Disney’s enormous potential in the streaming area

On its 2020 Investor Day, Disney showed everybody that it was going to be a force to be seriously reckoned with in the streaming business in the years to come. The four hour presentation was packed with announcements on upcoming titles, business updates and impressive revised projections. Netflix fans always point to the fact that the streamer won the streaming war by having a much bigger subscriber base than any other competitors. The big subscriber base allows Netflix to operate at a much lower cost advantage. For the same investment of $1 billion in content, a base of 100 million subscribers will lead to a cost of $10 per subscriber while a base of 10 million will result in a cost of $100/user. As each user brings in monthly revenue, a lower cost structure enables a higher profitability which, in turn, enables more money in content creation which, in turn, leads to more appeal to consumers.

Netflix, with 195 million subscribers, enjoys a cost advantage to other competitors. It already got over the peak operating losses and has seen positive free cash flow for the past three quarters, despite spending a massive amount of money on content. I believe none of the other streamers achieved that feat yet. In short, Netflix has an invaluable head start.

Enter Disney Plus. Last year, Disney forecast to have around 60 to 90 million subscribers by the end of FY 2024. They just announced that the number of Disney+ subscribers was 86.8 million as of December 2, 2020. Critics say that Disney reached this number due to a huge subsidy in the Indian market which constitutes 30% of the base now. Well, that’s true, but it’s hard to reach the mass market in a short period of time and keep the price high. You have to take a multi-step approach. Expand the base first, add more value and increase the price.

That’s what Disney is doing now. With more than 86 million subscribers in the pocket, the company is planning 100+ titles per year for the next few years, coming from established brands such as Marvel, Disney, Pixar, Star Wars and National Geographic. At the same time, Disney is addressing the Average Revenue Per User (ARPU) issue with a price hike of $1/subscriber/month in the US and €2/subscriber/month in EU starting March 2021 and with a Premier Access model. The Premier Access model lets subscribers gain first access to select titles before everyone else for an additional fee. A few months ago, Mulan cost Disney+ subscribers an additional fee of $30 in exchange for first exclusive access.

As a result, Disney expects to have around 230-260 million Disney+ subscribers by the end of FY2024. Within one year, they revised the forecast from 60-90 to 230-260 million subscribers for the same time frame. There must have been some sandbagging, but I believe that even the folks at Disney didn’t expect to have such a big leap. The new figure should put Disney+ in the same conversation as Netflix by the end of FY2024 and well ahead of the other streamers. The profitability expectation remains at the end of FY2024, unchanged from the Investor Day last year, even though the legendary company expects to at least double its content cost by FY2024. The same upgrade in expectation is similar for ESPN+ and Hulu

| Investor Day 2019 | Investor Day 2020 | |

| Disney Plus | ||

| Subscriber | 60-90 million by FY 2024 | 230-260 million by FY 2024 |

| Profitability | FY 2024 | FY 2024 |

| Hulu | ||

| Subscriber | 40-60 million by FY 2024 | 50-60 million by FY 2024 |

| Profitability | FY 2023 or 2024 | FY 2023 |

| ESPN+ | ||

| Subscriber | 8-12 million by FY 2024 | 20-30 by FY 2024 |

| Profitability | FY 2023 | FY 2023 |

Those are impressive revisions, particularly given Disney’s distinct advantages. First, streaming services aren’t the only way they generate revenue and profits. Their Media and Parks segments generate considerable revenue and profit as well, especially Parks. Parks has been hit particularly hard by the pandemic, but once we go back to normal and vaccine is delivered to the public, Disney should have no problem attracting guests back to their hotels, parks and resorts. Even though the other segments don’t directly subsidize the streaming services, having them around definitely helps the company as a whole in terms of profits, revenue and cash flow. Netflix, rightfully worth every accolade for their laser focus, has only one line of business. As long as that line of business thrives, they will enjoy the full benefits of not having to spread resources like Disney. However, on the other hand, a crisis would hit them harder than Disney without any cushion.

