Launching a credit card product is similar to putting together a jigsaw. There are many pieces: how to appeal to customers, which customers are an issuer’s likely target, what a good experience looks like, how an issuer can make money and how a card can compete with existing products on a market. In this post, I’ll go over my thoughts on the economics of a credit card, the main credit card types that I see on the market (excluding those debit cards that have credit card functions), the appeal of Apple Card and how different cards compare to one another.

Economics of a card

An issuer essentially generates revenue from three main sources with a credit card: interest payment when customers don’t pay off their balance, fees (late fee, annual fee, cash advance fee, balance transfer fee, foreign transaction fee and others) and interchange. Interchange is a small percentage of a transaction that a merchant pays to a card issuer whenever a customer uses a credit card to pay. The more spend is accrued, the more interchange issuers generate. Interchange rates are determined by networks such as Visa, Mastercard, Discover and American Express. The exact rates depend on a lot of factors: the industry or category that a merchant is in, what type of card (high end or normal) is being used, regulations (Europe imposes a limit on interchange rates, unlike the US) and how a customer uses the card to pay (swipe, chip, mobile wallet, online, phone..).

On average, some categories such as Airlines, Restaurants, Quick Restaurant Services, Hotels or Transportation have an interchange rate somewhere between 2% – 3%. Other categories such as Gas and Grocery, especially at Walmart, Target or Costco usually yield a very low interchange rate around 1% – 1.4%. Any credit card that offers higher than 3% in cash back in a category likely loses money on that category as the interchange cannot make up for the reward liabilities. Issuers are willing to offer 3-5% cash back, knowing that they lose money on that front, because they are banking on the assumption that the money that they make up from other sources will offset that loss. Specifically, they are likely to make money on categories with 1%. For instance, if you buy clothes or pay for a subscription online or buy something from a Shopify store, your card issuer is likely to make at least 1% in interchange, after they give you 1% in cash back. Additionally, issuers that offer a rich reward scheme usually impose an annual fee to offset the reward liabilities and the signing bonus that they use to acquire customers.

Hence, cards with no annual fee offer a cash back between 1.5 – 2%. They can’t afford to go higher than that because the maths would unlikely add up. Cards that have an annual fee often come with high rewards and a big bonus. While a big bonus can be an attractive tool to acquire customers, it incentivizes short-term purchase bursts and unintentionally attracts gamers, customers who receive the bonus, cash it out and either become a ghost, if they don’t have to pay an annual fee, or close out the card for good. There are a lot of gamers and gamers aren’t profitable to issuers. However, issuers still dole out a big bonus and attractive rewards because they think that there are customers that stay for a long term and can provide the interest income and fees that issuers need.

Three essential types of credit cards

I call the first type of cards the “Everyday Card”. Examples of this category include Blispay and Citi Double Cash Back. These cards offer a standard rewards rate on every purchase category (1.5% to 2%) with no annual fee. There is usually a 3% foreign transaction fee and there is no signing bonus. What makes Everyday Card appealing is that customers do not need to remember the complex rewards structure. They can just “set it and forget about it”. It earns them respectable rewards on every purchase, even at Walmart.

The second type of cards is the “No Annual Fee With Bonus”. Examples of this category are Discover It Cash Back, Freedom Unlimited or Freedom Flex. These cards’ highest reward rate is usually 5% on a certain pre-determined category that tends to yield a high interchange rate. In some cases, this 5% rate can rotate every quarter, keeping it interesting for customers and making them locked in if they want to activate a preferred category. There is a signing bonus for new customers. Some cards reward customers with a few hundred dollars in a statement credit if they spend a certain amount in the first 90 days. This mechanism is designed to make customers locked in early. The issuers bank on the assumption that once customers earn their signing bonus, they will stick around to keep those rewards points alive. However, it’s not uncommon for customers to cash out their rewards and become inactive afterwards.

Discover’s signing bonus is designed to keep customers active during the first calendar year. They promise to match the cash back rewards at the end of the first year, but the bonus is a one-time occurrence and doesn’t repeat. This mechanism may keep customers active longer than what an outright statement credit does, but customers can always leave after the first year.

The last type of cards usually comes with an annual fee. Examples are Chase Sapphire Preferred or Bank of America Premium Rewards. Cards in this category come with a signing bonus after qualifying conditions are met and with a rich rewards structure. To offset expenses, issuers impose an annual fee. Customer acquisition may not be an issue with cards in this category, but will customers stay around after the signing bonus? Or are customers happy enough to pay a high annual fee every year? Also, these cards’ reward rate is high only in categories with higher interchange rate such as travel or dining. The rate is pretty light (1%) in other categories. While this approach appeals to a specific segment of customers, for customers that want “to set it and forget it”, does it still carry that same appeal though?

