Target’s growth during the pandemic

Writing that 2020 is good for somebody or a company is weird as this year has been nothing, but a disaster. However, from a business perspective, Target has had a pretty good 2020 so far.

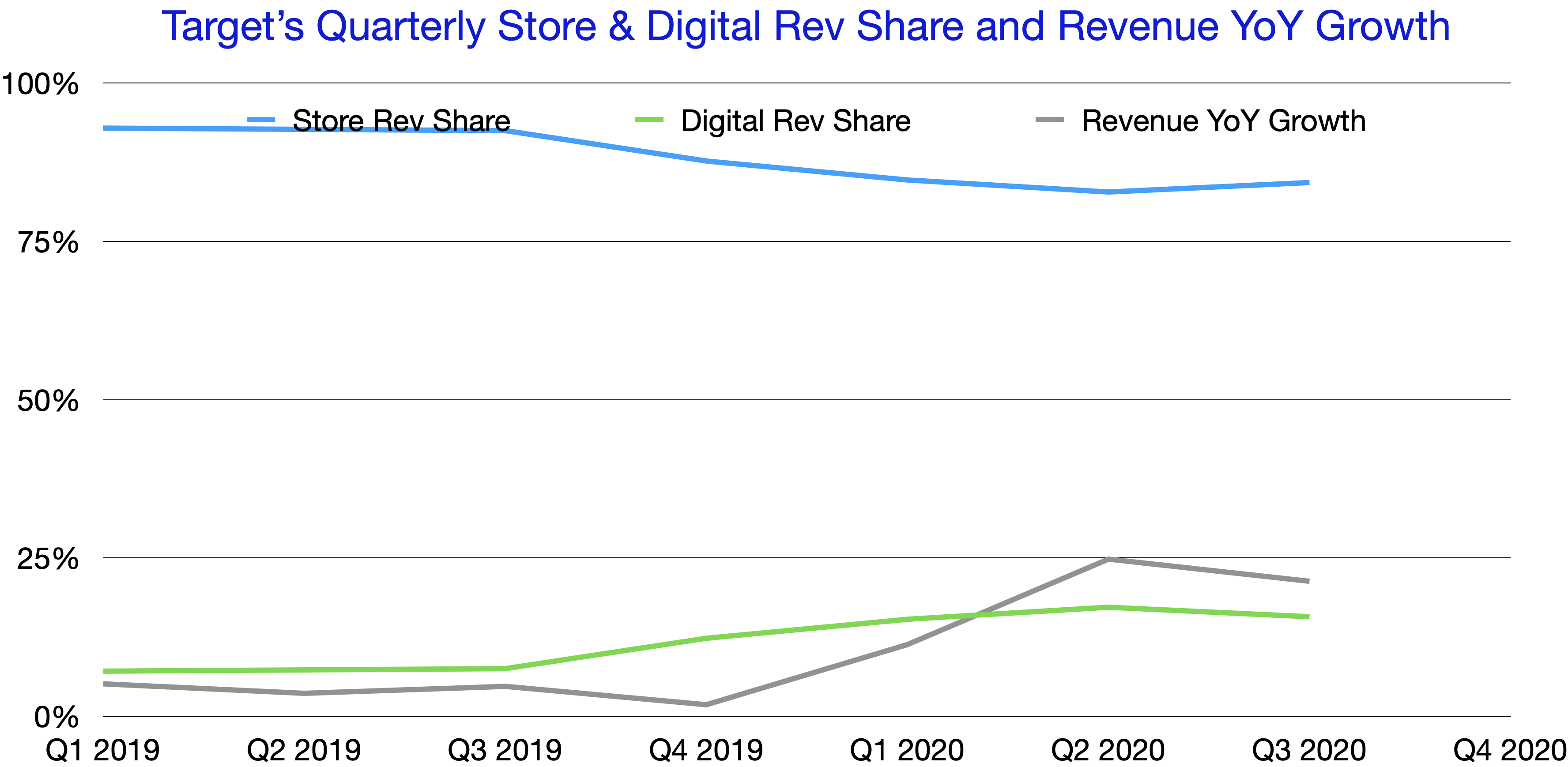

Before 2020, its comparable sales growth was often a low or middle single digit. In Q4 2019, its physical store comparable sale growth was even in the negative territory. 2020 flipped the switch. The company’s total comparable sale growth has been in the double digits with Q2 2020 recording the highest at 24%. Digital comparable sales growth is at least 9% or higher. Q3 saw a bit of a decline compared to Q2, but the overall growth was still higher than 20%. I find it interesting that the revenue YoY growth and the store comparable growth seem pretty in sync with each other, but that’s because physical stores make up at least 84% of Target’s revenue. Digital sales was responsible for almost 16% of the overall revenue in Q3 2020, an equivalent of $3.6+ billion in revenue for a quarter and up from 7.5% in the same quarter last year.