Moreover, Disney has so many ways to appeal to consumers. First, they have an extraordinary library of content and brands, ranging from series, films, documentaries and sports. Second, they can always create value out of a bundle such as what they are doing now with a bundle of Disney+, Hulu (ads and no ads) and ESPN+. Another model that can be deployed is Premier Access as I describe above or a theatrical release in which a movie will be available first in theaters and then on Disney+. An example is Black Widow. This takes me to another strength that Disney has. A portfolio of household brands that need no introduction. When somebody mentions Avengers characters or Star Wars, there is little introduction needed. That kind of brand power helps draw viewers regardless of the medium. When Disney releases Black Widow in theaters first, they likely won’t need to persuade Marvel fans to pay to watch. What they may need to persuade them on is whether it’s worth getting into theaters when the pandemic may still be around. This brand power isn’t just limited to consumers with kids. On the 2020 Investor Day, Disney CFO revealed that more families without kids are subscribers than families with kids; which is a very interesting revelation since it was assumed that Disney would appeal parents through content for kids.

In short, I believe the future is bright for Disney’s streamers and the company as a whole. That doesn’t mean that I think Netflix is doomed. The sizeof the market and the consumer behavior should allow these two behemoths to co-exist. As long as other streamers have the financial ammunition to compete, they should have a seat at the table, but this should be a two-race non-zero-sum market. The winners should be consumers who will get more choices and talents, including actors, directors, creators, storytellers and so on, who will be sought after as streamers strive to create quality content.

