Costs and benefits of a credit card from an issuer perspective

Issuing a credit card is a business and hence, it comes with risks, expenses, revenue and hopefully profits. A credit card issuer’s revenue comes from three main sources: interchange, fees and finance charge. Finance charge is essentially interest income or the interest on outstanding balance that users have unpaid at the end of a cycle. Fees include late fees, cash advance fees or annual fees, just to name a few. Interchange is what an issuer receives from merchants on a transaction basis, according to a rate agreed in advance and usually dictated by networks such as Visa or Mastercard. There are a lot of factors that go into determining what an interchange rate should be, but for a consumer card, it should not be higher than 3% of a transaction’s value.

As an issuer thinks about which credit card product to issue, it needs to balance between the benefits of the card, the expenses and the profitability. For instance, nobody would be paying $100 in annual fee for a credit card that has a standard 1.5% cash back without any other special benefits. That product wouldn’t sell. Likewise, an issuer would flush money down the toilet if it issued a card with a lot of benefits such as a Chase Sapphire without a mechanism to make money on the other side, like an annual fee. The art of issuing a credit card is to make sure that there is something to hook the users with and a way to make money.

The dynamic between a brand and an issuer in a Cobranded credit card agreement

In addition to having cash back or rewards on generic categories such as Dining, Grocery or Gas, an issuer can appeal to a specific user segment by having a special benefit dedicated to a brand. That’s why you see a Co-branded credit card from Walmart, Southwest, Costco or Scheels. These brands work with an issuer to slap their brand on a credit card. What do the parties in this type of partnership get in return?

From the Brand perspective, it offers to an issuer Marketing Assistance and an exclusive feature to appeal to credit card users. To the fans of Costco, a Costco credit card with 5% cash back; which should be very unique, is an enticing product to consider. Why saying no to extra money when you already shop there every week without it already? Moreover, a Brand can also be responsible for rewards at or outside their properties. For instance, Costco can pay for rewards at Costco stores or on Costco website or purchase outside Costco or the combination of all. It varies from one agreement to another.

From the Issuer perspective, it has to compensate the Brand in the form of Finder Fee, which is a small fee whenever there is a new acquired account or a renewal, and a percentage of purchase volume; which you can consider it a tax. The issuer, of course, has to take care of all the operations related to a credit card such as issuing, marketing, customer service, security, regulatory compliance, fraud, you name it. In return, issuers have an exclusive benefit to appeal to credit card prospects. They will also receive all the revenue, net the compensation to the Brand, as I described in the first section. Therefore, the longer a customer stays with an issuer and the more he or she uses the card, preferably revolves as well, the more profitable it is for the issuer.

| Brand | Issuer | |

| What to offer | – Marketing Assistance & brand appeal – Rewards | – Finder fee (a fixed fee for every new account and/or a lower fee for every renewal – In some cases, issuers fund rewards as well – All operational needs related to a credit card – A percentage of purchase volume |

| What to gain | – Finder fees – A tactic to increase customer loyalty – A percentage of purchase volume from the issuer | – An exclusive feature to appeal to credit card users – Revenue, net all the compensation to the Brand |

Typical credit cards

Based on my observations, there are three main credit card types on the market which I assign names for easier reference further in this article:

- The Ordinary: cards that have no annual fees, but modest benefits such as 1% or 1.5% cash back on everything. These cards are usually unbranded

- The Branded: these cards are Co-Branded credit cards that are issued by a bank, but carry a brand of a company. These cards can come with or without an annual fee, but they reward most generously for purchase at the company’s properties, such as 3-5x on every purchase. Then, there is another reward scheme for a generic category such as 2-3x on dining/gas/grocery/travel. Finally, there is a 1x on everything else

- The Premier: these cards are often accompanied by a high annual fee. To make it worthwhile for users, the issuers of these Cards hand out generous benefits and/or signing bonus. For instance, a Chase Sapphire user can get 60,000 points after spending $4,000 the first 90 days.

All the three types usually work well with mobile wallets and have a delay on when rewards are posted (usually it takes a cycle). This delay isn’t particularly enticing to users because when it comes to benefits, who would want to wait?

