Adobe has been a darling of Wall Streets for the past few years and a trailblazer of the SaaS movement. Below is Adobe’s stock performance for the past 5 years.

Today, I decided to take a look at Adobe’s past performance since the strategic switch from selling software as a perpetual license to a subscription-based model in April 2012. Even though I do own a few stocks of Adobe, this post stemmed from my curiosity about how the company has performed and if/how the strategic switch impacted the bottom line. Before we go into details, there are a few notes worth mentioning:

- Adobe’s three main product lines include Digital Media, Digital Experience and Publishing

- Adobe reports financial data by Product lines as just mentioned above and segments (subscription, product and services).

Why Adobe switched to cloud?

In 2011, Creative Suite brought to Adobe more than $4 billion in revenue and a filthy gross margin of 97%. The company sold the software and other products in perpetual licenses. In April 2012, the company announced the transition to the cloud and subscription model. Why?

I’ll let Adobe CFO Mark Garrett and VP of Business Ops & Strategy Dan Cohen at the time answer this question. Per Mark Garrett in an interview with McKinsey:

There were a number of reasons, both financial and strategic. For one, even though customers had higher creative demands, our creative business wasn’t really growing. The number of units we shipped under the old perpetual-licensing model was about three million units a year, and it remained flat for a long time. We were driving revenue growth by raising our average selling price—either through straight price increases or through moving people up the product ladder. That wasn’t a sustainable approach.

The perpetual-licensing model was also limiting us from delivering new innovations and capabilities to our customers. Historically, we had delivered product updates only every 18 or 24 months, but our customers’ content-creation requirements were changing much faster than that, with advances in devices, browsers, mobile apps, and screen sizes.

Inside the company, we had this fundamental belief that there were broader market opportunities for us. Where content was being created and managed, when it was being consumed, and where it was going to be monetized—all of that was changing. We also believed that data were going to become more important. We already had a strong presence in content creation, and we saw an opportunity to broaden our presence in these areas.

The recession was also a factor. During the downturn in 2008 and 2009, our revenue and stock price suffered more than that of most software companies, because other companies had high recurring revenue. Our recurring revenue for the prior fiscal year was about 5 percent annually. We had virtually no financial buffer.

And from Dan Cohen in the same interview:

When we looked at how other software companies were faring during the recession, we saw that companies with high recurring revenue had smaller declines in their growth rates and valuations. We had a very big drop in both—our revenue dropped about 20 percent, and our valuation fell even more. We had extremely high customer-satisfaction rates for our products, but when we drilled down into the numbers, we saw that people were saying things like, “I’m happy with what I have, I don’t see the need to ever buy another one again.” Clearly, we needed to figure out how we could get people to want to buy from us more regularly, and, related to that, how we could innovate better and faster for our customers. We saw that the new software companies that were reaching scale were those operating under a cloud model.

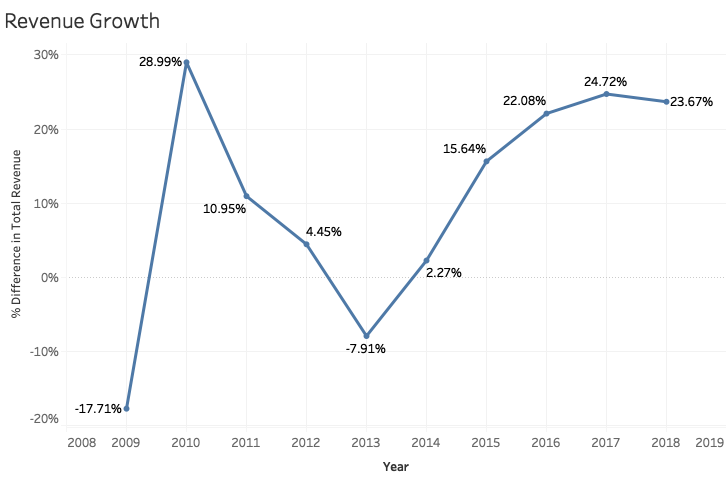

Revenue Growth

Except the two years after the launch (2012 and 2013) and 2018, revenue growth has been climbing. The past three years have seen a revenue growth of more than 20% on average.

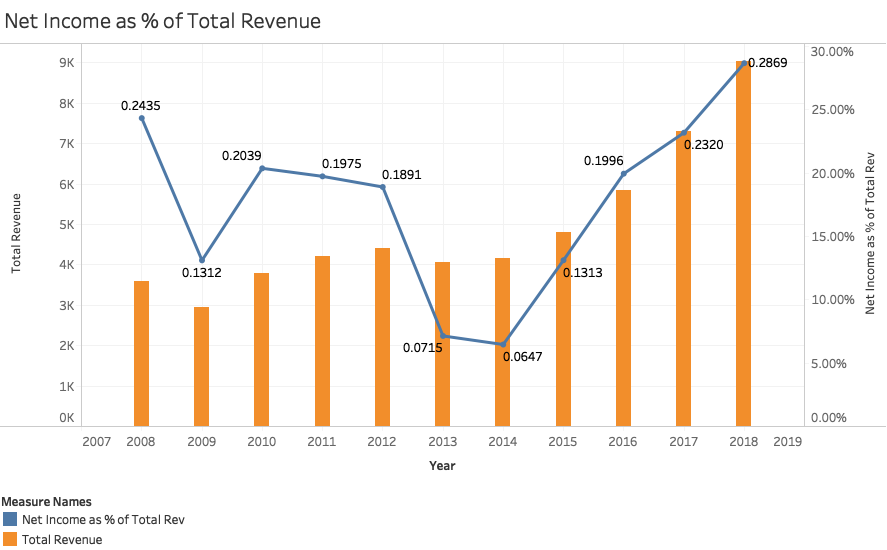

Net Income

Even though the trend looked negative from 2008 to 2013, the past 5 years has seen an amazing streak of increase in net income as % of total revenue.

Subscription revenue as % of total revenue

Before 2012, subscription revenue never accounted for more than 16% of Adobe’s revenue. However, everything changed after the launch and as of now, subscription revenue made up more than 87% of Adobe’s revenue.

Segment Revenue Growth

Since 2012, subscription revenue YoY growth has remarkably outperformed that of Products and Services.

Segment Gross Margin

On the other hand, Product reigned superior in terms of Gross Margin while that of subscriptions has crept up over the years. My guess is that Product refers to the sale of perpetual licenses while subscriptions refer to the regular charge of fees for usage of Adobe’s software. Meanwhile, the margin of Service continues to drop.

Subscription-based revenue by Products

Below is the subscription-based revenue by Products: Digital Media, Digital Experience and Publishing. Missing data is due to the lack of reporting by Adobe

For Digital Media and Digital Experience, revenue from subscriptions makes up the majority of each revenue stream.

Conclusion

Around 2011 when the subscription model wasn’t as popular as it is now, Adobe took a considerable risk by being a vanguard going into an uncharted territory. Nonetheless, it seemed that the company had no choice. Based on the interview with the two C-Suite executives at the time, as mentioned above, the business was entering into a threatening and tricky period. Raising prices was not a sustainable solution. Plus, the company faced a risk of being left behind as the explosion of content outpaced the development & release rate at the time. By turning to the cloud & a different delivery model, Adobe avoided the risk of being obsolete.

Retrospect is a beautiful thing. Looking at the wild popularity of SaaS model nowadays and the data above, it’s clear that Adobe made a correct strategic call to switch the cloud and subscription model.

Leave a comment