Apple released earnings last week and here are the headline numbers:

- Revenue: $85.8 billion, up 5% YoY in spite of 230 basis points in foreign exchange headwind

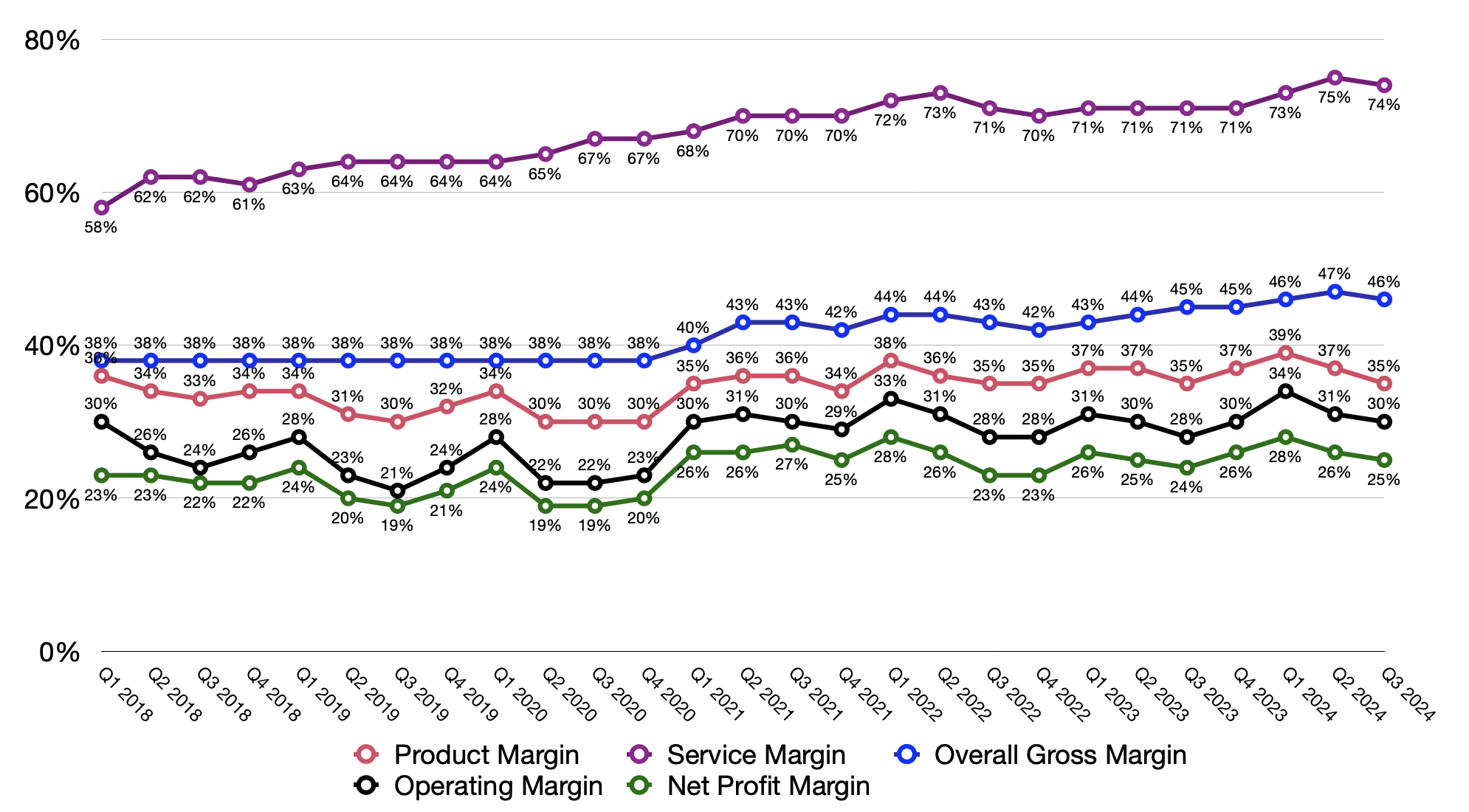

- Gross Margin: 46.3% up 180 basis points YoY

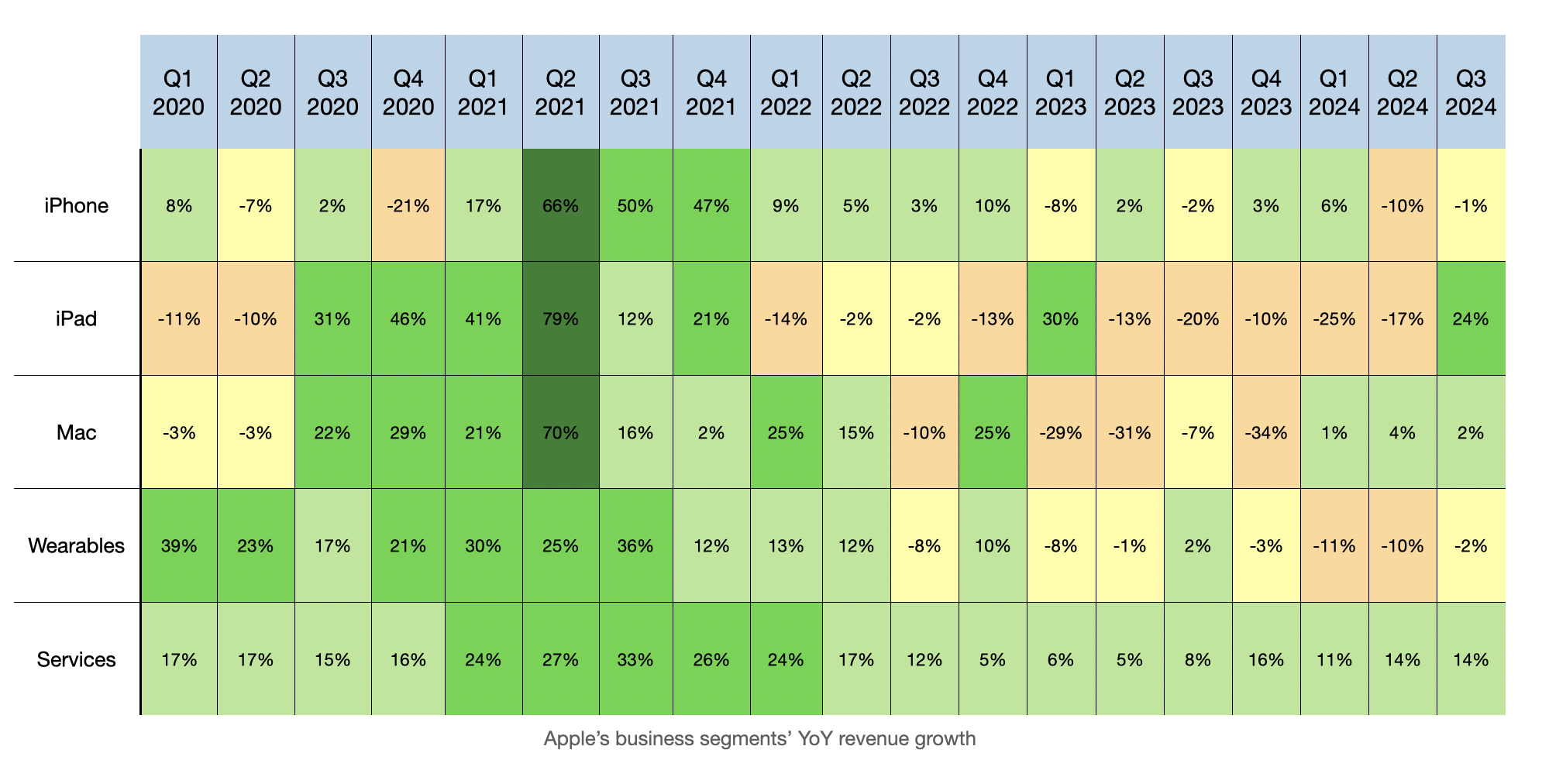

- Service Revenue: $24.2 billion, up 14% YoY

- iPhone Revenue: $39.3 billion, down 1% YoY

- Mac Revenue: $7 billion, up 2% YoY

- iPad Revenue: $7.2 billion, up 24% YoY

- Wearables, Home & Accessories Revenue: $8.1 billion, down 1% YoY

Many investors ridicule Apple because of its low single digit revenue growth and, at times, revenue decline. While I cannot dispute those factual figures, I will caution against using them to doubt Apple’s outlook. The company has staggered product launches which greatly influence the year-over-year comparison. Covid pulled forward revenue as people spent on devices for remote work or entertainment during isolation. Plus, because Apple sells products and services globally, it’s susceptible to turbulence in foreign exchange. Last but not least, there are crises around the globe that no company on Earth can control. Hence, revenue compare should not be the only metric to judge Apple.

