If there is one long-term (the keyword here is long-term) Covid beneficiary, that’s Uber. The company looks to be in a better shape than ever. Here is why

Bookings & revenue skyrocketed

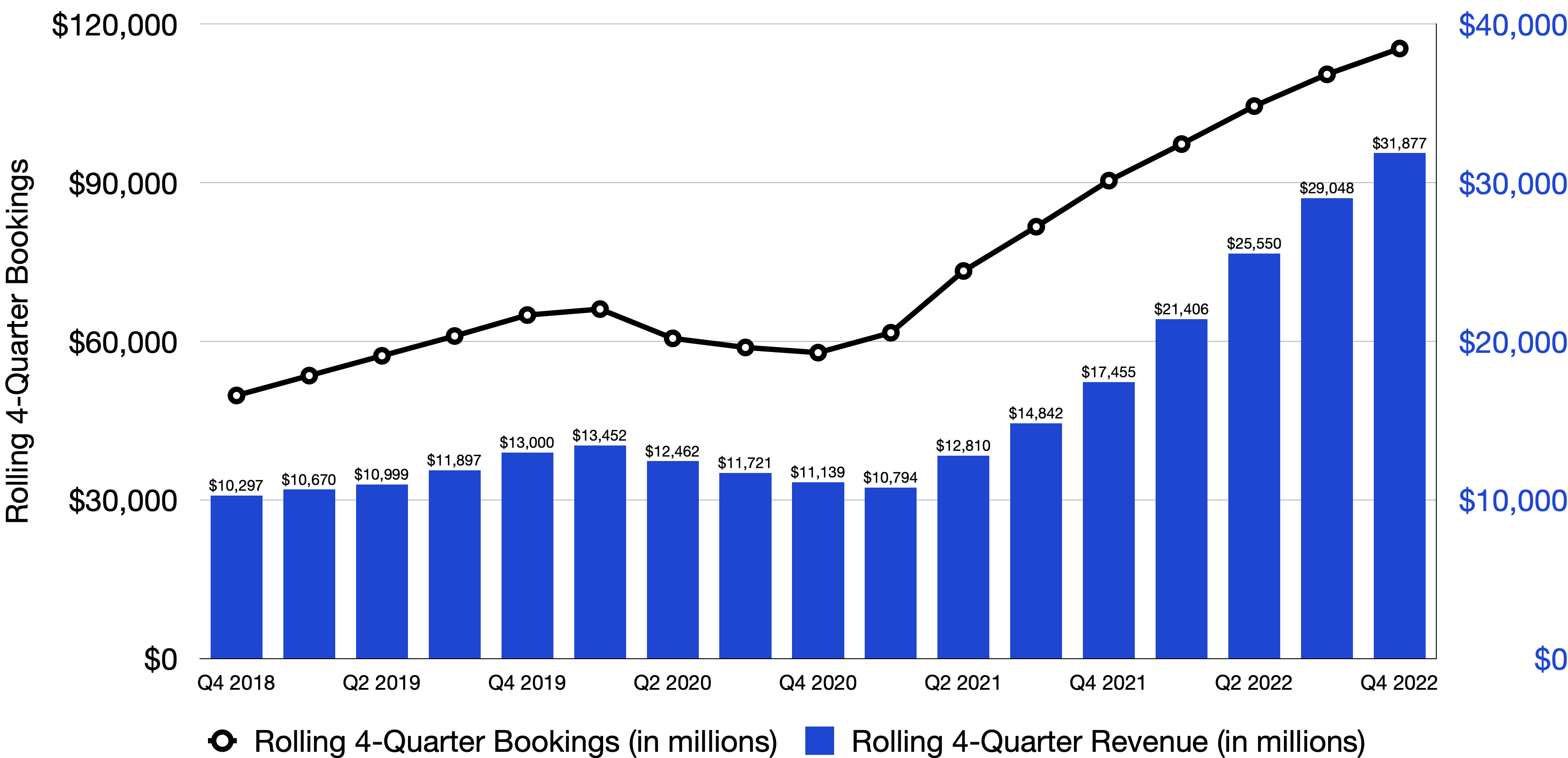

At the end of 2018, Uber generated about $50 billion in bookings and $10.3 billion in revenue every four quarters. Fast forward to the end of 2022, they reached $115 billion in bookings and $32 billion in revenue. In other words, bookings more than doubled and revenue more than tripled between 2018 and 2022. That’s some serious growth. To put it in perspective, Lyft made $4.1 billion in revenue in 2022, only 14% higher than what they recorded in 2019 (earliest year Lyft reported results publicly). The stock plummeted after a disappointing earnings call and a weak guidance early this week. What a stunning different the last few years made! Before Dara took over, Uber took one PR thumping after another. Hashtag #DeleteUber trended on social media a few times. Lyft became a serious threat. Nowadays, the pink company is barely hanging on while Uber is stronger strategically than ever.

