Because my daily job is related to credit card, today I will pull back the curtain a bit and talk about 10 areas where a credit card issuer can do to either maximize revenue or reduce expenses. This list is by no means complete. Rather, it includes the main tactics that I have come to know or worked on myself. If you’re curious about some insider knowledge, read on!

APR Optimization

A credit card is an unsecured loan. For every one dollar in past-due balance, the higher APR, the more revenue an issuer makes. A go-to APR usually consists of a Prime rate and a margin rate. When interest rates stay elevated like they are now, they increase the Prime rate and as a result, the go-to APR.

Some credit card portfolios use fixed pricing, offering the same APR to every customer regardless of the risk profile. Other portfolios opt for variable pricing that adjusts APR based on a customer’s credit history. In an inflationary environment like what we are experiencing now, variable pricing is the better option for revenue management.

Though increasing APR can help grow the top line, issuers need to be mindful that high APRs can turn off customers.

BT Fee

A common tactic in the credit card industry is to allow customers to transfer outstanding balance from another issuer at 0% APR for a certain period of time. Though interest-free, these Balance Transfer (BT) offers carry a fee of 3% – 5% of the BT volume. An increase of 1% in BT fee can result in a significant lift in revenue. Again, issuers must be mindful that increasing the BT fee rate too much can make their card less competitive in this fragmented market.

Reduce The Size Of Direct Mail

Direct Mail is still the primary acquisition channel for a lot of issuers. At high volume, this channel presents an area primed for expense optimization. Even a reduction of one page from the mail package can mean thousands of dollars in savings, if an issuer mails like 20 million pieces a month, a figure that is not uncommon in this industry. Hence, Marketing can work with Compliance and see what can be cut from a mail package while staying compliant with all regulations.

Many Direct Mail prospects apply online. In other words, after retrieving the piece from their mailbox, these prospects go to an issuer’s website, key in the access code and apply. The begs the question: is it necessary to include a paper application and a pre-paid envelope? Removing such elements means a reduction in postage and paper expenses. However, issuers must try to avoid disregarding senior prospects who may appreciate the option of a paper application.

Paperless Statements

Issuers can persuade customers to opt for e-statements instead of paper statements. Fewer papers mean lower expenses.

Interchange Optimization

Before we talk about interchange optimization, if you need a refresher on interchange, click here. Major card networks like Visa or Mastercard have multiple plastic tiers (it’s actually BIN tiers, but I call it plastic tiers so that I won’t confuse anyone) for both consumer and commercial accounts. Higher tiers come with higher interchange rates which bring in more interchange revenue for issuers. For instance, the same $100 purchase may produce $1.8 in interchange for Visa Classic, but for Visa Signature, it may bring in $2 in interchange. The difference is small, but if a portfolio generates billions of dollars in spend, interchange optimization can result in a serious lift in revenue.

Instant Issues

In some cases, customers can receive functional credit cards instantaneously after approval. We call them instant issues. Instant issues usually happen at a bank branch (like a Bank of America or Chase branch) or a partner’s store (such as a Target or Best Buy). To an issuer, an instant issue costs less than an ordinary plastic that needs to be printed and sent via the post office. Therefore, instant issues can save an issuer some Embossing expenses.

Informed Delivery

Informed Delivery sends us a notification in our email on what mails we are going to get every day. To improve the feature, USPS works with ferocious mailers like credit card issuers and courts their support in exchange for a discount on postage. As of this writing, I do know that the discount is still going on. From an issuer point of view, informed delivery doesn’t increase response rates in a direct mail campaign, but it does help reduce the postage expense.

Plastic Management

Depending on materials and design, the production cost can vary from one card to another. For instance, a metal card is more expensive than a plastic one. A complex design costs more than a monochromatic version. Some issuers even let customers design their own cards (DYC); which can lead to higher expenses to accommodate customized requests. Halting the DYC program or curbing on complex designs can help lower expenses.

Increase Deposits

Credit card issuers have to borrow money from the Federal Reserve in order to lend to consumers. The cost of borrowing that money is called Cost of Funds (COF). The higher the interest rates, the higher the COF. To minimize that expense, issuers must raise as much money on their own and borrow as little as possible. That’s why you see that in this environment, banks race to accumulate as many deposits as they can, even if they have to pay consumers higher interests than they usually do. It’ll still be cheaper than borrowing from the Fed.

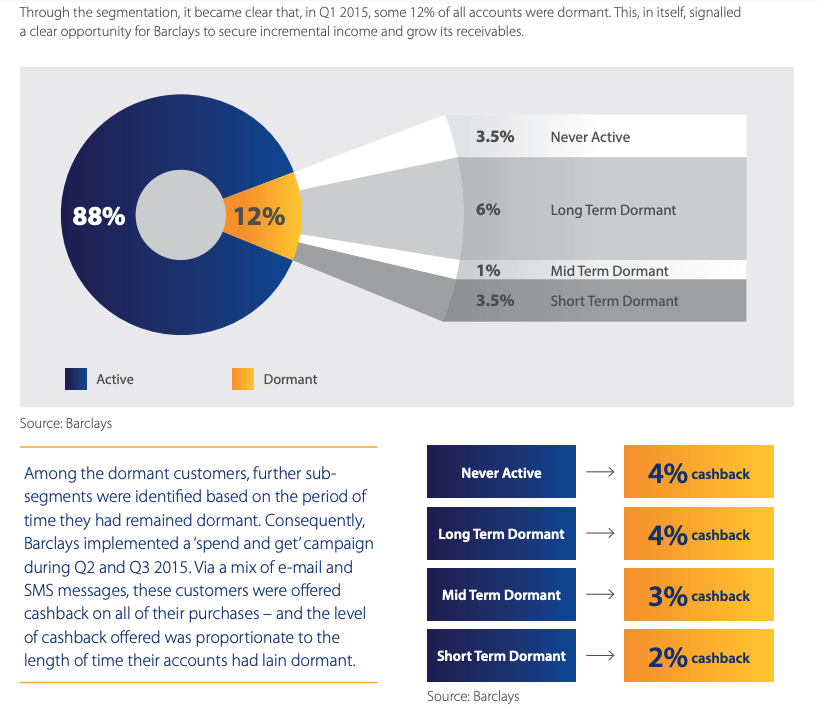

Reactivate Dormant Accounts

Issuers want their accounts to be as active as possible. When an account spends, its issuer receives interchange revenue. When an account revolves, its issuer generates interest income and late fees. Hence, issuers run trigger campaigns once in a while to reactivate accounts that don’t register any activity for a while. Also, the old adage that it’s cheaper to retain a customer than to acquire a new one still rings true in this case.

Leave a comment