A different Q4 than others

Apple recorded around $64.7 billion in revenue, a tad higher than they did in the same period last year, and gross margin of 38.2%, 50 basis points higher than Q4 FY2019. Operating income came in at $14.8 billion due to an increase in Operating Expenses. While the increase in revenue is modest, the underlying story between this quarter and Q4 FY 2019 is very different. First of all, we are still in the middle of the pandemic which forces changes in consumer behavior. Students or office workers may spend more on hardware to aid remote working or learning. Consumers may increase consumption of digital content and services more while in isolation for a long time. Secondly, Covid-19 also forced Apple to close some of its stores; which might have adversely impacted sales. Thirdly, Apple didn’t have a new iPhone like it did with iPhone 11 last year; which is a significant element to keep in mind while comparing the two fourth quarters. About 2 weeks of sale for a highly anticipated like a new iPhone is a big deal. Apple executives gave some color on it:

While COVID-19 and social distancing measures impacted store operations in a significant manner, demand for iPhone remained very strong. In fact, through mid-September, customer demand for our current product lineup grew double digits and was well above our expectations – Luca Maestri

If you look at China and look at last quarters — I’ll talk about both last quarter and this quarter a bit. Last quarter, what we saw was our non-iPhone business was up strong double digit for the full quarter. And then if you look at iPhone and you look at it in 2 parts: one, pre-mid-September, which is pre the point at which the previous year we would have launched iPhones, that, that period of time, which was the bulk of the quarter, iPhone was growing from a customer demand point of view. And of course, the — not shipping new iPhones for the last 2 weeks of September makes that number in the aggregate a negative. – Tim Cook

Source: Apple Q4 FY 2020 Earning Call

While I understand the story here; folks didn’t want to buy a new phone in the last two weeks of September until after iPhone 12 came out, I wonder why both Tim and Luca kept emphasizing the growth of iPhone in terms of demand, not sale. Perhaps, I am being too paranoid, but I wonder if that specific call-out implied there is a difference in demand and sale or, in other words, there is a supply constraint.

Because of the reasons given above, it’s not easy to draw a conclusion on the two fourth quarters. It’s unclear how much the factors canceled out one another, but I have a feeling that not having a new iPhone for 2 weeks is the larger force at play here. Hence, I think it’s positive for Apple to exceed the sale last year without an iPhone. But what made up the absence of the new iPhones and a bit more?

