Below is my take from reading Instacart’s anticipated prospectus.

What Do They Do? How Do They Make Money?

The best way to describe Instacart is that it is the Uber of grocery delivery. The company was founded in 2012 with a mission to bring online grocery shopping to consumers. Consumers browse for what they want and place an order. After that, a shopper will shop the ordered items from partner retailers/grocers and deliver them to the end destination. Plain and simple.

Like Uber, Instacart is a multi-sided network that connects consumers (orderers), shoppers and retailers with one another. Even though to get this type of business off the ground and scale it is highly challenging, once at scale, the business will have unit economics advantages and an effective barrier to entry against new comers. And at scale is exactly what Instacart is:

- Gross transaction volume (GTV) increased from $5.1 billion in the year ending December 31, 2019 to $28.9 billion in 2022. For reference, even Uber only has about $6 billion in annualized New Vertical bookings, which includes groceries. Also, revenue grew from $215 million to $2.55 billion in the same period.

- 1,400 retail partners including Costco, Aldi, Kroger, Publix, Wegman, Bestbuy and Walgreens. These partners help Instacart reach allegedly thousands of households in the US. However, there is a certain level of concentration risk as three customers accounted for 43% and 38% of Instacart’s GTV and revenue in the first half of 2023 respectively. Any cancellation or disrupted partnership would materially affect Instacart’s business.

- 7.7 monthly active orderers, including the 5.5 million valuable Instacart+ members. More on this later.

- 600,000 shoppers who work 9 hours a week on average, including 4.5 hours actually spent on shopping. Two thirds of these shoppers are female while half are parents.

Let’s talk money. The delivery platform has two primary streams of revenue. The first is transaction revenue. Every time an end user places an order on Instacart, the firm earns a delivery fee and a service fee which varies based on multiple factors (distance, surge pricing, items in question). Instacart then pays shoppers their cut and any tips that end-users generously gave. To be clear, tips are not included in the company’s financial statements.

End users can avoid delivery fees and lower service fees if they subscribe to Instacart+, which costs $10/month or $100/year, and have a minimum order of $35. Subscription fees are recorded under transaction revenue. Unsurprisingly, Instacart+ members are more active and valuable, generating more than 6 times in GTV than non-members and more than half of the company’s GTV in the first 6 months of 2023. Retaining and growing this loyal customer base will be critical to Instacart in the future.

In addition to fees from end-users, Instacart also charges retailers for additional businesses and brand awareness. The prospectus doesn’t reveal how much merchant fees make up of GTV, but I don’t think it’s too high. Grocery is a low-margin business. As a result, Instacart doesn’t want to overcharge and ruin relationships with retailers and grocers.

In the first six months of 2023, transaction revenue averaged 7.2% of GTV, up from 6.3% a year ago. The increase indicates that not only does Instacart grow GTV, but it also becomes better at monetizing the transactions it processes.

The other stream of revenue is advertising. If you have the attention of 7.7 million monthly active users, that’s a great asset to monetize. For Instacart, advertising is a valuable tool that helps the platform reach profitability; a sentiment so coveted by investors these days. In the last twelve months ending June 30, 2023, the company made almost $820 million from ads, approximately 28% of the total revenue. At this rate, I believe it will take Instacart less than 18 months to will reach $1 billion. To put it in perspective, Uber has $650 million in annualized ads run-rate as of Jun 2023 despite being a much bigger platform and available in more markets.

Instacart is one of a few technology companies that go public on the back of multiple quarters of profitability. On an operating income basis, the company has been in the black for the last five quarters, largely due to its advertising business.

