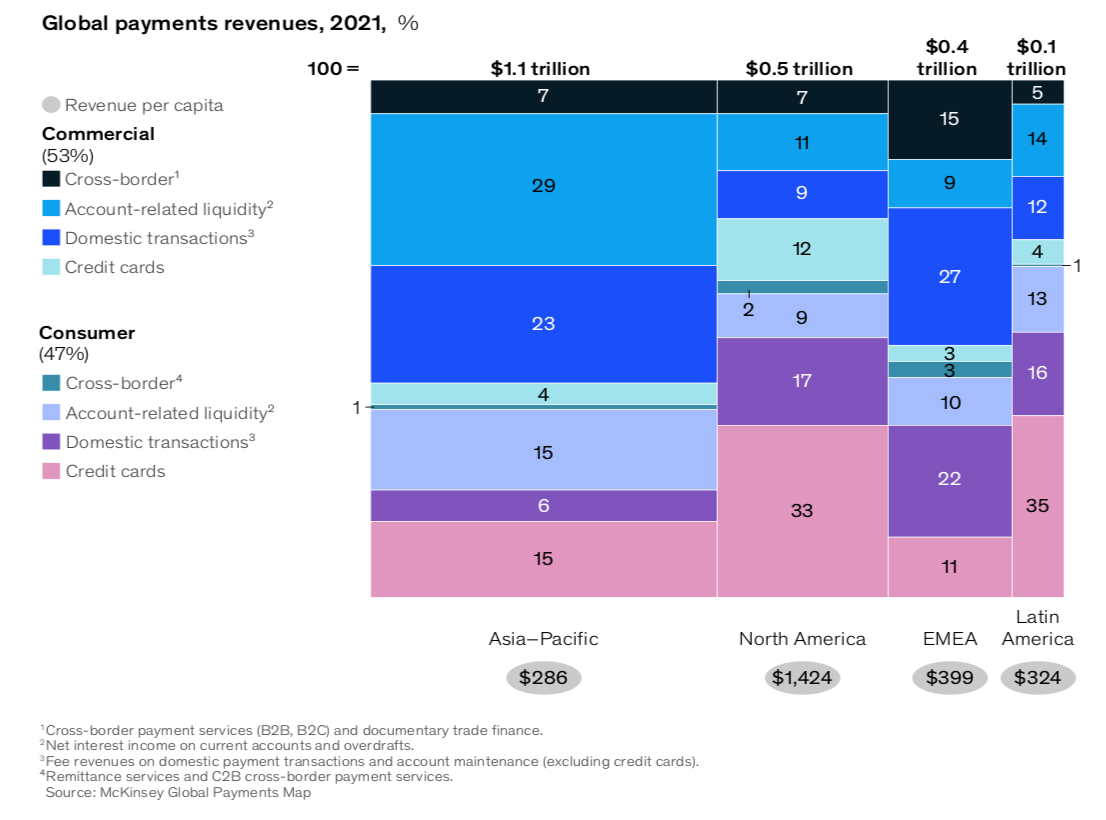

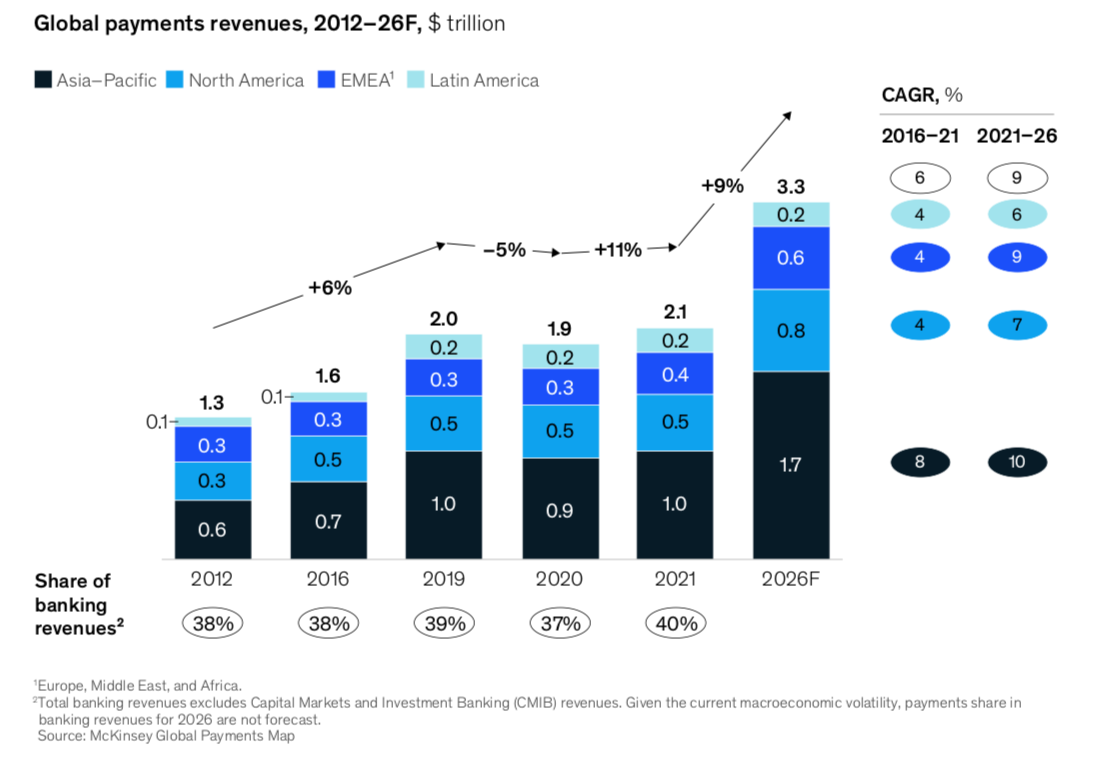

In 2021, payment revenue in Asia reached $1.1 trillion and was as large as that of the rest of the world combined. North America has the highest revenue per capita at $1,424. The composition of payment revenues varies from region to region. Half of North America’s revenue came from Consumer and credit card made up 50% of all Consumer, the same trend observed in Latin America. Meanwhile, Consumer was only 37% of all Asia’s revenue. McKinsey predicted that global payment revenue would grow by 9% every year between now and 2026, with most of the growth stemming from Asia and North America.

Cash usage varies, depending on where you look

Cash is not a popular payment method in Europe and especially some countries like Norway, where the usage dropped to 3%. The pandemic accelerated the process to move away from cash in Czech Republic and Greece, where the use of cash dropped by 12 and 15 percentage points between 2019 and 2021. On the other hand, hard cold cash is still the most popular in other areas. In Africa, 95% of all transactions in 2021 involved cash. Cash still dominated in-person point-of-sale (POS) transactions in Southeast Asian markets. It made up 63%, 54%, 51% and 48% of POS transaction value in Thailand, Vietnam, Indonesia and Philippines respectively. In Latin America, the figure was 36%.

This presents a huge opportunity for growth to the likes of Visa or Mastercard and future fintechs.

Central Bank Digital Currency

Roughly 90 percent of the world’s central banks are pursuing central bank digital currency (CBDC) projects. Some, including those in the United States and South Africa, are at the exploratory phase; others are development projects (the European Union) and pilots (China). In some locations, including Nigeria and the Bahamas, solutions are already operable, and central banks are looking to expand. Despite the high level of activity, most CBDC initiatives today remain in the nascent stages of market development and, in many cases, even technical design.