Apple Card

Apple Card is a credit card issued by Goldman Sachs and marketed by Apple. The card has no fees whatsoever, but comes with some special features:

- An expedited application process right from the Wallet app on iPhones

- Instant cash back in Apple Cash – no delay

- Native integration with Apple Pay

- 3% cash back on all Apple purchases

- 12-month 0% interest payment plan for select Apple products

- 2% on non-Apple purchases through Apple Pay

- 1% on non-Apple physical transactions through a chip reader or a swipe

Without the 2% cash back with Apply Pay, Apple Card would very much be for Apple purchases only. But because there is such a feature and Apple Pay is increasingly popular, I think Apple Card should be something that issuers need to beware. Let me explain why

With the increasing popularity of Apple Pay, Apple Card should not be taken light

Last month, the Department of Justice filed an anti-trust lawsuit against Google. Interestingly, the lawsuit said that 60% of mobile devices in the US were iPhones. That says much about how popular Apple’s flagship product is. With the easy application process and the native integration into iPhone and Apple Pay, Apple Card has a direct line to consumers. Once a consumer contemplates buying an Apple product, it’s impossible not to think about getting an Apple Card and reaping all the benefits that come with it. With the existing iPhone users, the extensive media coverage and the marketing prowess of Apple will surely make them aware of Apple Card. Therefore, other issuers are on a back foot when it comes to acquiring customers from iPhone user base. However, most people have multiple cards, so one can argue that this advantage may not mean much. To that, I’ll say: fair enough. Let’s look at other aspects.

If you compare Apple Card to the Ordinary above, Apple Card clearly has an advantage. In addition to the 3% cash back on Apple purchases, there is also 2% cash back on other purchases through Apple Pay, higher than the 1.5% offered by the Ordinary. Granted, Apple Pay’s presence is a requirement, but as more and more merchants and websites use Apple Pay, it’s no longer relevant. It almost becomes a given and this advantage Apple Card has becomes more permanent. Besides, Apple Card has no fees and can issue cash back immediately after transactions are approved, compared to a host of fees and a delay in rewards from the Ordinary.

Between Apple Card and the Branded, it’s harder to tell which has the advantage. It depends on the use cases. For on-partner purchase (purchase on the brand’s properties), Apple Card has no chance here as the reward rate from the Branded is much higher: 3-5x compared to 2x from Apple Card. However, things get trickier when it comes to non on-partner purchase. If a non-on-partner purchase warrants only 1x reward from the Branded, Apple Card has an advantage here as it can offer 2x rewards with Apple Pay. If a non-on-partner purchase warrants 2x reward from the Branded, the question of which card consumers should favor more rests on these factors:

- How much do consumers care about receiving immediate cash back?

- Can the transaction in question be paid via Apple Pay?

- How much are consumers willing to go back and forth in their Apple Pay’s setting?

Between Apple Card and the Premier, the comparison depends on which time frame to look at. Within the first year on book, the Premier should have an advantage. No one should pay $95 for a card and does not have a purchase plan in mind to get the coveted signing bonus. In other words, savvy users should plan a big purchase within the first 90 days to receive thousands of points. In this particular use case, the Premier clearly is the better card. However, it gets trickier after the first year on book. Without a signing bonus, users now have to determine whether it’s worth paying an annual fee any more. The usual benefits from the Premier should be better than Apple Card’s, but the high annual fee and the delay in rewards may tip the cost-benefit analysis scale to a tie or a bit in favor of Apple Card.

Given my arguments above, you can see how Apple Card, provided that Apple Pay becomes mainstream, can become a formidable competitor to issuers. Apple Card may not affect the acquisition much, but it may very well affect the purchase volume and usage of other issuers’ cards, and by extension, profitability because, as I mentioned above, issuers’ revenue come partly from interchange. In other words, Apple Card should not be taken lightly as a gimmick or a toy feature at all.