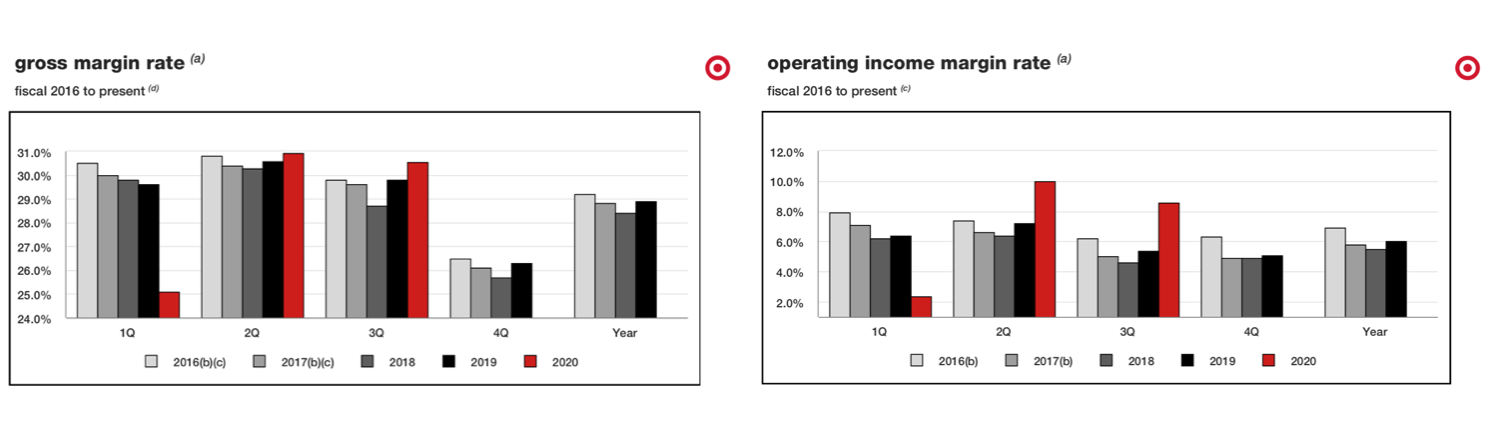

In terms of profitability, Q2 and Q3 of 2020 saw the highest gross margin and operating margin in the last 5 years. Operating margin reached 10% and 8.5% in Q2 and Q3 respectively while gross margin was 30.9% and 30.6% in Q2 and Q3. During a year dominated by a once-in-a-lifetime pandemic, Target managed to pivot its business to adapt to the dire situation and improved not only its top line, but also its profitability. That’s proof of resilience and managerial competence.