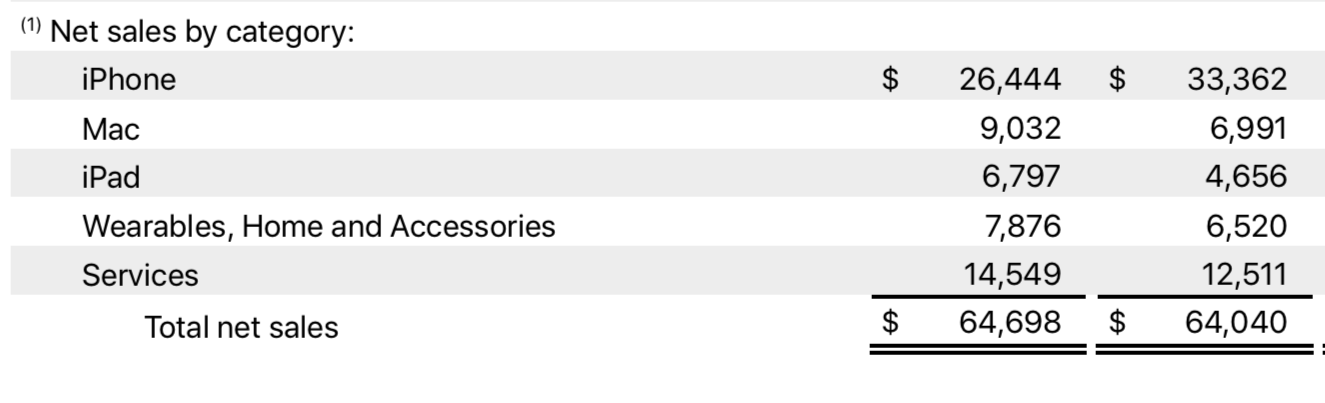

Even though iPhone sale dropped by 21% in Q4 FY2020, non-iPhone sale grew by 30% with an excellent performance from Mac, which reached an all time high revenue of $9 billion and 29% growth, and iPad, which grew by 46% YoY. According to Apple, Mac grew by double digits in every geographic segment and notched all-time revenue records in Americas and Asia Pacific. Meanwhile, iPad had the best September quarter in 8 years in spite of supply restrictions and also saw double digits from every segment like Mac. Additionally, Services had a nice quarter as well with $14.5 billion, up 16% from the same period last year with all time records in App Store, cloud services, Music, advertising, payment services and AppleCare.

In terms of geographic segments, all segments, except China, grew year over year. The absence of a new iPhone, like Tim Cook said, impacted sales in China more than other regions as last year, iPhone made up a higher percentage of sales in China than in other regions. Another reason, according to Tim as well, is a drawdown from the channel side. However, Apple is very bullish on the prospect of iPhone 12 in China because of 5G’s popularity and the fact that Apple is arguably the only major phone manufacturer without a 5G-enabled phone.

On the subscription side, Apple reported 585 million paid subscriptions in total, a sequential increase of 35 million from the previous quarter. For the last 3 years, that has been a sequential increase from one quarter to another. At this rate, it won’t be an issue for the Cupertino-based company to reach its goal of 600 million subscriptions by the end of the calendar year 2020. With the introduction of Apple One on Thursday and the imminent advent of Apple Fitness+, it’ll be interesting to see how they will impact the subscription base. There is no doubt that it will go up, but how fast it will reach the 1 billion mark remains to be seen. My guess is 3-4 years, at the earliest.

How did Apple perform after a year full of challenges?

Apple spent at least half of the last fiscal year in the middle of a once-in-a-lifetime pandemic that brought both headwinds and tailwinds. On one hand, there was more demand for iPad & Mac to enable remote working as well as for possibly Apple TV+, Games and Music. On the other, there were supply constraints and forced store closings. Given all the ramifications of Covid-19 and the absence of a new flagship iPhone, Apple still managed to pull in $274 billion in revenue in FY2020, up 6% from last year. Gross margin increased by 50 basis points to 38.2%, due to a bigger percentage of revenue from Services. Operating margin dropped slightly by 40 basis points to 24.14% because of higher expenses. Next year, my expectation is that gross margin will decrease marginally while operating margin will remain flat because 1/ the new iPhone 12s will be available for order; which will bring a lower gross margin than Services and 2/ the new subscription bundles should also adversely impact gross margin.

Looking at Apple’s segment breakdown, iPhone sale unsurprisingly decreased by 3% YoY while non-Phone sale (Mac, iPad and Wearables) rose by 16%. Individually, Mac grew by 11%, a substantial step-up from 2% YoY growth last year, while iPad grew also by 11% and Wearables by 25%. Apple gave a bit more color on the performance:

- Mac sale increased due to primarily higher sale of Mac Book Pro

- iPad sale grew due to “higher net sales of 10-inch versions of iPad, iPad Air and iPad Pro”

- Wearables sale grew “due primarily to higher net sales of AirPods and Apple Watch”. Because this segment also includes Apple TV, Homepod, iPod touch, Beats products and Accessories (like keyboard, Magic Mouse or cables), this disclosure means that last year wasn’t particularly a good year for Apple TV and Homepod. It’ll be interesting to see how the new Homepod Mini will perform in the future.

The changes in Services really caught my attention. Services brought in almost $54 billion in FY2020, up 16% YoY, “due primarily to higher net sales from the App Store, advertising and cloud services”. The color given by Apple this year differed a bit from last year’s when the increase in Services sale came mainly from App Store, Licensing and Apple Care. The difference, I suspect, came more from the impact of Covid-19 which forced some store closings and hurt AppleCare, than from an increase in demand for iCloud. When comparing the language Apple used to describe their Services segment, two points stood out for me

| 2020 | 2019 | 2018 | |

| Services’ main components | – Advertising – AppleCare – Cloud Services (iCloud) – Digital Content – Payment Services (Apple Pay, Apple Card) | – Advertising – Apple Care – iCloud – Digital Content – Other services (Apple Arcade, Apple News+, Apple Pay, Apple Card) | – Digital Content and Services (which doesn’t include any language on licensing) – iCloud – Apple Care – Apple Pay |

