Uber continued to show investors that it is going from strength to strength after delivering a great Q2 FY2024 earnings results and upbeat guidance.

- Monthly Active Platform Users: 156 million, up 14%

- Trips: 2.7 billion, up 21%. This is the 6th consecutive quarter in which Uber delivered a 20%+ growth in trips

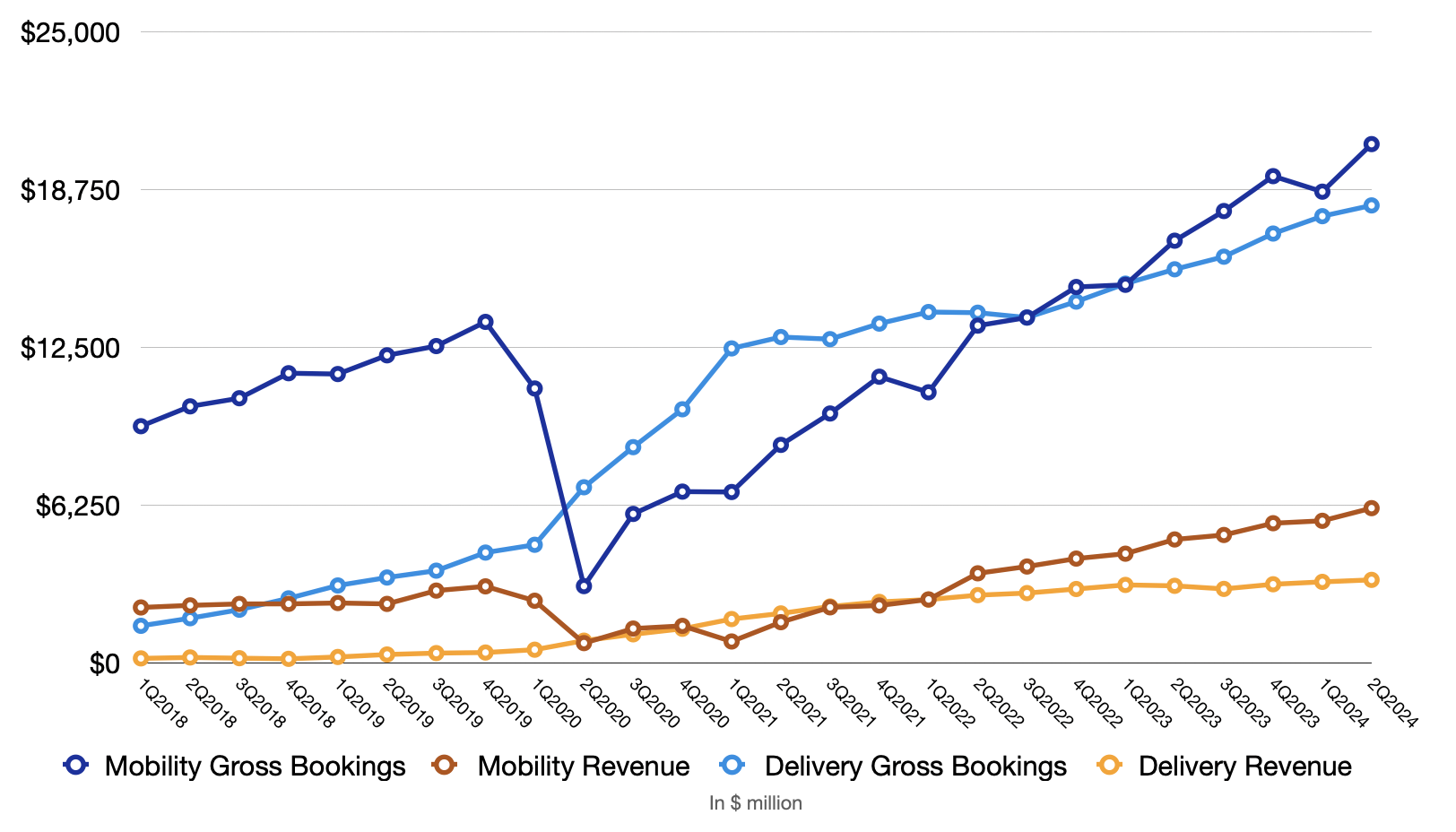

- Gross Bookings: $40 billion, up 19%

- Revenue: $10.7 billion, up 16%

- Operating Income: $796 million, up 144%

- Free Cash Flow: $1.7 billion, up 51%

Uber is a long-term holding in my personal portfolio and has been one of the better performers in the two years. If you are new to my blog, you can read “Uber – Stronger Than Ever” to see why I am bullish about the company and the stock.

For the last 12 months, Uber delivered $150 billion and $40 billion in gross bookings and revenue, respectively. For comparison, DoorDash and Instacart generated approximate $73 billion and $32 billion in gross bookings respectively. In terms of revenue, it was about $10 billion from DoorDash and $3.2 billion from Instacart. That goes to show the size of Uber and how impressive it is that the company is still growing some of the key metrics by 20% or higher.

