Uber is well on track to a full recovery. Delivery continues to be the bright spot

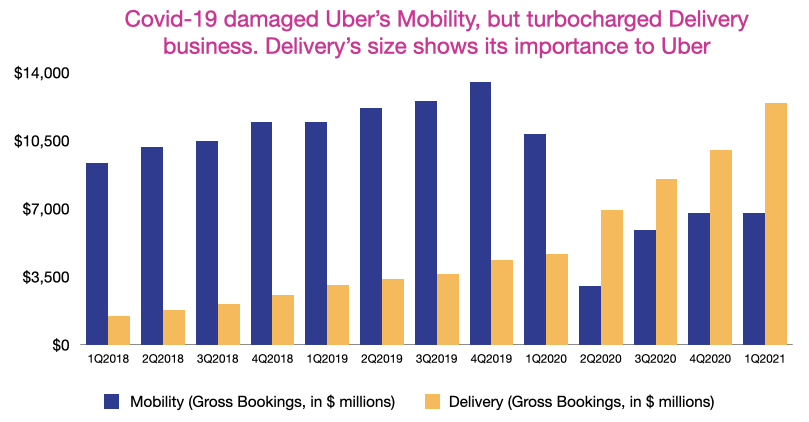

Yesterday, Uber released their financial results for Q1 FY2021. In general, the overall business mostly recovered from the impact of the pandemic. Even though it made fewer trips and less revenue than last year, gross bookings rose by 24%. Mobility Gross Bookings continued to be down year over year as countries are still battling Covid-19. On the other hand, Delivery Gross Bookings increased by 166%, up to $12.5 billion from $4.7 billion a year ago, due to strong demand. To put it in perspective, Uber generated almost as much Gross Bookings in Delivery in Q1 2021 as it did in the entire year of 2019.

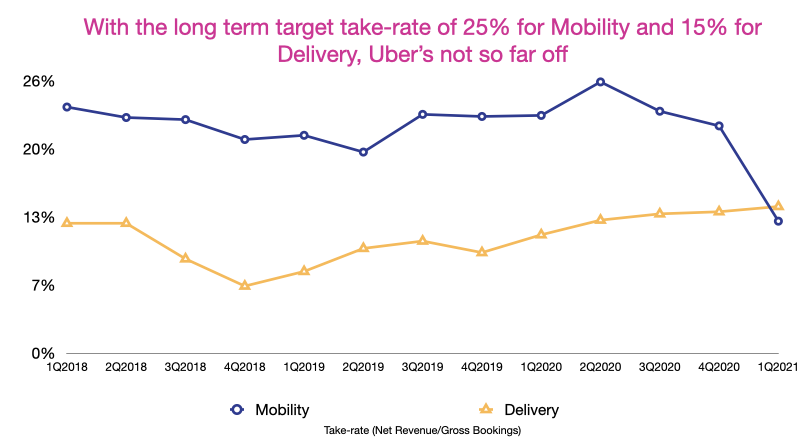

In Q1 2021, the company’s adjusted EBITDA was -$360 million, but it was up from the loss of $612 million a year ago. Mobility was still profitable, albeit down 49% YoY. Delivery and Freight remained loss-makers, but the loss narrowed compared to Q1 2020. According to Uber, Delivery was profitable on the adjusted EBITDA basis in 12 markets in Q1 2021. Take rates for Mobility and Delivery were 12.6% and 14%, respectively. Mobility’s take-rate dropped from their usual 20% range because Uber took a draw-down of $600 million for driver expenses following the High Court’s verdict in the UK that would force Uber to classify drivers as employees. Without the draw-down, Mobility take rate would be 21.5%. Delivery’s take rate has been steadily increasing since Q4 2019. As the platform continues to grow in scale and fine-tune its operations for higher efficiency, I expect to see Delivery take rate to hover around the 14-15% range.

Driver-friendly regulations can be both a threat and a blessing for Uber

This is the first time that investors could, to some extent, quantify the impact of regulatory threats on Uber’s business. Yesterday, the Biden administration rescinded the previous administration’s rule which would have made it more difficult for drivers to be considered employees. The Secretary of Labor also mentioned that drivers should be treated as employees with benefits instead of just contractors, but stopped short of announcing a concrete policy change. That’s why Uber’s executives repeatedly emphasized that they would engage in dialogues with the federal government moving forward to find an agreeable solution and that it’s not doom and gloom yet for their business.

Some are justified in their pessimism for Uber. A driver-friendly regulation would definitely hurt Uber’s bottom line in the short term. In the long run, I am not so sure. Any new regulation regarding gig workers would affect not only Uber, but also and more importantly its smaller rivals. Every company from Lyft, Instacart, Doordash to Gopuff will have to pay more personnel expenses. But few of them have the scale and resources that Uber does. Take Lyft as an example. It operates in Canada and the US only and doesn’t have a Delivery service like Uber, at least not yet. As a result, it would have a higher driver expense per order than Uber because the latter could stretch the fixed expense over many more Ride/Order. That’s a unit economics advantage that comes with operating in more markets, more verticals and at a higher scale.

