These are the headline numbers from Apple’s Q1 FY2024 earnings

| Q1 FY2024 | Q1 FY2023 | |

| Earnings Per Share | $2.18 | $1.88 |

| Total Revenue (in billions) | $119.6 | $117.2 |

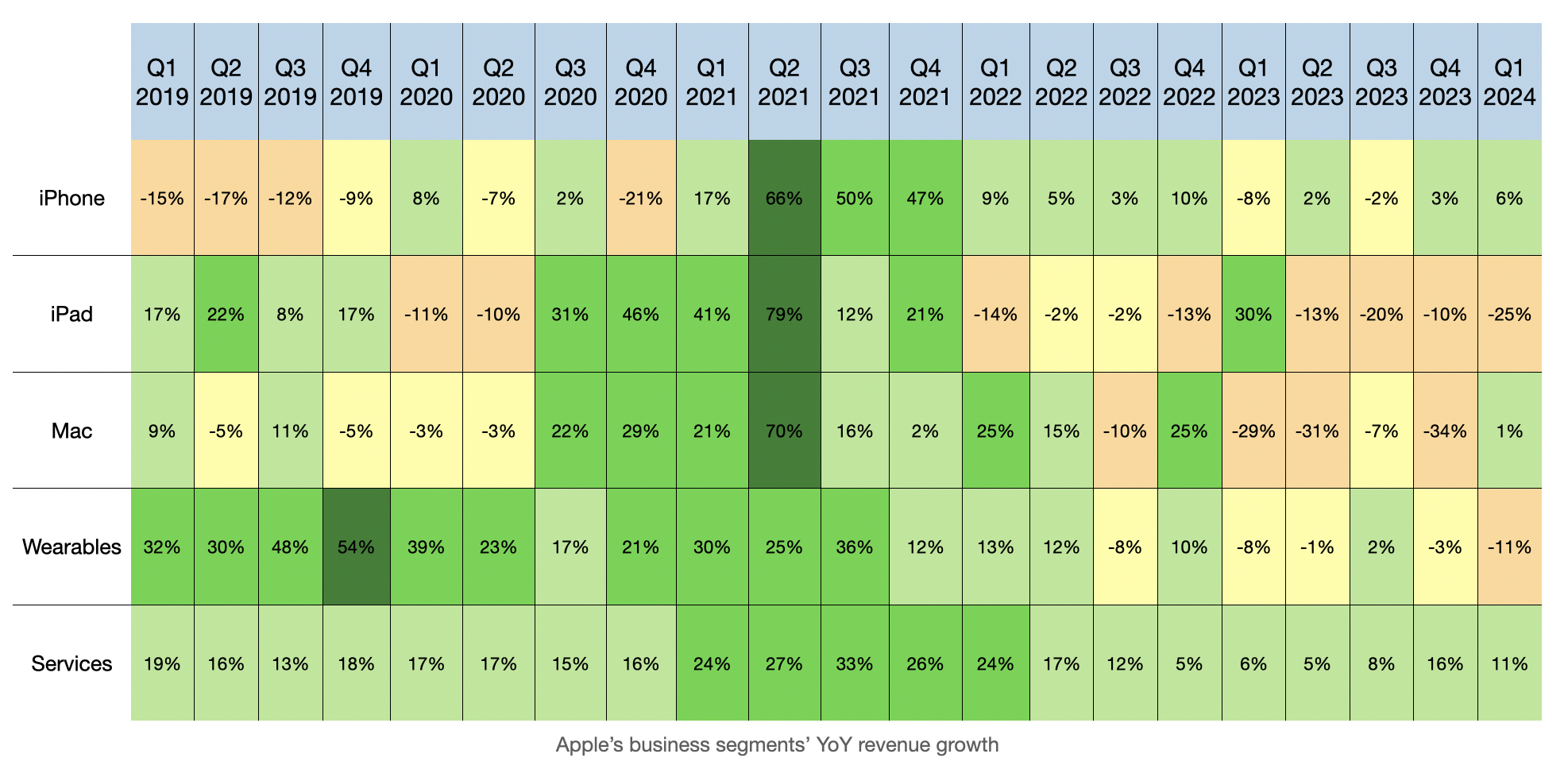

| iPhone Revenue (in billions) | $69.7 | $65.8 |

| iPad Revenue (in billions) | $7 | $9.4 |

| Mac Revenue (in billions) | $7.8 | $7.7 |

| Wearables, Home & Accessories Revenue (in billions) | $12 | $13.5 |

| Services Revenue (in billions) | $23.1 | $20.8 |

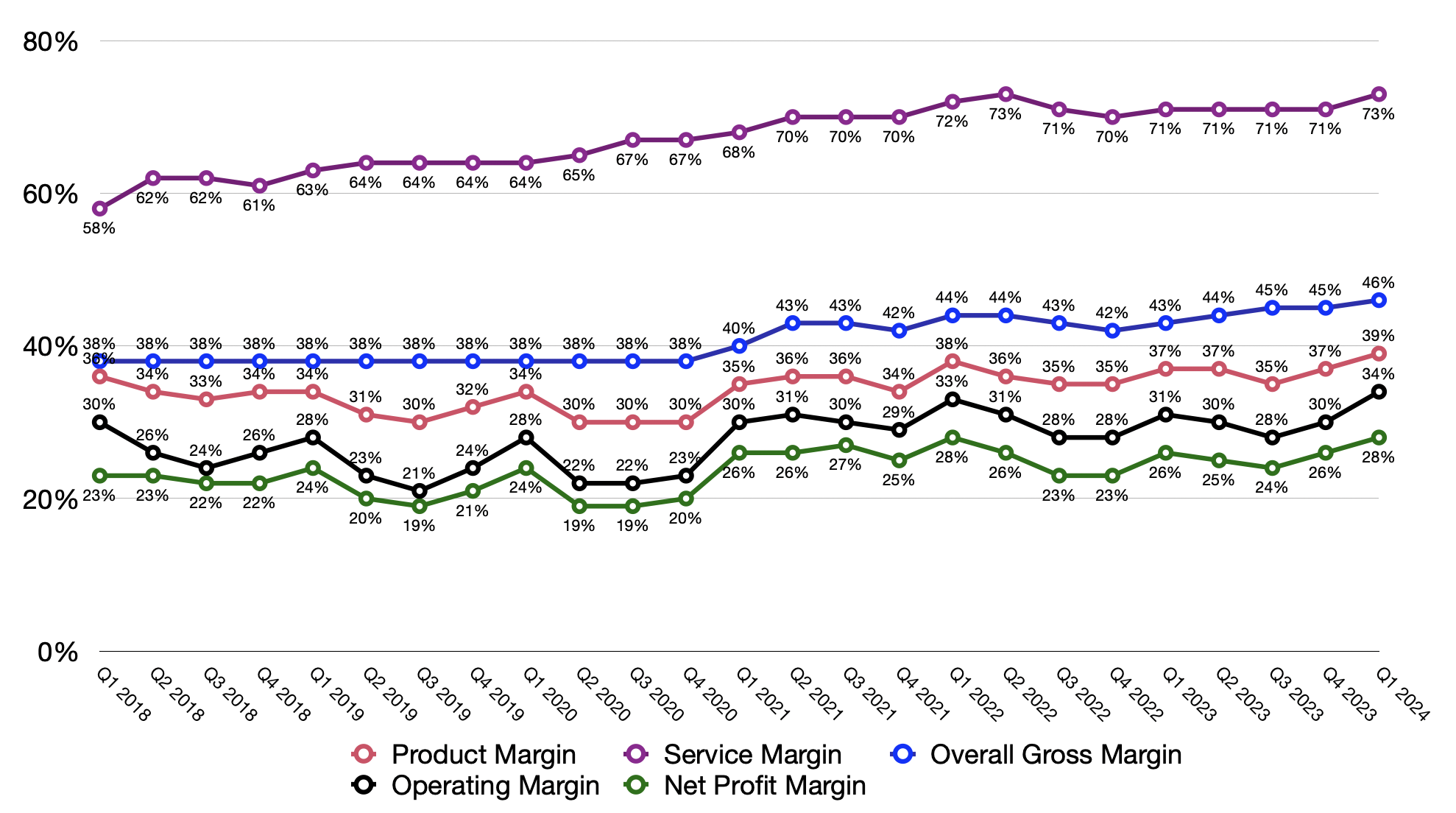

| Gross Margin | 46% | 43% |

| Product Margin | 39% | 37% |

| Service Margin | 73% | 71% |

| Free Cash Flow (in billions) | $37.5 | $30.2 |

After multiple consecutive quarters of revenue decline, Apple was back to the growth territory, albeit by only 2%. Excluding the foreign exchange headwind and the impact of the extra week in Q1 FY2023, YoY growth would be 4%. Earnings Per Share increased significantly, in spite of the modest revenue growth, due to better margin profile and, more importantly, share buybacks.

I find it hard to conduct revenue YoY comparisons for Apple, for several reasons. First, because it is a global operation and has many elements, the impact of foreign exchange is significant. Second, unexpected force majeur also affects how Apple runs the business. Covid, the shutdown in China, the incident at a major factory, global supply chain and the shortage of chips delayed the shipment of products and the recognition of income. In addition, Apple doesn’t have a fixed schedule of product rollout. New products provide a jolt of revenue. Because a product line, with the exception of iPhone, seldom has a new release in the same quarter two years in a row, any YoY comparison must account for this factor and hence can be very tricky. Last but not least, every 6 years, Apple adds a week to the December quarter.

