What is Visa+? How does it work?

A couple of days ago, Visa introduced a new service aimed to facilitate payments between different payment apps. Per the press release:

Visa announced it is partnering with PayPal and Venmo to pilot Visa+, an innovative service that aims to help individuals move money quickly and securely between different person-to-person (P2P) digital payment apps. Later this year, Venmo and PayPal users in the US will be able to start moving money seamlessly between the two platforms.

Visa+ will not require users to have a Visa card; instead, by setting up a personalized payment address linked to their Venmo or PayPal account, individuals using either app will be able to receive and send payments quickly and securely between the platforms.

As part of a joint effort to build interoperability across payment platforms, Visa partners DailyPay, i2c, TabaPay and Western Union, will also integrate Visa+ within their platforms. Through this collaboration, Visa+ will expand its reach and enable more use cases, including gig, creator and marketplace payouts. Participating digital wallets, neo-banks and other payment apps, reaching millions of US users, will be able to enable interoperability through Visa+.

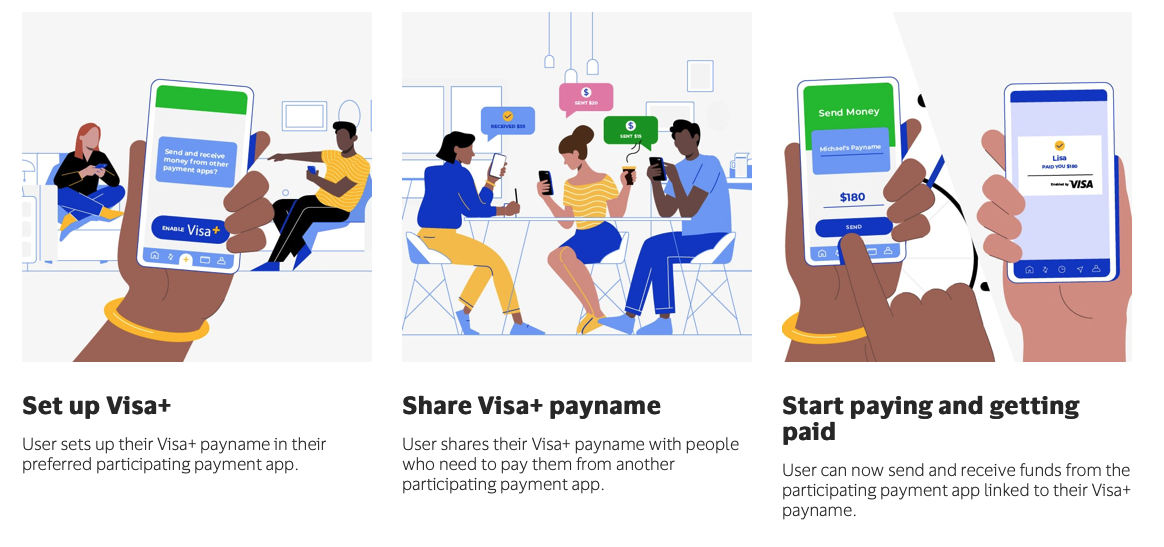

This is how Visa+ works. Users of participating apps will see an option to set up their Visa+ paynames. These names will be unique and work across the Visa+ ecosystem. Let’s say: I pick Nebraskan2023 as my Visa+ payname on PayPal. My friends who are Venmo users can send money to me on PayPal from their Venmo accounts using that payname. On the other hand, I can send money to then from my PayPal account to their Venmo’s as well. My PayPal balance will reflect the money sent to me and by me. It’s that simple.

From Visa perspective

In my opinion, it’s all about enabling more flows on Visa rails and making more money. When a small business disburses pay to its employees, it can take place on non-Visa rails, something that the network can usually do little about. With Visa+, they now can direct some of those flows back onto the Visa ecosystem. If a small business’ owner decides to pay workers from his PayPal balance or balance of his checking account at a neobank using Visa+, the payout will be on Visa rails. If a marketplace platform uses Visa+ to pay gig workers or content creators, that’ll be on Visa rails too. With names like Uber, AirBnb or TikTok, you can see the potential size of these flows. It can be hundreds of billions of dollars.

For the kind of transactions between payment apps, Visa charges the institution initiating transactions between $0.025 and $0.01 per transaction. In the beginning, it’s likely going to be immaterial to Visa’s bottom line, but who’s to say what it could be in the future when the service attracts more partners and is available in more countries? And like I said above, when Visa expands the use cases, their benefit can grow multifolds.

To make Visa+ work, the network needs to solve a chick-and-egg problem. Partners only join when they recognize the value that Visa+ brings to consumers. Consumers will only use the service when there is utility, especially beyond just exchanging money between payment apps. Take PayPal and Venmo as an example. These two platforms allow Visa+ users to use the funds on their PayPal or Venmo balance at the stores with PayPal or Venmo Debit Card or on a website through PayPal checkout. That’s extra utility that Power PayPal/Venmo users may like.

From partner perspective

For fintech platforms, it is really helpful to maintain and grow deposits. Take PayPal as an example. The more users maintain balance on their PayPal account, the more likely these users will use PayPal to transfer money or make payments. Plus, PayPal can earn interests on these deposits and incur lower expenses on transactions, compared to those facilitated through a debit or credit card.

For those that already signed up to partner with Visa, their intention is to use Visa+ to increase consumer balance and platform usage. For those that have not signed up yet, with notable exclusions including Cash App and Apple Wallet, the question becomes: is Visa+ a net benefit? Let’s pick on Cash App a little bit here. Becoming part of the new service means that Cash App power users will be less likely to sign up for PayPal. But using the same logic, participation also means that PayPal users will be less inclined to use Cash App. I don’t know which way this issue is going to go. But given Cash App’s popularity, their absence at the launch may mean that they considered joining Visa+ not beneficial enough.

From incumbent banks perspective

Given the way Visa+ works and how much payment apps want to keep money within their walled gardens, banks’ deposits will take a hit. Zelle is likely to be affected too. I doubt the impact will be sizeable at first, but bank executives may want to watch this space. The more value payment apps offer consumers and the bigger the Visa+ ecosystem, the bigger the hit to their deposits will be.

Leave a comment