Adobe’s extraordinary story continues

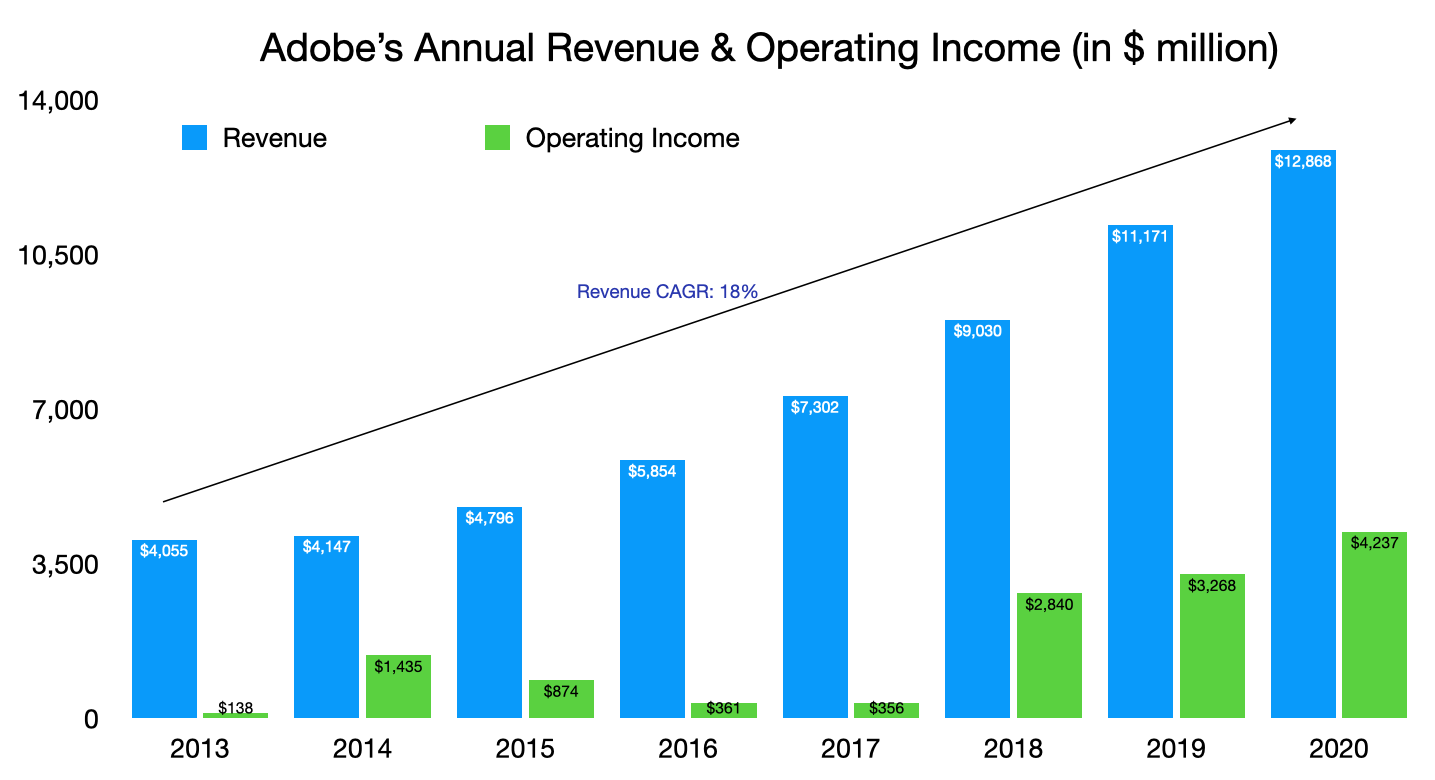

Adobe may not be as popular as some of its products. It’s the creator of Photoshop, Illustrator, InDesign and PDF. It also owns Behance, the LinkedIn of creative folks. Its less known products include Marketing Solutions, such as Email Marketing, eCommerce and Customer Analytics, and Document Solutions such as eSignatures or Document Intelligence Services. Besides its famous products, Adobe is also known for being the trailblazer in transitioning to a Software-as-a-Service model. The transformation started in about 2011 or 2012, and it has been the case study as well as