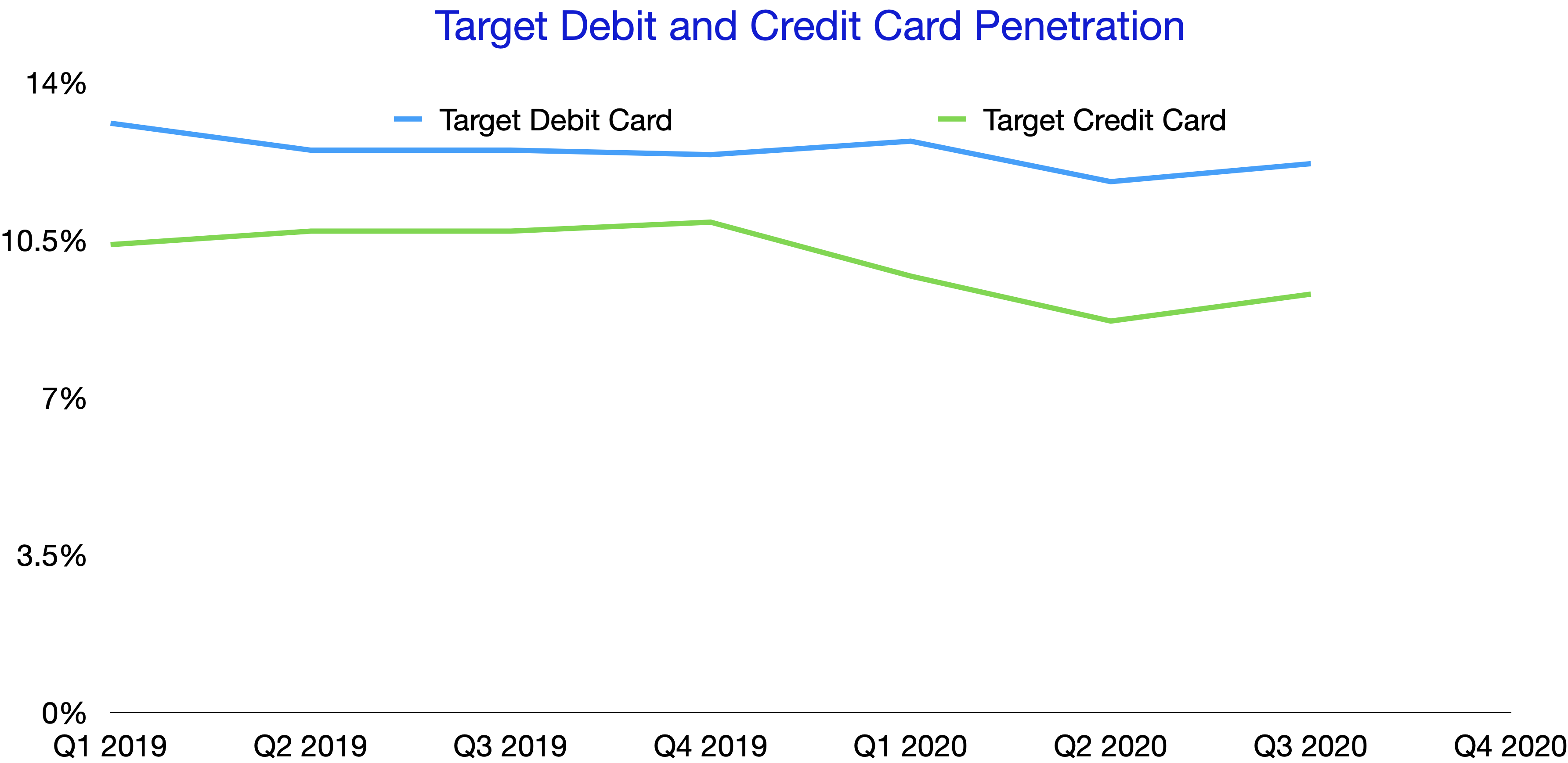

Another aspect of their business that I find interesting is their branded cards’ penetration. Target measured its credit and debit card’s penetration as percentage of sales that took place on their cards. In other words, if there is about $200 million in sales in a week and $50 million of which is paid through Target’s credit and debit cards, the penetration rate is 25%. And shoppers have a reason to use those cards. Owners of these cards have exclusive benefits that other issuers can hardly match, such as: no annual fee, 5% off on purchases at Target stores and on its website, free 2-day shipping on select items and longer return period. Yet, there has been a slowly steady decline in terms of the RedCard penetration. The penetration rate in Q3 2020 was 21%, down from 23% from the year before. Given the increase in sales and the unique offerings of the RedCards, it’s surprising that the figure not only didn’t grow, but it also contracted. This indicates to me that Target can do much better in getting customers to apply for a RedCard. It is a good retention tool and it brings extra revenue to the company. In Q3 2020, credit card profit sharing was $166 million, but down from $177 in the same period last year.

In short, Target has been doing quite well. They succeeded in growing their online business which has been turbocharged by the pandemic, but that, in no way, means that the company didn’t put in the effort. Think about it this way, every retailer tried to grow its online business, but Target managed to do in a cut-throat industry and at their scale. So credit to them. Plus, they made appropriate and necessary investments in same-day services and deliver. In the last two earning calls, the management reported ridiculous numbers of same-day services’ growth, to the tune of several hundred percentages. Shoppers like options. With Target, they can now order online and have it delivered to their door, or drive up to the parking lot to pick the order up or fetch it in stores. The flexibility is there and it will bode well for Target in the upcoming holiday season that is unfortunately engulfed, still, by the pandemic.