Ok, what then? Apple generated more than $385 billion in revenue in the last 12 months. Running and growing an enterprise like that is not easy, and fortunately for Apple, it has a world class management. Gross and Net Margin have been in the mid 40% and 20% for the past years despite all the chaos in the world. There was no mass hiring or widespread layoff like what happened at other big techs. Even now in the AI arms race, Apple smartly relies on its partners sharing the investment cost.

Whenever there is a tariff threat, it’s likely that Apple products are exempted. Tension between China and the US has been rising for a few years, but Apple deftly manages to avoid the wrath of the Chinese government. The ability to maintain relationships with powerful entities can’t be based only on luck.

Furthermore, even though critics lamented that Apple showed no innovation, the company under Tim Cook introduced several new products such as Apple Watch, Airpod Pro and Vision Pro. Also, don’t forget the M chips. The ability to integrate chip, hardware and software enales Apple to control the customer experience and its own fate. But running your own chip department requires vision, commitment, investments and company-wide collaboration. Such success is not accidental.

Ask yourself this: does a capable management matter in your Apple thesis than a fluctating revenue growth that directionally heads up and to the right?

What about growth? Right now, the only constant growth engine of Apple is its installed base and Services revenue. People don’t upgrade products every year, but what they do is to spend plenty of time on their devices. The more Apple devices become essential to consumer daily life, the more likely Apple is going to generate Services revenue.

That is not to say Apple doesn’t have areas that can stimilate growth. Take India as an example. Called “a major focus” by Apple, the country offers an manufacturing hedge against China as well as an appealing market full of middle-class households with increasing disposable income. Bloomberg reported that Apple’s sales in India in the 12 months ending March 2024 hit $8 billion, only a fraction of the $67 billion that Great China brought in the same period. It may not reach China’s level, but India has a lot of potential for the iPhone maker.

Then, there is enterprise. Every quarter, we have a few sentences of update on enterprise like the quote below from the Q3 FY2024 earnings call. I wrote about Apple Business Essentials before. Sadly, we don’t know how big the enterprise segment is to Apple and how big they think it can be. In addition, Vision Pro can unlock special markets for Apple as well, but its potential remains to be seen.

Turning to enterprise. We continue to see businesses leveraging our entire suite of products to drive productivity and creativity for their teams and customers. USAA, a leading insurance and financial services company, recently expanded beyond their existing iPhone and iPad deployments to provide their employees with the latest MacBook Air. And American Express has continued to add to their fleet of over 10,000 Macs to enhance their employees’ productivity, security, and collaboration. We’re also excited to see leading organizations, such as Boston Children’s Hospital and Lufthansa, using Apple Vision Pro to build innovative spatial computing experiences to transform the training of their workforces.

Finally, we have Apple Intelligence. Analysts and investors have conflicting expectations on the impact of Apple Intelligence. Honestly, unless Apple volunteers this data, nobody will know for sure. Personally, I don’t think Apple Intelligence would lift revenue by anything past 5%.

What about risks? Given how important Services is, the increasing regulatory scrutiny is definitely a threat. Any unfavorable rule against the payment from Google or any additional non-sense from the EU can inflict pain on Apple. It’s just the matter of how big the pain will be.

The biggest risk of all is the talent pool. I firmly believe that as long as the current leadership stays, Apple will be in a strong position. Nonetheless, most of them are over 50 years old and very similar in age. Once they leave, it remains to be seen how the future Apple can navigate challenges. Take the industrial design team as an example. It suffered so much loss of talent that it is headed now by Chief Operating Officer, Jeff Williams. Apple appointed a team leader in between who is not a Vice President. Because the company’s success hinges on tight collaboration among various departments, a weak leadership will greatly affect that culture.

For now, I am bullish about Apple. It is my hope that we will see more of the next generation of leadership and that the current team stays on for as long as possible.

Leave a comment