the envy of established software makers all over. Adobe’s revenue grew at a CAGR of 18% from 2013 to 2020, reaching almost $13 billion in 2020. More impressively, its FY 2020 Operating Income was even higher than its revenue in FY 2014. Additionally, its Operating Margin in FY 2020 was 32%, the highest in the last 6 years.

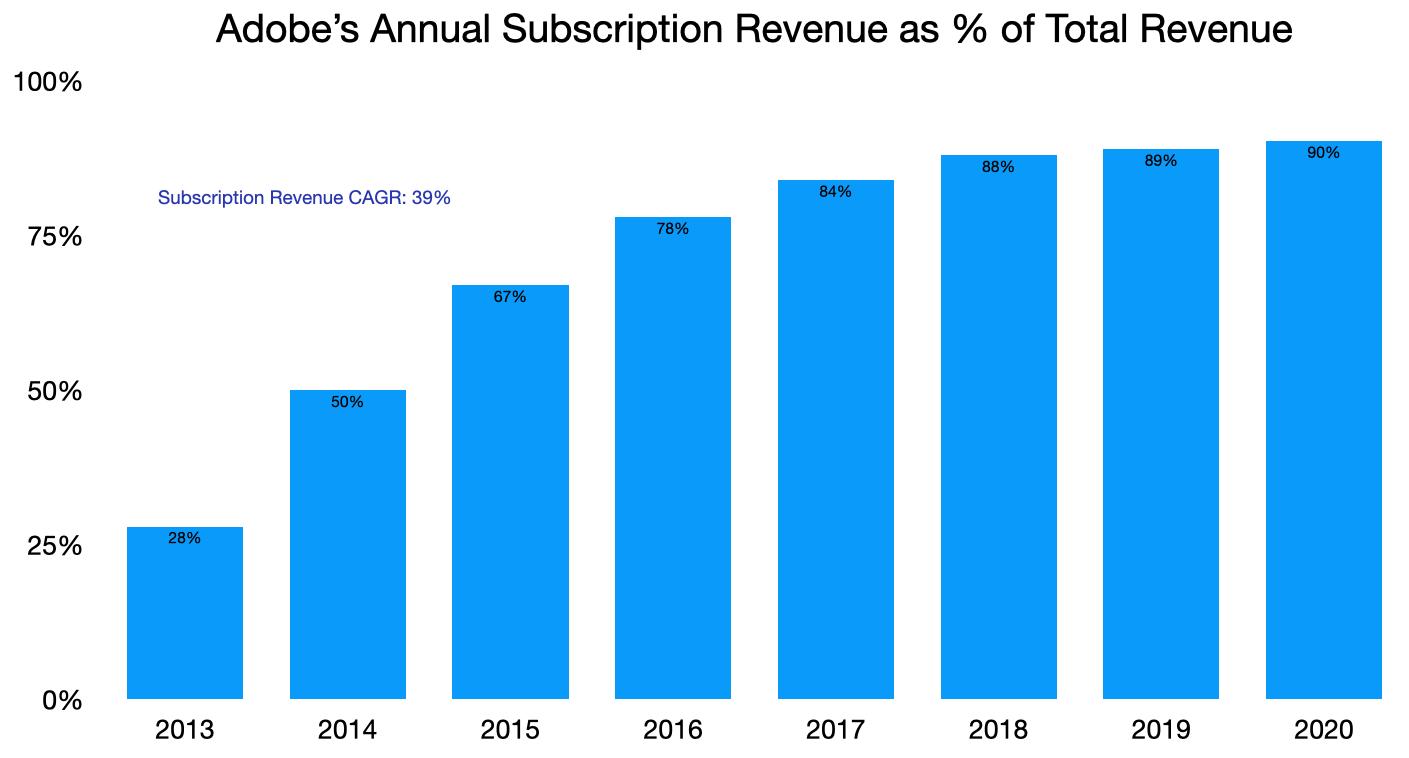

The transformation was best reflected in Adobe’s subscription. In 2013, only 28% of the company’s top line came from subscriptions which have higher margin and stickiness. In FY 2020, the figure stood at 90%. In terms of CAGR of subscriptions’ absolute dollars, it is an extraordinary 39%.