Used to rely on Mobility, Uber now has two equal businesses

Everyone knew Uber as a ride-hailing company. Its whole business used to revolve around transporting folks from one place to another. In 2014, Uber Eats was launched, but it was tiny compared to the cash cow Mobility. Covid-19 changed everything. While Mobility took a dive as folks limited their movement to the outside world, Delivery rose and, as of December 2022, rivals Mobility in Bookings. Having Delivery is absolutely crucial to the company’s survival and growth for the following reasons:

- Delivery brings more earning opportunities to drivers and as a consequence, Uber attracts more drivers and retains them better. In fact, Uber just posted monthly active drivers at all-time high. More drivers mean shorter waiting time and higher customer satisfaction.

- A bigger driver pool also means that merchants see more deliveries out of the door and get to consumers faster. More merchants make the whole Uber ecosystem healthier and more robust.

- I don’t wish to ever see another pandemic like Covid again, but nobody can dismiss that possibility completely. Having a business like Delivery reduces the overall risk exposure for Uber. Just ask Lyft about it.

Uber has not yet made money, but it’s getting there

One major criticism of Uber, mostly deservedly, is that the company has not delivered profits. Which business gets to $33 billion in annual revenue with zero profit? To be fair to Uber, the task is exceedingly difficult given the circumstances. Dara stepped into the CEO’s shoes with the mandate to restore Uber’s public image and bring adult leadership. Then, Covid happened, decimating the cash cow Mobility service. Then, he had to deal with the post-Covid consequences: driver supply & inflation. And let’s not forget about competition from the likes of DoorDash, GrubHub and Instacart. Navigating through all those challenges with a global operation is not easy.

Hence, it’s encouraging to see the transformation of Uber’s business and the stride it took towards profitability. For the past four quarters, on an adjusted EBITDA basis, both Delivery and Mobility were in the black. I understand the gripes (again deservedly so) that many have about EBITDA metrics, but the point lies in the intent and execution that Uber’s executive showed. Here is Nelson Chai, the CFO, on the topic:

Our call to action moment was actually in 2020. And if you recall back then, our Mobility business was over 85% of the company’s gross bookings. And as we sat here in April of 2020, that business was down 80%. So as you recall, we acted pretty decisively during that time, we took over $1 billion of costs out of our infrastructure. We shuttered down a bunch of businesses. And unfortunately, we did have to let go over 20% of our headcount.

So we’ve been really focused on efficiency since then. I think you’ve heard us lay out our plans, and I think Dara mentioned on CNBC, in 2021, we wanted to really push hard for EBITDA profitability, and again, we achieved that metric in 2021. Last year, we talked about being free cash flow positive at some point in the year. And again, we achieved that metric. And now, we’re talking about being GAAP operating profit at some point later in the year. And we expect to continue to achieve that metric.

Now we’ve done this — and you mentioned incremental margins, we’ve done this because we focused efficiently on cost, and we’ve been laser-focused on it. So our headcount will largely be relatively flat this year. And even if you go back to the build that the many companies had over the past few years, we’ve grown our headcount about 10%, excluding the Freight business, over the period of time. And our gross bookings went from $62 billion in 2019 to $115 billion last year. So just think about that growth and efficiency. Where we’ve hired heads has been in some areas of tax, selectively, as well as some sales folks on the Delivery business.

Uber was one of the notable tech companies that haven’t announced a layoff. What the executive team told analysts and investors about EBITDA profitability and free cash flow in 2022, they delivered. Growth looks the exact opposite of rival Lyft. These instances have earned Uber’s management team some benefit of the doubt in their quest to reach unquestionable profitability.

Other updates

- Advertising: As of December 2022, 35% of merchants have become advertisers on the platform. The ads business has annualized run rate of $500 million, only half way to the target of $1 billion by FY2024. Given the high margin of the ads business, Uber would love to scale it as much as they can. However, they will have to be mindful of the detrimental impact that high ads load can do to user experience.

- The flagship subscription Uber One as of December 2022 had 12 million. The company reported that members spent 4.1 times more than non-members and were 15% more likely to stick around. This type of users with their concrete intent to purchase will be something that merchants covet.

- Freight generated almost $7 billion in revenue and was profitable on adjusted EBITDA basis from Q1 to Q3 this year

In short, I believe Uber is in the strongest position than ever. It managed to not only survive the pandemic, but also took advantage of the unique opportunity offered. Talk about never letting a crisis go to waste! The company still has a long way to go towards its long term goals, but the foundational blocks are there. The opportunity is there. All it takes now is disciplined execution. To that end, the management team has demonstrated that they can.

Disclaimer: I own Uber in my personal portfolio.

Leave a comment