Instead, I prefer to look at something that is less volatile and complex: margin.

Gross Margin hit the record high of 46% and the company guided 46-47% for the next quarter. Both Product and Services contributed to the improvement of margin due to favorable mixes. On the product side, it was the strength in iPhone 15 sale, while on the Services side, the primary contributors were advertising, video and cloud services.

As Apple is unlikely going to have a double digit growth in revenue in the near future, margin improvement is the key lever to grow earnings. With the launch of VisionPro and sustainable strength in higher models of iPhone, I expect Product margin to continue to expand. Regarding Services, it’s a bit more unpredictable. I am not worried about Apple users not paying for services. The challenge is in the regulatory affront awaiting the company. Right now, the biggest change is limited to Europe, which only makes up 7% of the total App Store revenue, but there is no telling what will unfold in the US.

Regardless of what will happen, I am confident that the Apple management team will continue to navigate through tough waters and deliver results. I have been vocally pleased with the competency of Cook and his lieutenants. Together, they took the company to a $3 trillion status, delivered major products in AirPods, Apple Watch, VisionPro, new iPhone models and ground-breaking M chips while overcoming tough unpredictable challenges like the pandemic, supply chain issues, chip shortages, inflation and the Ukraine war. It’s anybody’s guess as to what will unfold in the future. The only thing that investors put their confidence in is the caretakers of a company and their historical performance. In Apple’s case, it’s nothing but excellent.

Leave a reply to Weekly Reading – 10th February 2024 – Minh Quang Duong Cancel reply