- Advertising, which may include the deal with Google, was called out more prominently in 2019 and 2020. Perhaps, it’s because the payment from Google is substantial enough for it to have its own section

- The new Payment Services now has its own section which I suspect will be the case moving forward. Tim Cook already said it’s an area of great interest to Apple, though they haven’t made public any more updates on either Apple Pay or Apple Card for a while

From the geographic segment perspective, 2020 was a good year for Americas, Asia Pacific and Europe as those segment booked all-time records while Japan stayed largely flat for the past three years and China had the lowest revenue since at least 2015. In fact, China’s revenue as % of total revenue came down from 20% in 2018 to less than 15% in 2020 while Europe was responsible for one fourth of Apple’s total revenue, up from 23% in 2018. With the new 5G-enabled iPhone 12 that suits Chinese consumers well, this segment’s revenue may likely increase considerably in the upcoming fiscal year.

In terms of operating margin, Japan led the way consistently at 43% while Americas, the biggest market for Apple, lagged behind other segments. China’s operating segment has been steadily improving and has now the second highest operating margin, behind only Japan. Because Apple didn’t give any explanation on the difference in operating margin across segments, I suspect that the reason why Americas’ is low is because of introductory offers from services such as Apple TV+, Apple Card, including sign-up bonuses, investment in content and installment plans for purchases with Apple Card, which is available to only consumers in America.

From a market distribution standpoint, Apple has been steadily increasing its direct share, growing it from 28% in 2017 to 34% of total revenue in 2020. I would imagine that a direct sale through its stores and website carry a higher gross margin than through a 3rd-party supplier. However, given that Apple didn’t particularly offer enough information and that Apple has 0% interest payment plan in America for customers with Apple Card through its stores and website, it’s challenging to gauge the specific impact of this transition. Nonetheless, because America’s operating margin and the company’s stayed largely flat, the more emphasis on direct channels may mean more in terms of customer relationships than in margin.

All in all, here are my take-aways from looking at Apple’s latest 10Q and 10K

- Non-iPhone businesses have a bright outlook. Mac and iPad booked a strong 4th quarter, are well-liked and with a high probability, will continue to enjoy the tailwind of remote working trend. Wearables will continue to grow. I love my Apple Watch and Airpods Pro and anyone I know who bought these products says the same thing. The fact that Wearables is now the size of a Fortune 130 company after only 5 years on the market is incredible. The thing with Apple is that they tend to have a knack for offering incremental improvements that work well for consumers while keeping the prices largely on the same level. Because of that, I have confidence that Wearables will continue to grow in the near future.

- iPhone is no longer responsible for half of Apple’s revenue like it used to in the past. Regardless, it’s still a popular phone. Just look at how people follow closely every announcement, from hardware to software, and how folks share their homescreen designs with iOS14, something that Android has had for a long time. Because I live in the US where 5G infrastructure isn’t really well built, it’s hard to see how iPhone 12 will sell. Personally, I wouldn’t buy iPhone 12. There is not enough motivation to upgrade from 11 to 12. Even Apple executives were pretty guarded when it came to giving colors on the new phones. On the other hand, iPhone 12 may become a hit in China, especially with the 5G infrastructure they have over there.

- Services is now bigger than Mac and iPad combined and grew at a clip of 16% in the last two years. The key drivers of that growth look set to remain strong in the near future: 1/ Apple Care, which rides along with Apple’s popular products, 2/ App Store & iCloud and 3/ Advertising which seems to be made up largely of the deal with Google. Even though that deal is under scrutiny, it’s unclear whether Apple will lose that lucrative advertising money. Even if it does, there will be other browsers ready to jump in, albeit at a lower value. The breadth of Apple’s services keeps growing with Apple One and Apple Fitness+, and presence in more geographical markets. Hence, I expect Services to keep growing at 15-16% a year in the next two years.

Disclaimer: I own Apple stocks in my personal portfolio.

Leave a comment