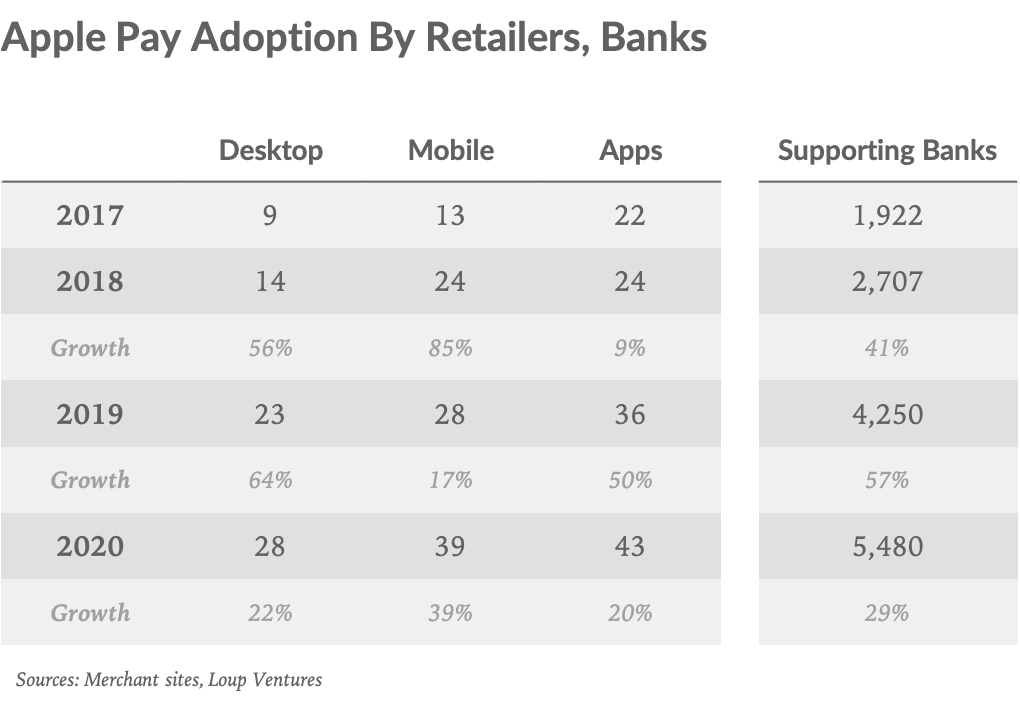

How popular is Apple Pay?

In Q1 FY 2020, Tim Cook revealed that Apple Pay transactions doubled year over year and reached a run-rate of 15 billion transactions a year. Loup Venture estimated that 95% of the US top retailers and 85% of US retail locations adopted Apple Pay.

Source: Loup Ventures

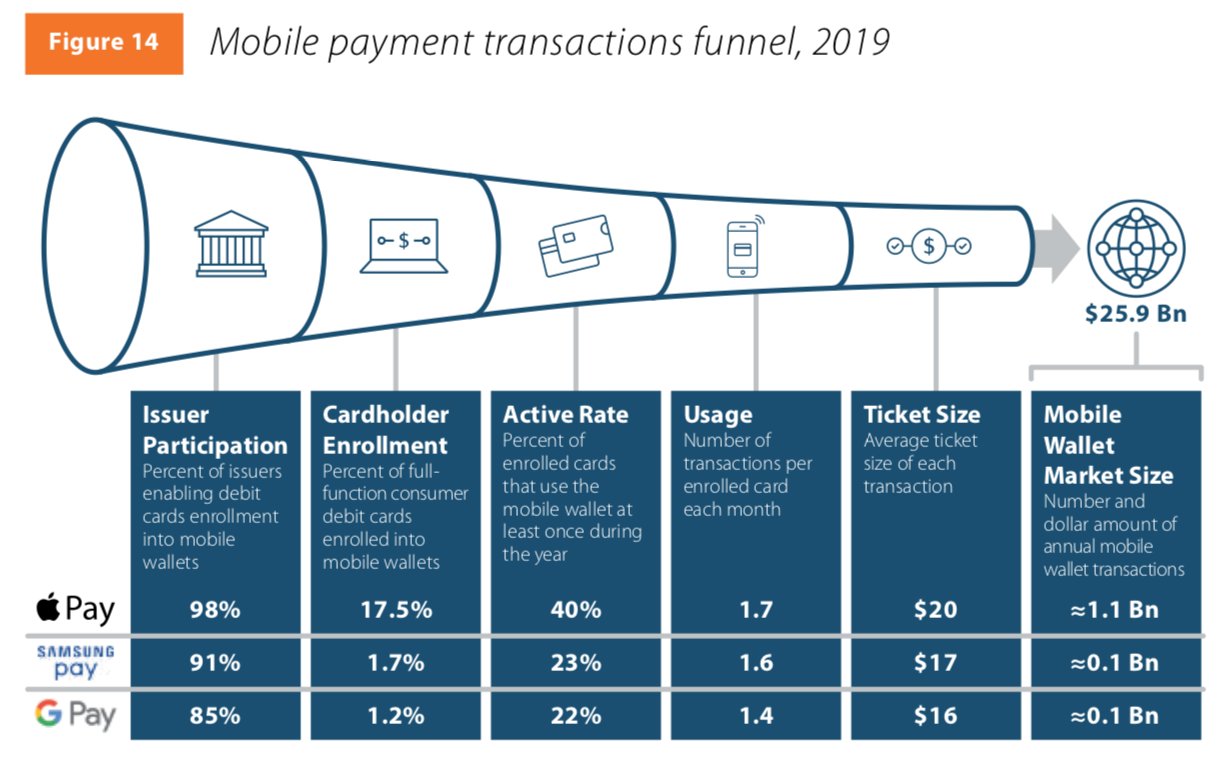

According to a research by Pulse, in the US in 2019, there was around $1.3 billion worth of debit transactions through mobile wallet, $1.1 billion of which came through Apple Pay. This level of popularity will leave retailers and merchants with no choice, but to have Apple Pay-enabled readers; which in turn will gradually benefit Apple Card.

Disclaimer: I own Apple stocks in my personal portfolio

Leave a comment