Amazon continues to amaze me with another blow-out quarter in Q3 FY2020. Their total net sales increased by 37% compared to the same period a year ago, reaching $96 billion, while Operating Income increased by 96% from $3.2 billion in Q3 FY2019 to $6.2 billion this quarter. It’s an extraordinary growth for a company that generated more than $1 billion a day in net sales this quarter. Their gross margin in general didn’t change much from a year ago, but their operating margin increased by almost 200 basis points from 4.5% in Q3 2019 to 6.4% in Q3 FY2020. While the high level margin doesn’t look impressive, the devils are in the details if we look closer at their segments.

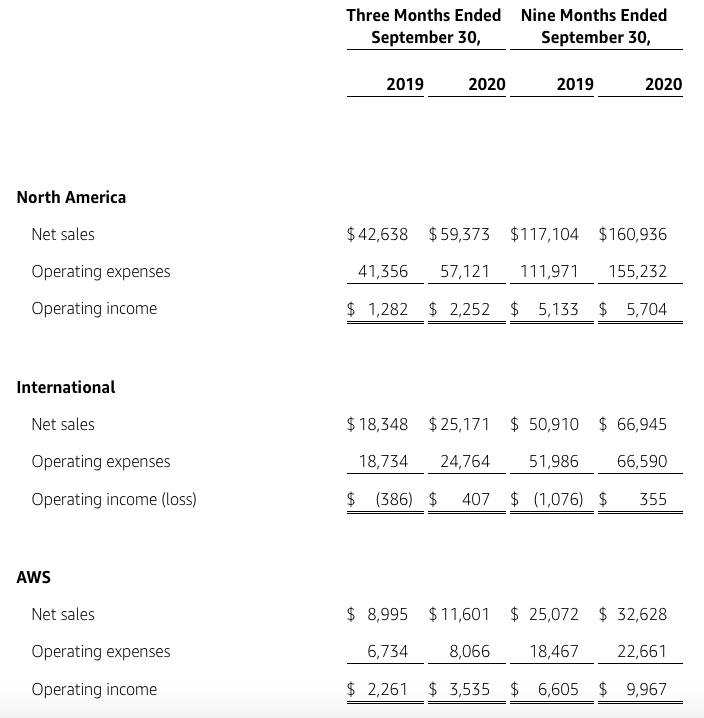

If we look at Norther America, International and AWS, all three were profitable this quarter with International, traditionally a money loser, being in the black for the second quarter in a row. AWS continues to be responsible for most of Amazon’s operating income as it carries a sweet 30% operating margin, compared to a meagre low single-digit from the other segments. Interestingly, AWS’s growth was the slowest among the three segments, recorded at 29%, compared to 39% of North America and 37% of International.

If we look at the results at a deeper level, specifically at the breakdowns into Online Stores, Physical Stores, AWS, 3rd party marketplace, Advertising and Subscriptions, the only area with negative growth in revenue is Physical Stores. 3rd party marketplace, Advertising and Online Stores notched the biggest growth, in that order, followed by Subscriptions and AWS. Regarding Subscriptions, Amazon reported that Prime now has 150 million subscribers with the service coming to its 20th country in Turkey.

Internationally, the number of Prime members who stream Prime Video grew by more than 80% year-over-year in the third quarter, and international customers more than doubled the hours of content they watched on Prime Video compared to last year.

Source: Amazon Q3 FY 2020

Even though Amazon is the master of operating at scale, innovating and squeezing efficiency from every step, I do think the expansion of Prime internationally helps with the increased performance of the International segment which has been profitable in two consecutive quarters. Of course, the decision makers at Amazon have data to see which markets can be improved by launching a high-margin subscription that makes customers stick around longer and shop more. So I wouldn’t surprised if Prime played a role in bolstering the profitability of Amazon’s International segment. So far, there are only 20 countries where Amazon Prime is available. When that number gets bigger, I predict that Amazon will be even bigger and more profitable than it already is; which is both admirable and scary.

When it comes to Amazon, advertising is unlikely the top 3 or 5 services that come to mind. Nonetheless, the segment brought in almost $5.4 billion this quarter, at the growth rate of a whopping 51%. To put that in consideration, neither Pinterest, Twitter nor Snapchat recorded even $1 billion in revenue in the most recent quarter (all of these companies reported results this month). Even Microsoft’s search advertising revenue this quarter was at only $1.8 billion, down from about $2 billion from the year before. As Amazon has an excellent relationship with customers (in general) and customers, when searching, already have intention to buy, this advertising business will not stop here. In fact, I do think it will continue to grow nicely in the future. A short while ago, I wrote about Amazon Shopper Panel, a new initiative by Amazon. The service will compensate shoppers if they send the company 10 eligible non-Amazon at-store receipts every month. This initiative, if done well, will empower Amazon with an unparalleled understanding of consumers, down to even the line items of a receipt. This understanding will bolster their advertising machine even more.

Amazon admitted that 2020 has been a big year for capital investments. The company aims to grow its fulfillment and logistics network by 50%, plowing around $12-13 billion in CAPEX this quarter or over $30 billion so far in 2020. That is an extraordinary amount of money allocated in growing assets. Not many companies even have that kind of numbers in revenue, let alone CAPEX. On top of that, Amazon reported that its shipping costs reached $15 billion this quarter. Fulfillment and shipping are hard as they are resource-intensive and require a mastery in operations to achieve the necessary efficiency. Any competitor that wishes to challenge Amazon needs to have a pocket deep enough to absorb these expenses; which constitutes a competitive advantage for the biggest e-Commerce player in the US. In the end, how many companies in the world could claim they generated $55 billion in trailing 12-month (TTM) Operating Cash Flow or $29 billion in trailing 12-month free cash flow?

In short, the business looks to be in a fantastic shape with amazing growth at a massive scale. Plus, there is plenty of room to grow for Amazon in the future with International expansion, Prime in more markets and advertising. Jeff Bezos is now a $200 billion man. I won’t be surprised if he reaches $300 billion in net worth in the future.

Leave a comment