The renowned venture capital firm, a16z, recently published an article named “The Future of Payments is… Red?“, whose content I find at best unconvincing. The gist of the article is that the author believed fintech startups could challenge the two dominant networks (Visa & Mastercard) by pushing for ACH transactions to replace credit cards. The example used to substantiate the thesis is Target Red Card. Per the article, and sorry for the lengthy excerpt:

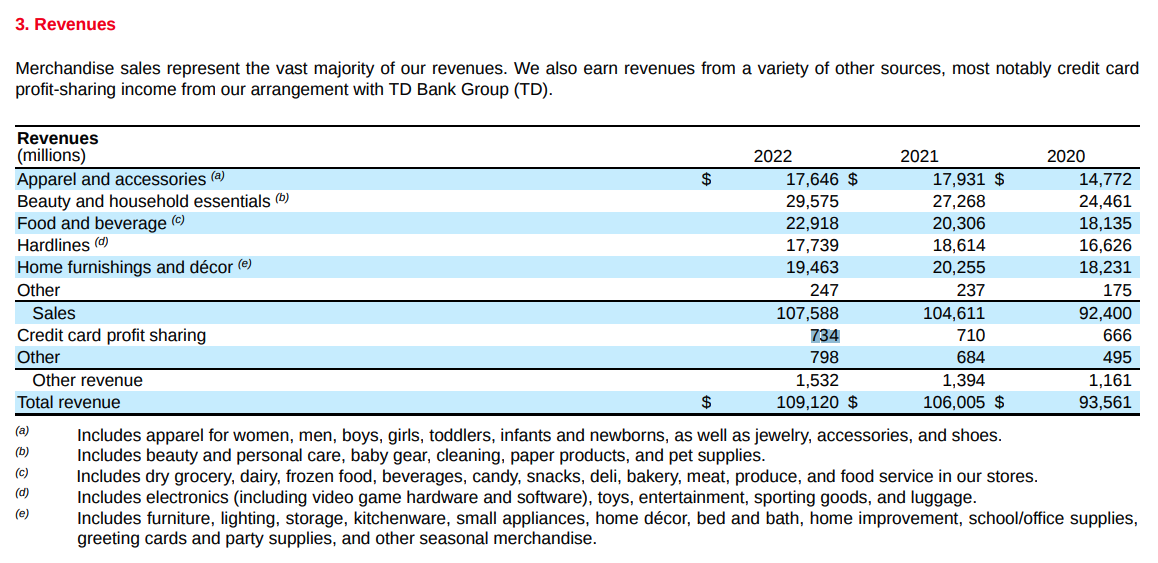

Look at Target’s full-year revenue for 2022: they made $107.6 billion in sales and $3.4 billion in pre-tax income. Now imagine if every transaction at a Target store or at target.com were made with a credit card—which is currently not the case—at an average fee of 2%. This would result in $2.2 billion in incremental income if all payments shifted to ACH, which would be 65% more profit!

Target has impressively shifted 20% of their entire sales to their own cards. The only “illogical” part of this is that to save ~2%, the company is… giving up 5%, albeit to the user in the form of direct savings at Target, which is the primary benefit of the RedCard.

Target isn’t an outlier here. Most “frequent interaction” or high-frequency billing companies do the same. Verizon and AT&T, as additional examples, give you substantial monthly savings for moving your bill-pay off of credit cards and to ACH (or sometimes debit cards, given the lower average fee).

That said, while I think Target has been smart to roll this out, paying 5% to save 2% (and justifying it by showing increased engagement, which likely reverses cause and effect and shows sampling bias!) is not smart. A better alternative, in my opinion, would be to provide customers with a one-time benefit to make the switch. As an example, imagine if Netflix started offering such a benefit and started offering customers, upon log-in, a $2 one-time discount if they clicked and switched their payment method to direct debit. This would provide Netflix with long-term savings of more than $100 million a year in North America alone, based on their rough interchange costs.