Regarding the possibility of Target having a similar subscription to Walmart+ or Amazon Prime, I think Target is still missing the main hook, the main attraction. Amazon Prime has been around for more than 10 years. Over the years, Amazon kept adding more and more benefits for shoppers so that the subscription now offers a plethora of benefits ranging from unlimited 2-day shipping regardless of order size, movies, music, books, exclusive deals and so on. On Walmart Plus side, Walmart can offer affordable groceries and discount on fuel. Target doesn’t seem to me that it can match any of those benefits. Even though some pieces are there such as Target’s popularity, its network of stores across the country and its delivery flexibility, I don’t see a main selling point for a Target’s own subscription yet. We’ll see.

Salesforce reportedly in talks to buy Slack

Yesterday, after the news broke that Salesforce has been in talks to acquire Slack and a deal can happen next week, Slack’s stock price popped by more than 30% within a day. The reaction that I saw on Twitter was mostly positive for both parties. I can see why. But the fact that investors are happy about this prospect of an acquisition says something about Slack as a standalone business. Slack last reported its active daily user at 12 million back in October 2019. Within the past 12 months, Microsoft revealed the metric at least 3 times: 20 million in Q2 FY 2020, 75 million in Q3 FY 2020 and 115 million last month for Q1 FY 2021. There are two reasons why companies don’t make disclosures: 1/ they are legally obligated not to and 2/ there is nothing rosy to disclose. In this case, it’s squarely the latter case. My guess is that Slack hasn’t seen a meaningful increase in its Daily Active Users (DAU) numbers DESPITE a pandemic that turbocharged working from home, the same way that Microsoft Teams has achieved. In the face of a formidable challenge from Microsoft, Slack initially played it cool. Below was their reaction 6 months ago

“What we’ve seen over the past couple of months is that Teams is not a competitor to Slack,” Butterfield told CNBC in an interview after Microsoft’s Q3 earnings update. Butterfield also downplayed the impact on Slack’s growth caused by Microsoft “bundling [Teams] and giving it away for free” with Office 365 over the past three years.

Source: ZDNET

Yet, Slack filed a formal complaint to the EU about Microsoft’s alleged anti-competition practice, the same practice that Butterfield downplayed. I wrote here about why that formal complaint is unlikely to succeed. But it shows Slack’s desperation. If Microsoft weren’t a competitor and its bundling practice was nothing, why would Slack sue to stop it? All of these factors and the fact that investors were happy about the prospect of being acquired by Salesforce paint a solemn picture of Slack as a standalone company. If it joins Salesforce, there will likely be a Salesforce bundle that includes Slack, the same way that Microsoft bundles Teams into Office 365. Slack would get more assistance in selling to corporate clients while Salesforce would get extra capabilities quickly without having to build them from scratch.