Concerns

Declining Engagement From Existing Customers

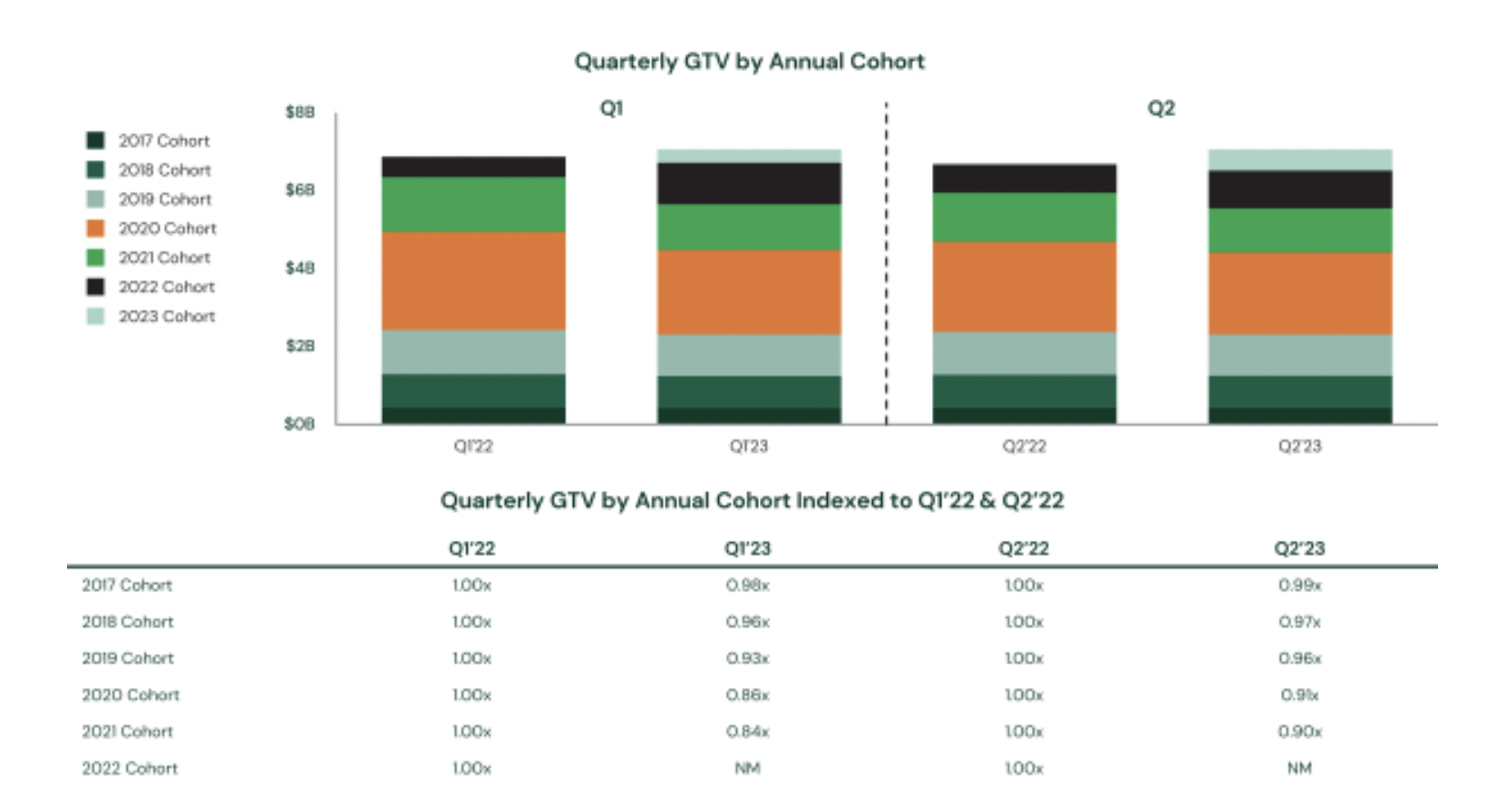

In the first two quarters of 2023, GTV from pre-2023 customers declined by 1-10% compared to the same period one year ago. The only reason why Instacart had a positive YoY GTV comparison is because of the new customers they acquired in 2023. Does this mean that existing customers don’t find the platform useful any more?

One can argue that Instacart may benefit from letting less active customers churn and focusing on more loyal customers. That’s true and it’s true that the company reported higher gross profit as of % GTV for every cohort. The problem; however, is that Instacart included advertising revenue in gross profit calculation, making it impossible to know, without advertising, whether the company gross profit would actually expand.

Growing CAC

Instacart seems to also spend more and more on acquiring new customers. Customer Acquisition Cost (CAC) grew ferociously from $87 in 2019 to $625 in 2022. The first half of 2023 saw CAC grow to $353 from $305 in the same period a year ago, mainly because of the 86% increase in customer incentives and promotions. The growing CAC makes me question the organic appeal of the platform. When and how will Instacart acquire customers more efficiently?

Consumer Behavior

Although I consider myself a netizen, I haven’t bought groceries even once in my life, not even during Covid. Besides the fact that I dislike the additionaly fees, the bigger reason is that I want to physically test the freshness of my groceries. That sentiment is also popular among many other consumers. According to brickmeetsclick, a consulting firm, online grocery sales in the US has had a rocky year so far in 2023. Personally, I don’t think this trend will reverse in the future.

Ads Is A Double-Edged Sword

Some investors will like the fact that Instacart is profitable on the operating income basis, not adjusted EBITDA, partly due to the nice margin that advertising dollars bring. However, there is a risk from having advertising make up 25-30% of Instacart revenue. If the company onboards too many advertisers and litters its search result screen with ads, it will rub end-users the wrong way. Since Instacart already finds it challenging to keep cohorts engaged and/or acquire new customers, an inferior customer experience will push those on the fence to leave the platform. In other words, by overloading ads, the firm prioritizes short-term gains while sacrificing its long-term outlook.

Competition

As mentioned above, in terms of grocery delivery, not even Uber has the scale at which Instacart operates and I don’t think the former will grow fast enough to catch the latter any time soon. Nonetheless, it doesn’t mean the likes of Uber or DoorDash can’t hurt Instacart. A crucial piece of a gig-economy business is drivers or shoppers in Instacart case. These individuals have limited resources in how much time they can spend on driving and delivering. Naturally, they will come to any platform that can help them maximize earnings. That’s the angle which other companies can use to hurt Instacart. If Uber or DoorDash can convince drivers to come and drive for them, Instacart will have fewer shoppers; which will lead to more waiting time for end-users and as a consequence, inferior customer experience and eventually churn.

Competition also comes from Instacart’s own partners. Take Walmart as an example. The Arkansas-based retail behemoth doesn’t want to share precious margin in a tight business like grocery with anyone. Plus, with the launch of Walmart+, the company has more reasons to invest in the flagship subscription and have it drive delivery as well as pickup at stores. In addition, despite partnering with Instacart, Kroger also has its own delivery service. Together, these two retail giants account for 72% of online grocery sales in the US. If these retailers decide to go all-in or prioritize their own delivery services, it will limit Instacart’s future growth. Yes, smaller grocers may need Instacart more, but consumers don’t get the best prices at these smaller players. They want the prices that Walmart offers.

To recap, I am more bearish than bullish over the outlook of Instacart. Yes, the company is operating at scale, it is popular with a lot of consumers and brands, and it achieved profitability. However, the concerns outline above show that Instacart’s competitive advantages are under threat and may not exist in the future, unless the firm does something about it. Until I see something different, it’s difficult for me to be a bullish investor.

Leave a comment