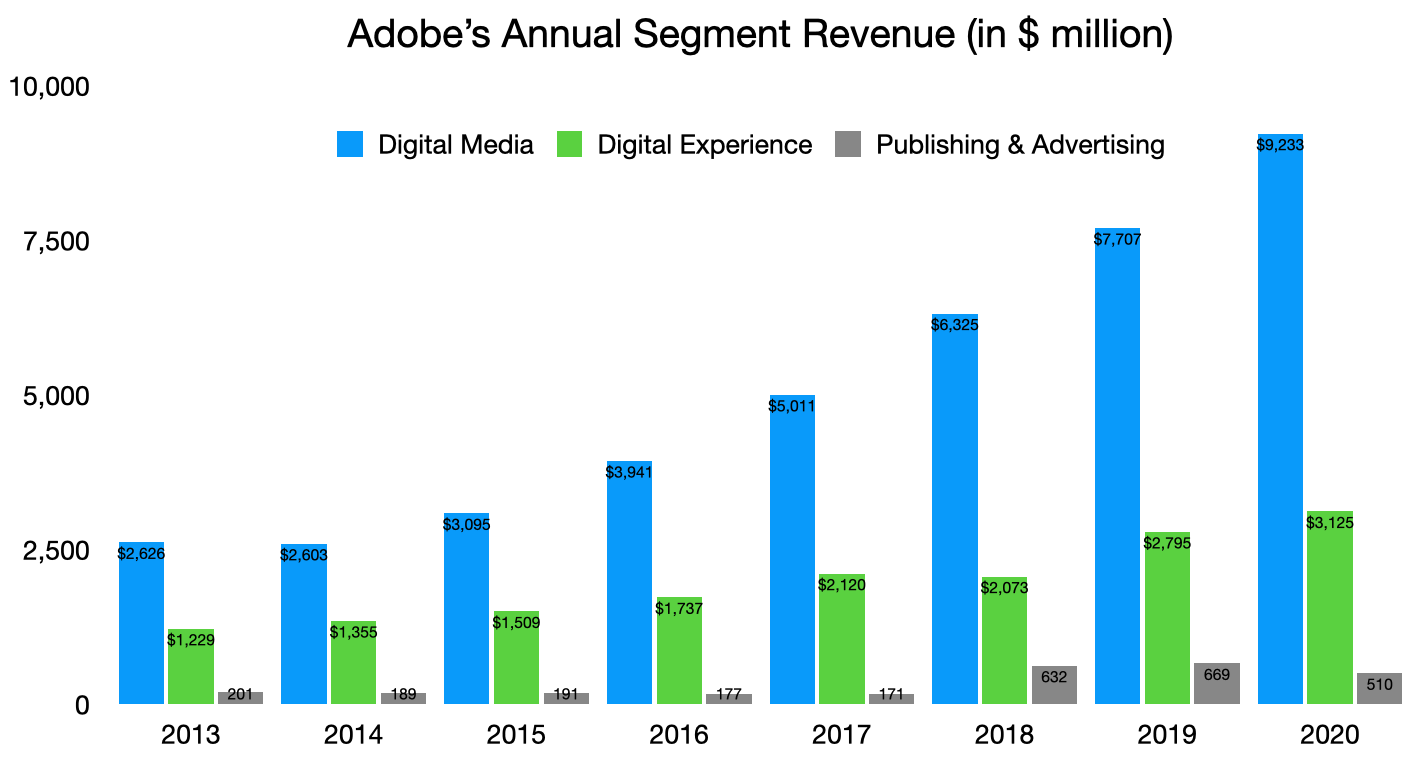

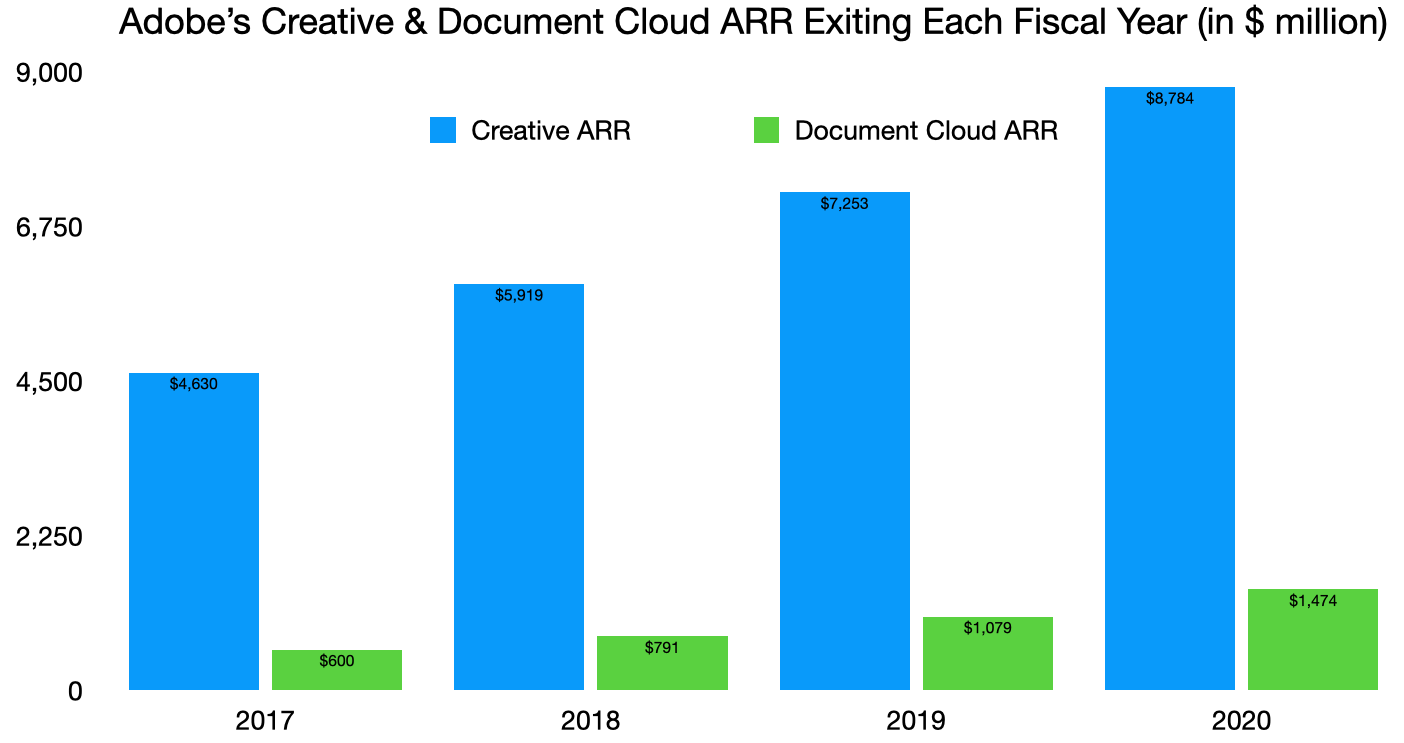

Among the main business segments, Digital Media is the biggest and certainly the driver of growth at Adobe. Since 2013, Digital Media’s revenue grew by almost 300%. Within Digital Media, Creative and Document Cloud Annual Recurring Revenue more or less doubled in the last 4 years.

While Digital Experience, which includes B2B solutions, faces stiff competition from the likes of Salesforce, Adobe is clearly the market leader with their Digital Media offerings. How many designers or creators in the world don’t have an Adobe product? Which document format can replace the de factor PDF when it comes to official documents? Their Digital Media products, whether it’s Creative Cloud or Document Cloud, are popular among subscribers. According to Adobe’s 2020 Investor Day

- 75% individual subscribers in 2020 were completely new to Creative Cloud

- Individual subscribers made up more than half of the Creative Cloud’s revenue

- 2 billion mobile + desktop devices were installed with Acrobat Reader

- 75%+ individual subscribers in 2020 were new to Acrobat

- Mobile IDs were more than 300 million in total as of Q4 FY 2020, with more than 175 million created