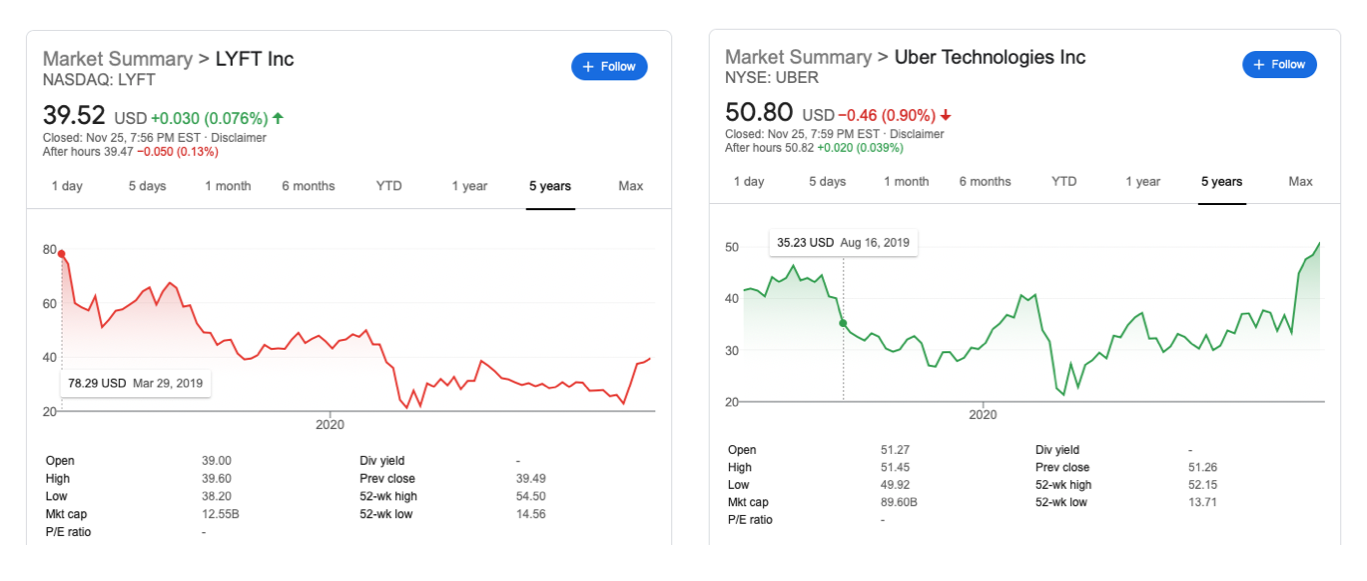

Uber vs Lyft

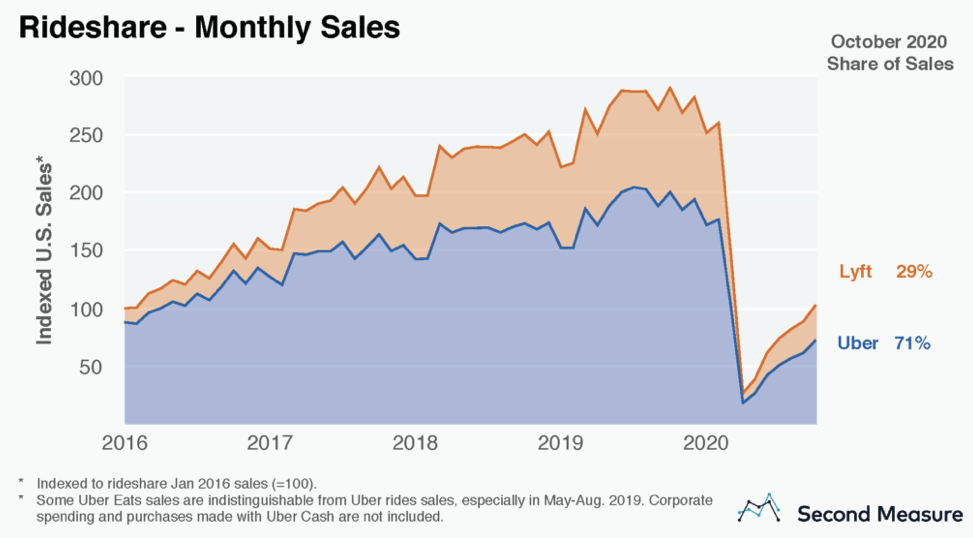

The pandemic has been a catastrophe for ride-hailing companies such as Lyft and Uber. According to Second Measure, the market in the US dropped to only half of the 2016 level and only recovered to the 2016 level in October 2020. That’s how big the impact of the pandemic has been on this business. Since Uber and Lyft are always compared to each other, you’d think that their business is faring similarly. Not really.

While Lyft essentially has only one business in ride-sharing, Uber successfully grew its food delivery service UberEats to be a $4.5 run rate business, making up 40% of Uber’s revenue in Q3 2020. Uber Eats’ $1.1 billion in revenue in Q3 2020 was more than double Lyft’s entire revenue in the same period. Additionally, the pandemic affects each other differently. Lyft’s main market is the US, which is, unfortunately, going deeper and deeper into the pandemic. There is no sign of things turned around here in the US, unless there is a vaccine. It severely handicaps Lyft’s business and Uber’s ride-sharing segment. Nonetheless, Covid-19 has been a boon to Uber Eats. It has grown substantially in the past few months and become a silver lining for Uber. Plus, Uber announced its effort to deliver groceries and its acquisition of Postmates indicates that it is serious about becoming a delivery-as-a-service business. In other words, while the two companies are often mentioned in comparison, they are vastly different now, with Uber becoming more of a diversified company. It is more diversified horizontally (more services) and vertically (if you consider being present in more countries). In this environment, I think that the Uber model is a much better one. Don’t take my word for it. Look at the stock prices. The two companies made debut on the stock market almost at the same time. While Uber soared past its IPO price, Lyft is trading nowhere close to its own IPO price.

It’ll be interesting to see how the next couple of years will be for these two companies. Would Lyft venture into another business like Uber did? What would a vaccine bringing back our previous life mean for Uber? Knowing that it would power up the ride-sharing business, but adversely affect the growth of Uber Eats?

Leave a comment