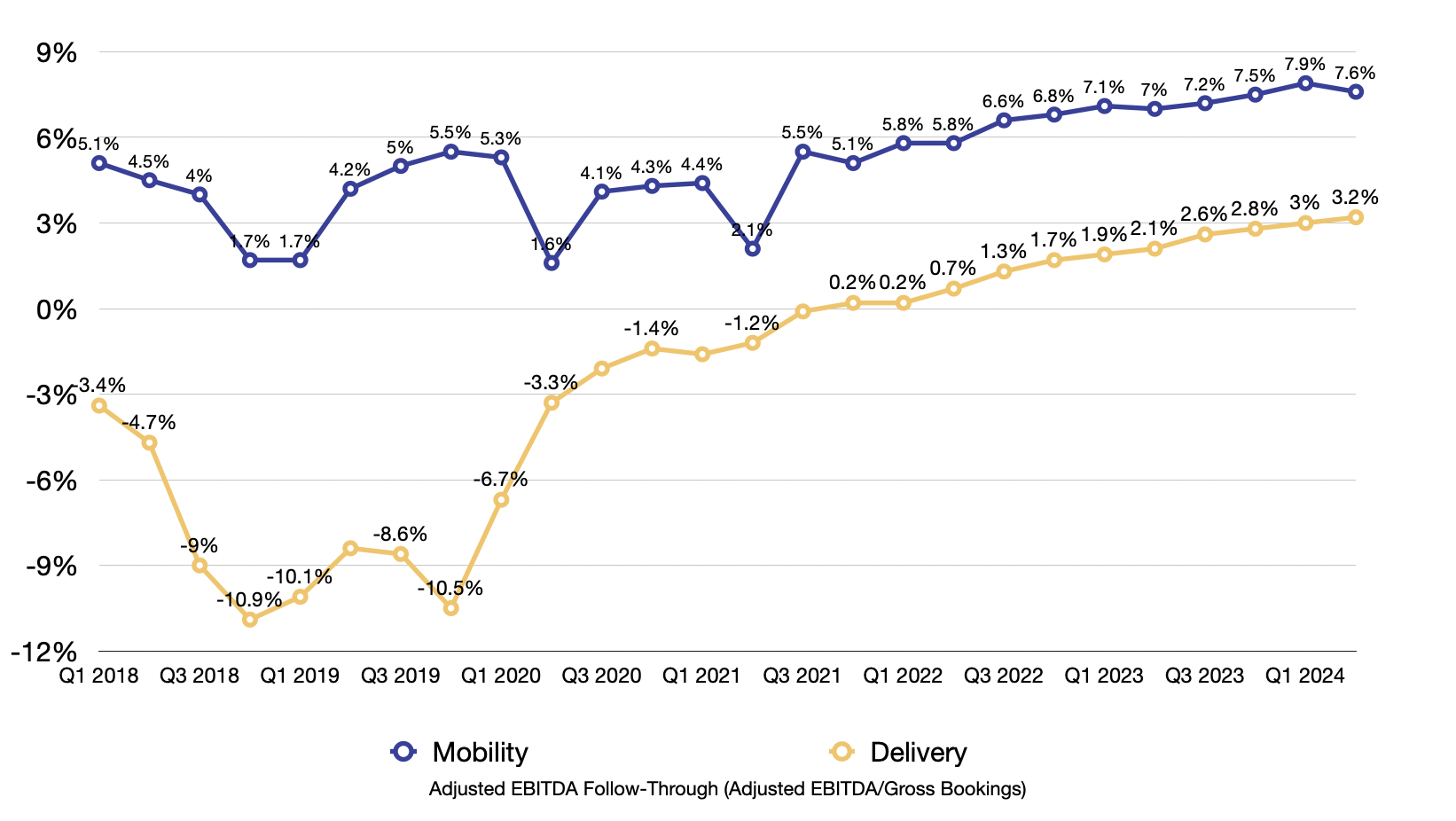

And it’s not only about growth. It’s increasingly profitable growth. Uber Adjusted EBITDA over Gross Bookings has been consistently growing for both Mobility and Delivery. The improved economics stemmed from multiple fronts:

- Uber did not have to spend as much on incentives as it used to. 35% of its users used multiple products. 15% of Uber Eats customers use the platform for grocery delivery as well.

- Uber One drives user engagement and retention. The subscription is now responsible for 50% of Uber Delivery gross bookings, up from 45% in December 2023.

- Having big merchants such as Costco or Domino’s Pizza helps Uber attract users organically

- The advertising business grew to $1 billion in annual run rate

When Uber has more engaged customers who are willing to spend, it’ll be much easier to attract drivers and merchants. The company disclosed that it had 7.4 million drivers and 1.1 million merchants as of Q2 FY2024. These numbers are as good, if not better, than what DoorDash has to offer. The thing with multi-sided platforms is that any competitor wishing to disrupt Uber will have to break the user-driver-merchant flywheel. Such a task is not only exceedingly difficult, but also very expensive. I just don’t see it happening in this environment.

What makes me even more confident in Uber is its willingness to sacrifice short-term wins for the sustainable health of its ecosystem. On the earnings call last week, Uber revealed that merchant funded offers grew 70% year over year. With sponsored listings, merchants pay Uber to reach more customers. With merchant funded ads, businesses don’t run ads, but use attractive discounts to lure customers. From Uber’s perspective, sponsored ads offer higher margin, but the company is happy to encourage merchants to do whatever they need to grow their businesses. Uber understands that even if it squeezes more margin from ads, yet merchants go under, the platform will be a poorer place. Plus, the user experience will be diluted with excessive ads. Overall, I think it’s wise.

The same thinking applies to Uber preferring a richer selection of merchants to using incentives. I imagine that Uber has to make concessions to secure deals with the likes of Costco and Domino’s Pizza. Nonetheless, such a move will benefit the company in the long run as customers are more willing to engage and stick around. Even without incentives.

Uber likely trails DoorDash in food delivery and Instacart in grocery delivery. However, no company has the ecosystem across ride hailing and those two markets like Uber. The business may have a bump on the road from inflation, but over the long term, it should not affect Uber much. Regulatory pressure presents another challenge, but as a market leader, Uber should be able to navigate it better than others. And Dara has proven himself to be a very capable CEO since taking over in 2017. His departure may be the biggest threat to the business, in my opinion.

Leave a comment