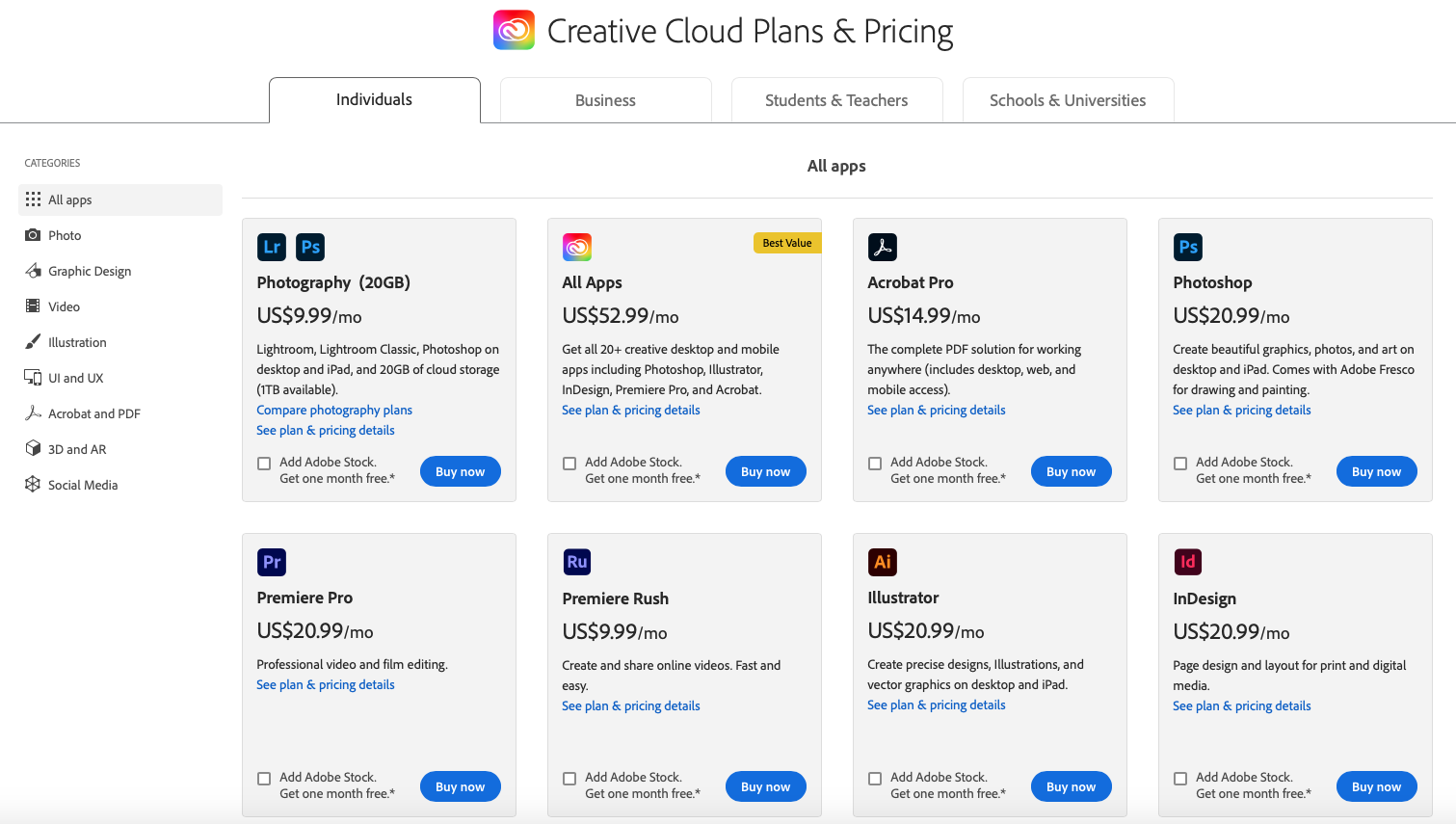

- More than 60% of Creative Cloud ARR is based on All Apps subscribers. An All-App subscription costs $53/month, much more expensive than individual app subscriptions.

All these data points show how much customers love Adobe products. As more and more people use Adobe products, it helps the company establish an invaluable network effect. If you are a designer collaborating with other designers and businesses that are used to working with Illustrator and Photoshop, it’s difficult not to use those applications. That’s perhaps the strongest moat Adobe has. There may be better alternatives than their products on the market, but those products don’t have the brand names, the popularity, the established sales channel and the network effect that Adobe has. Once a company can establish this kind of relationship and network effect, its priority should be to continue add values to subscriptions to keep the churn low. In other words, as long as the existing subscriber base doesn’t shrink, Adobe’s revenue will only grow. Any new subscribers acquired will only add to their fortune.

Disclaimer: I own both Disney and Adobe in my personal portfolio.

Leave a comment