If you find credit cards complex and confusing, that’s normal because they are usually designed that way

Most credit cards can be pretty complex and confusing to customers. Let’s start with rewards. A tiered reward structure forces customers to mentally remember all the combinations of categories and rates. If customers have multiple cards in their wallet as they often do, it’s not an easy ask. Of course, there are folks that make a living in maximizing rewards, but that doesn’t work for the rest of us. In addition, it’s not always clear to customers how to categorize merchants. Merchants are categorized by Merchant Category Codes. These codes help issuers set up rewards and help networks determine interchange rates. MCCs are known in the banking industry, but to an ordinary customer, they don’t usually mean much. In some cases, issuers provide a list of qualifying merchants, but they can’t list all the available merchants and the practice is not ubiquitous.

Moreover, reward redemption can be a time-consuming process. Points or cash back earned in this cycle have to wait at least till the cycle ends before they are available for redemption. It can take longer in some cases, especially when it comes to signing bonuses. Here is a list of how long it takes for points to post at different issuers, compiled by Creditcards.com

| How long it takes to redeem the signing bonus? | How long it takes to redeem spending rewards | |

| Amex | 8-12 weeks after a customer hits the spending requirement | When the current cycle ends |

| BofA | At the close of the billing cycle when the minimum spend is met | When the current cycle ends |

| Capital One | Within 2 cycles of when the spending requirement is met | Up to 2 cycles |

| Chase | Up to 6-8 weeks after a customer hits the spending requirement | When the current cycle ends |

| Citi | 8-10 weeks after a customer hits the spending requirement | When the current cycle ends. With Citi Double Cash Back Card, it can take a bit longer if customers don’t pay in full |

| Discover | Within 2 cycles after a customer hits the spending requirement | When the current cycle ends |

| US Bank | Up to 2 billing cycles after a customer hits the spending requirement | When the current cycle ends |

| Wells Fargo | Up to 2 billing cycles after the qualifying period | When the current cycle ends |

The final point in rewards is that issuers tend to deceptively inflate the rewards by posting numbers in points, instead of dollars. Understandably, 100 points sounds much better than $1, even though they have the same value. Nonetheless, it creates an unnecessary level of complexity for customers to mentally convert points into cash, especially when the reward value is big.

Rewards aren’t the only source of frustration for credit card customers. Credit cards are essentially loans on which you may or may not have to pay interest. However, issuers hope that customers will incur interest and fees (as long as they don’t charge off). How often are fees prominently and clearly marketed as rewards? How often do you see in advance the potential interest payment if you don’t pay off your balance? Here is a study by Experian on the concerns that consumers have about credit cards

Apple Card is designed to do something different

Apple launched Apple Card in August 2019 in collaboration with Goldman Sachs. Customers can apply for an Apple Card right from the Wallet app, which is pre-loaded on an Apple device. The preloading is a significant advantage as customers don’t need to either load another bank app or search for a website and apply for a card. As soon as an application is approved, customers can use their Apple Card immediately either by holding your device near an NFC-enabled reader or paying online. With Apple Card, cardholders earn 3% cash back on purchases at Apple and strategic partners such as Exxon, T-Mobile, Walgreens, or Nike, 2% cash back on others purchases using Apple Pay and 1% cash back using the titanium physical card. The 2% cash back on other purchases can be appealing, but not every offline or online merchant allows Apple Pay.

The biggest selling points of Apple Card are transparency and simplicity. Take their no-fee structure as an example. There is no fee involved with Apple Card. No annual fee, no foreign transaction fee, no over-the-limit fee and no late fee. While Apple remains coy on cash advance fees, their special clientele may not use the mainly virtual Apple Card for this specific reason much.

The simplicity also goes into their daily cash back. Typically, cash back earned through a credit card can take weeks to be registered and redeemed. Points or cash back earned this cycle must wait at least till the cycle ends before they are available for redemption. With Apple Card, cash back is earned daily in Apple Cash. As long as transactions are posted, customers can see the earned amount reflected in their Apple Cash. In real money term not in points. This takes away an unnecessary step for customers to mentally convert points into cash. Furthermore, Apple Cash can be used at any time, either in a person-to-person transaction, in a deposit back to a checking account or to pay back the outstanding balance in Apple Card.