CBDCs differ fundamentally from other forms of digital coins in that they are directly backed by central bank deposits or a government pledge. Therefore, they offer stable value and can aim to combine benefits in the areas of trust, regulatory stability, and audit transparency. CBDCs can be deployed under a variety of technology models, depending on a central bank’s desired objectives and use cases. CBDCs do not necessarily rely on decentralized technologies, as they can be administered by central bank agents as well as distributed via digital-ledger technologies. They can be held on physical devices such as cards or phone wallets or exist as a purely digital book entry. They can be issued as stand-alone tokens (stored at any of multiple carriers) or as account-based assets held directly at the central bank.

Wholesale CBDCs mostly target financial institutions (banks and nonbanks) and large corporate treasury centers as their primary users, and they aim to improve the efficiency of settlements—both payments and securities, domestic and cross-border. This may or may not involve providing nonbanks with direct access to central-bank accounts.

Retail CBDCs target consumers and local businesses as end users, with possible use cases including disbursement of social benefits, an alternative to cash for e-commerce point-of-service and bill payments, and enabling of seamless peer- to-peer transactions for banked and unbanked users. In more complex initiatives, CBDCs combined with smart contracts,6 such as the Bank of Israel’s initiative, aim to improve payments convenience. Examples include payment of sales tax directly to tax authorities at point of sale and automated distribution of social benefits for economic relief conditioned on the recipients meeting defined requirements.

