My understanding of Amazon’s business model is as follows:

- Successfully become a household online store for shoppers and build a loyal user base (Prime members in particular)

- Leverage the infrastructure (supply chain) for the online store to allow sellers to fulfill orders and sell products through their stores (3rd parties)

- Leverage the IT infrastructure built to maintain online stores to offer Enterprise IT services (AWS)

- Leverage the immense traffic to its online sites and ability to turn traffic into orders to sell advertising services to brands

In my free time, I like to go through annual reports of companies to understand their businesses and performance, in addition to reading the news from sources such as WSJ, Techcrunch, CNBC, to name a few. I did it before for Adobe, Spotify and Apple. Below are my findings from digging through Amazon’s financials from 2013 to 2018. Unavailable figures are due to the lack of reporting from Amazon.

Amazon’s total revenue has been growing increasingly fast in the past 5 years

In terms of net income, except for 2014, it has been growing as well, with 2018 as the standout year

With regard to revenue breakdown, every segment, except online stores, has seen its influence on the total revenue grow for the past 3 years (two for physical stores). AWS, in particular, is making up around 11% of Amazon’s total revenue. Amazon started to report on physical stores’ revenue in 2017. As of 2018, it made up around 7% of the company’s revenue.

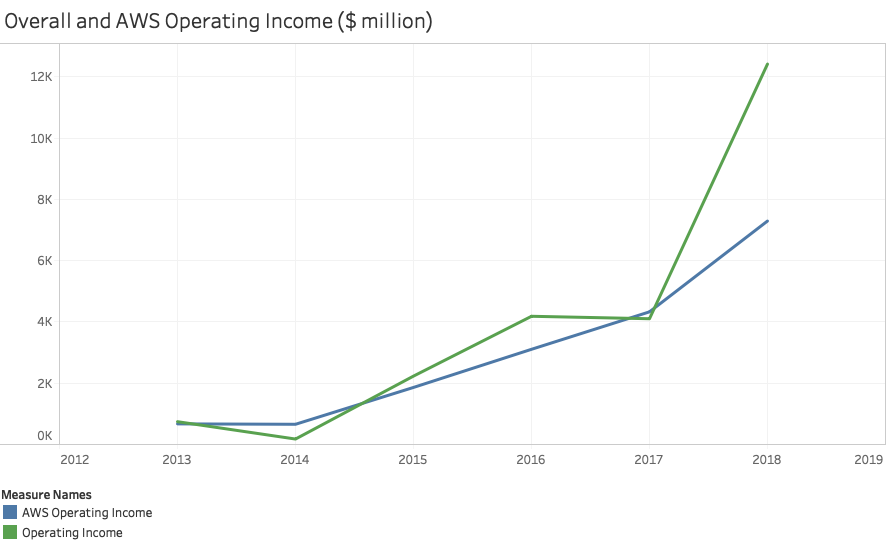

Despite making up only 11% of Amazon’s total revenue, AWS is responsible for the majority of Amazon’s operating income. The reason seems to be that the company lost money from its International segment

Much has been discussed about the growth of advertising and AWS. The two segments have indeed been impressive. Advertising has gone nuts for the past three years while AWS’ growth has never been lower than 42% since 2013

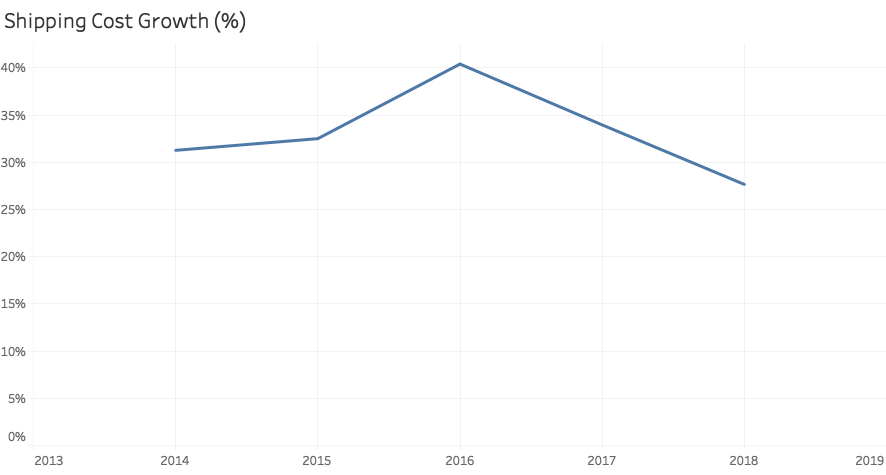

Shipping costs have been growing at a 2-digit clip since 2013, a concern that many analysts and investors expressed. However, the growth rate has slowed down since 2016

Expenses have been growing at a two-digit clip in the past 5 years

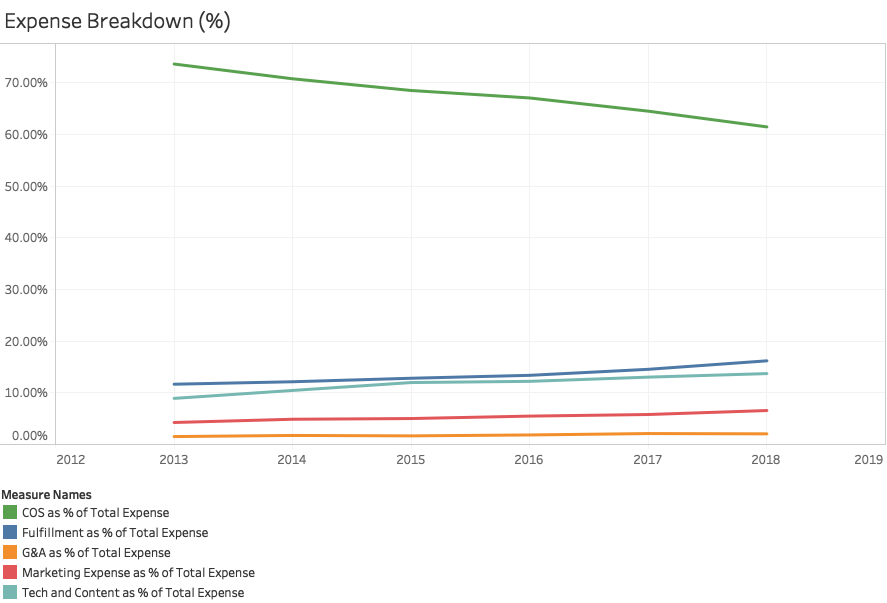

In terms of expense breakdown, Cost Of Sale is still the dominant item, though its contribution to the total expense has been declining steadily. There is one item called Other Expenses in the reports, but I decided to ignore it since it wasn’t significant compared to other items.

Amazon looks to have been successful in diversifying its business, transitioning to more profitable segments from merely relying on the low-margin online stores. With its dominant market share in the cloud and companies moving to the cloud, I believe AWS will continue to grow its importance to Amazon’s first and bottom lines. It also won’t be a surprise to see a middle two-digit growth this year for advertising.

Leave a comment