In terms of transparency, Apple Card tells customers how much interest they are paying when making a payment. And their APR is on par with other issuers’. In the Wallet app, customers can determine how much of the outstanding balance they want to pay. Depending on the amount, Apple will let customers know in advance their interest so that they can make an informed decision. It is in contrast to what almost all other issuers do.

Source: Apple

Apple Card only works with iOS devices and Apple Pay can be a challenge for elderly or less tech-savvy customers. Nonetheless, no card is perfect for everybody and the transparency and simplicity can teach us a lesson on how to craft a good customer experience. Despite being available only in the US and all restrictions above, Apple Card’s portfolio balance grew from $2 billion in March 2020 to $3 billion in September 2020 and roughly $4 billion at the end of 2020. Not bad for a portfolio with one card that is restricted to iOS devices.

Annual fee or no annual fee? Appealing and complex or straightforward and simple?

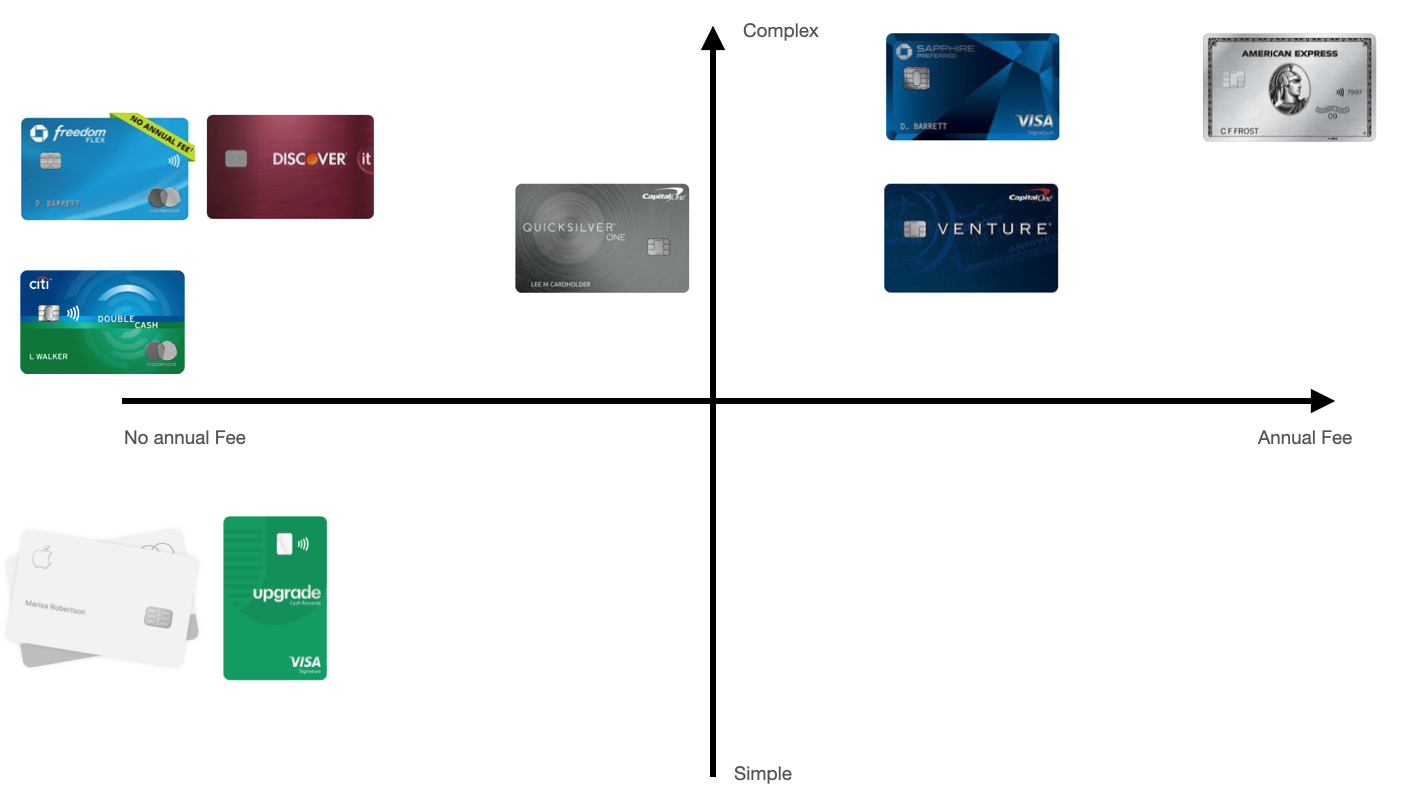

A good practice in positioning is to use a 2×2 matrix. In this case, I’ll look at Apple Card and the three main credit cards mentioned above through whether they are easy to use and whether they have an annual fee.