Nigeria became the first African country to introduce a digital currency with the October 2021 launch of retail CBDC eNaira. Its intended bene- fits include faster and more equitable distribution of cash assistance to households and communities participating in social welfare programs, lower transaction costs and faster settlement, efficient cross-border transaction capabilities, and traceability and security to limit fraud. The eNaira app garnered almost 800,000 downloads in the first seven months following its launch. According to some reports, half of those downloads have not been activated. Merchant adoption of digital currency has been similarly limited, with fewer than 100 active retailers accepting eNaira payments as of May 2022—a small number, given Nigeria’s status as Africa’s largest economy.

The low initial uptake of eNaira has been attributed to limited knowledge of the CBDC and how it functions, fear of exposure to security breaches, and poor internet access in some regions. In response to these challenges, the Nigerian government recently announced that eNaira will be made available on feature phones via Unstructured Supplementary Service Data (USSD), which will expand the potential market by 100 million citizens on top of the current 25 million to 40 million smartphone holders.1 The government also recently sponsored a hackathon to promote visibility and identify key feature and technology improvements.

Instant Payments

Instant payments are inching towards the inflection point of mass adoption. Usage doubles annually in countries like India, Spain and Thailand, increases by 50% every year in Australia and Singapore, and grows at double-digit rates in China and the UK. In India, UPI has 260 million users, 300 registered banks and 6 billion transactions a month. In Brazil, Pix has reached half of the population and more than 775 registered institutional participants, including banks, government agencies and others. In the US, instant payments’ growth rates have exceeded 60%, but the volume is relatively small.

Wallet

Digital wallets play an important role in consumer life and payment landscapes in several markets across the globe. In the Philippines, Vietnam and Indonesia, wallets account for 31%, 25% and 39% of transaction value respectively. In the Philippines, the majority of adults in the country are users of the top two wallets, GCash and Maya. In Brazil, 70% of the respondents to a recent survey said they use digital wallets, even though the transaction value and frequency still remain low.

To offer more utility to users and find revenue, wallets look to partnerships and other areas beyond just payment. Ride-hailing apps like Gojek and Grab go into groceries and other categories with higher ticket size. In Africa, M-Pesa forms partnerships to offer services in e-Commerce, travel, health, agriculture and other areas in order to become a Super App. In Latin America, Rappi, which is a Colombia-based Uber-like service with more than 30 million users, adopts the same approach and offers e-Commerce, insurance and loyalty points. In Vietnam, Momo is a formidable and popular wallet. Shortly after launch, Momo partnered with every telecommunications network in the country to enable airtime top-ups as the strategy to acquire users and grow. Since then, the partnerships and Momo’s business have expanded. Nowadays, Momo is everywhere in major cities like Hanoi or Ho Chi Minh City. You can pay for a bowl of soup on the street by asking the merchant for their QR code. Plus, users can buy a lot of things such as online-gaming credits, airline tickets or movie passes.

In the Philippines, in order to provide more utility to users, GCash launched GSave and GInvest to enable savings and investments on its app. The recently launched Maya app follows the same playbook. In India, Paytm is now a functional bank which can broaden its offerings to lending products.

We will undoubtedly continue to see the growth of wallets everywhere in the world. But they are all under pressure to deliver profitability, not just growth. The question then becomes: can they become profitable like incumbent banks faster than banks can gain feature parity?

Other observations

Debit cards have extended their lead as the most used card product, with 94 transactions per capita globally, versus 49 for credit. The share of debit card among overall electronic transactions is highest in Russia (84 percent), followed by Norway, Ireland, and Romania (each roughly two-thirds).

The digitization of commerce and business management has massively expanded opportunities to embed finance in nonfinancial customer experiences. As much as 33 percent of global card spending—50 percent in the US—now takes place online, with a large portion of small and midsize companies in the US relying on software solutions for managing their business.

10 percent of UK adults reported holding, or having held, a crypto asset. The European Central Bank (ECB) has indicated that as many as 10 percent of households in six large EU countries owned digital assets. And roughly one-fifth of respondents to a McKinsey survey—22 percent in India, 20 percent in Brazil, and 14 percent in the US—reported that they held digital assets as part of their financial portfolios

Globally, between 2018 and 2021, the number of noncash retail payment transactions have increased at a compound annual growth rate of 13 percent; while in emerging markets, that figure is 25 percent. Some of the fastest growth occurred in emerging markets in Africa (Morocco, Nigeria, and South Africa) and Asia. Strong growth is expected to continue in some emerging markets over the next few years, with projected CAGRs of 15 percent between 2021 and 2026.

Leave a comment