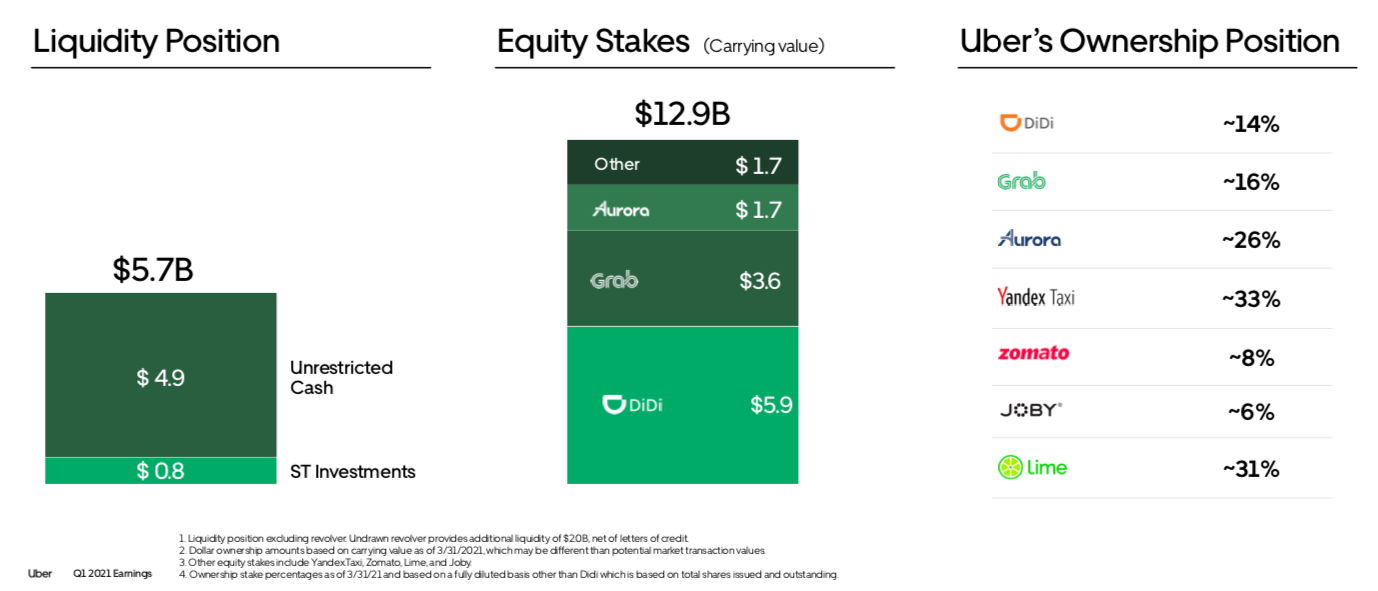

Plus, if Uber decided to pay drivers more than others, it could lock in drivers exclusively on its platform and create a driver supply problem for its smaller rivals. Fewer drivers mean slower services. Slower services lead to less satisfied customers. Less satisfied customers result in less business. That’s the vicious cycle that Uber could inflict on its smaller rivals. Plus, Uber has about $13 billion in equity in the likes of Grab, Aurora or Didi. If push comes to shove, it can sell off all of it to finance its operations, something that I doubt other delivery services can do.

Other positive developments

Uber mentioned that its Delivery would debut soon in Germany. Germany is arguably the biggest consumer market in Europe and it doesn’t make sense to not have one of its main business lines in the country. As a new market, Uber may have to take a loss in the short run to establish its presence, among local competitors. Since the CEO took over, Uber has scaled back operations in areas where it didn’t believe it had competitive advantages. If they decide to launch in Germany, there may be a good reason.

This may be the first time I remember that Uber specifically called out its advertising business. While it’s not really surprising, it has plenty of potential. As a household name that has millions of users on its platform, Uber is an attractive partner to merchants. Hence, it makes sense Uber wants to monetize its valuable real estate on its app. Advertising is a higher margin business and should help Uber with its profitability goal.

Additionally, the company also mentioned that its New Verticals (grocery, alcohol and convenient items) reached an annualized Gross Bookings of $3 billion in March. The revelation contained some caveats such as: what does “annualized” mean? What is the distribution of such Gross Bookings between grocery, alcohol and convenient items? Nonetheless, with the acquisitions of Drizly, Postmates and the partnership with Gopuff, it’s a vertical to watch out for in the future.

Leave a comment