Let’s look at the positioning chart above. On the top right corner, we have an ultra-luxury card such as The Platinum Card from Amex. This card’s annual fee runs up to $550 and while rewards rate can range from 1x to 10x, it is not easy to remember all the details or to redeem rewards. On its left side, we have cards such as Capital One Venture and Chase Sapphire Preferred. These cards’ annual fee is $95, lower than the Platinum Card’s. Similarly, the complexity of cards such as Chase Sapphire Preferred is still high. Capital One Venture has 2x rewards rate on every purchase, making it less complex to use for some users, but it’s still time-consuming to redeem cash back.

Moving further left, there is Capital One Quicksilver. This card’s annual fee stands at $39 and it offers 1.5x on every purchase. It’s in the middle of the spectrums. On the “no annual fee” side, we have two groups. The first group features cards such as Freedom Flex and Discover It Cash Back. These cards offer a 5x reward rate, but it rotates every quarter and to some customers, that can add some complexity. The other group features cards such as Citi Double Cash Back and FNBO Evergreen. These cards have no annual fee and offer 2x on every purchase. Nonetheless, they still have a complex fee structure and a reward redemption process that can be improved.

The point here is that it’s very competitive on the top half of the chart. All these cards have their own unique selling points that appeal to different customer segments. What they do have in common is that their fees and reward redemption are pretty complex.

On the other side of the x-axis, there are Apple Card and Upgrade Card. Even though it’s straightforward to use Apple Card as there is no fee and cash back is earned daily, the use of Apple Card depends much on whether customers have an iPhone and whether merchants enable Apple Pay. 40% of mobile users in the US don’t own an iPhone and as discussed above, older and less tech-savvy customers may not find Apple Pay comfortable. Without Apple Pay, the titanium card itself earns customers a paltry 1% cash back.

Upgrade Card is a credit card issued by Sutton Bank, a medium sized bank in Ohio with $500 million in assets, and marketed by Upgrade. There is no fee with Upgrade Card. Here is what the company claims on its website

Not all traditional credit cards charge fees. However, creditcards.com’s 2020 Credit Card Fee Survey found that the average number of fees per card is 4.5. For example, the 2019 U.S. News Consumer Credit Card Fee Study found that the average annual fee (including cards with no annual fee) is $35.23, the average late fee is $36.34 and the average returned payment fee is $34. 01. The Upgrade Card charges none of these fees. Over 90 percent of cards charge balance transfer fees and cash advance fees. The Upgrade Card enables you to transfer cash from your Personal Credit Line to your bank account with no fees.

Source: Upgrade

With Upgrade Card, customers earn 1.5% cash back on all purchases as soon as customers pay off balance. The 1.5% cash back rate is lower than what Apple Card customers earn using Apple Pay, but on the other hand, Upgrade Card is device-agnostic and doesn’t rely on any mobile wallets. Hence, it is more accessible. However, Apple Pay allows customers to earn and use rewards daily while Upgrade Card only allows customers to redeem rewards after they make full payments.

According to the book The Anatomy of The Swipe, medium sized banks are essentially unregulated and can charge a higher interchange rate than big regulated banks. Hence, it’s very likely that Upgrade Card’s interchange rates are higher than those of cards issued by the likes of Chase or Capital One. The higher interchange rates can help offset rewards liabilities and generate revenue.

In fact, I am surprise to find no product like Upgrade Card from big banks. I suspect it would take a huge investment in infrastructure by legacy banks to offer the Daily Cash feature that Apple Card has. But legacy banks can essentially waive all fees like Upgrade Card does. While the likes of Chase, Discover or Capital One have more expenses than a smaller platform like Upgrade, they also have more popular brand names than Upgrade; something that would help tremendously in customer acquisition.

In summary, the credit card world is highly competitive. If an issuer follows the conventional way of launching a credit card, it will surely have a lot of competition and little to differentiate itself from competitors. In the upper half of Figure 4 above, I do think all the concepts and variations of rewards and economics have been tried. To be different, an issuer has to think differently and appeal to customers more with a superior customer experience (easy and simple to use) and less with complex features.

Leave a comment