Luckily, inertia, one of the twin moats that protects so much of banking, is now decreasing thanks to improved technology, and consumers are more willing to switch up their payments methods. (Rewards, the process by which merchant fees fund customer benefits, with banks in the middle, remains a stubborn reason why “RedCard as a Service” hasn’t previously taken off.)

There are several points with which I disagree with the author and I’ll go over them one by one.

The claim that Target gives 5% discount on Target transactions to save 2% in interchange is not true. A loyalty program is more than just payments. First of all, loyalty programs existed way before credit cards came around. Brands understood that a loyalty program helped build customer relationship and retain customers. Second, a branded debit or credit card is a tool with which retailers collect valuable first-party information. Who a customer is, how often a customer visits a certain store, what they buy, what combination of goods they buy, what promotions they are most responsive to, whether they want to pick up goods at drive-through, in store or have them delivered. The kind of information not only assists a retailer in personalizing offers and making operational adjustments accordingly, but also powers a high-margin advertising platform. Look at the big retailers on the market. The Walmarts, the Amazons and the Targets of the world all have ambition to build an advertising machine popular with advertisers. How else do they provide targeting to those advertisers without data about their own customers?

There are a bunch of 2% cash back credit cards on the market. Some even offer a higher rewards rate on Target purchases. Consumers are pretty savvy. They will use whatever saves them the most money. Remember that Target would have no information on a customer if they used a non-Target card. Without offering a competitive earn rate, how could Target compete and gain valuable customer information?

The Target credit card is underwritten by TD Bank USA. Co-branded credit cards usually serve as a revenue stream for brands and Target credit card is no exception. According to the latest 10K, Target recorded $734 million in profit sharing from TD Bank as revenue. $734 million! Of course, that’s not entirely pure profit as I believe Target shoulders some of the rewards expenses, but it’s still one hell of a figure. Because Target debit card is issued by Target itself, in collaboration with a bank, they earn much less, if anything at all, from the debit card. So why do they have it in the first place? Why does Target have a reloadable account with the same 5% cash back?

One word: accessibility. Not everyone has a Social Security Number or an ITIN to open a checking account and get a debit card. Then, not everyone with an SSN can get a credit card. TD Bank must have some say in whom they want to give credit to. A FICO of 600 should disqualify a lot of folks from having a credit card. Hence, a lineup of different options helps Target widen their target audience. And if Target already offers a debit card or a reloadable account, they may as well give a reason to customers why they should use those options.

The author of this article argues that retailers should incentivize consumers to use ACH and abandon credit cards. His example is that utility providers already do so. There are two errors with that argument. First, consumers love credit card rewards. Why would they turn away from concrete savings and benefits? Second, using utility providers as an example doesn’t make sense. Consumers pay for utility once a month. Twice or three times at most. These providers charge 4%, which is substantially higher than most credit cards’ earn rate. The extra fee deters consumers from using credit cards as payment method. The gain is smaller than the expense. It doesn’t hurt because most of the time, it’s just one transaction every month. For retailers like Target, it’s different! They want consumers to shop as often as possible. Retailers rarely impose a transaction fee like utility companies do (they negotiate a favorable interchange rate with the networks) and consumers want their rewards. Hence, it’s exceedingly difficult here to change consumer behavior.

In addition, I don’t understand why the Target Debit Card is an example of how Visa and Mastercard can be disrupted. Visa and Mastercard are two of the most known and trusted brands in the world. Walk to a restaurant in a remote country and if you see the Visa logo, you know that your Visa card will work there and you are protected from fraud. How popular is Plaid globally? Is it as trusted as Visa and Mastercard? The networks built an incredible business model in that they are accepted by millions of merchants and millions of consumers trust them. Plaid has been around for a while and if they haven’t gained much traction, what are the odds that Plaid will build a similar business model like the networks?

Plus, how could we replicate that model with ACH? Mom-and-pop merchants want customers and frictionless payments that are proven and tested. Yes, saving 2% is great, but it’s still a lot better than losing business to a competitor nearby because that competitor enables card payments.

I understand that a16z wants to push a narrative that is favorable to their fintech investments, but this is not a good one as the reasons mentioned above.

Leave a comment