Compared to 2 or 3 years ago, Uber is a much more focused company nowadays. Instead of stretching itself thin across the globe, losing money significantly in many markets and fighting legal battles everywhere, Uber is now present in only markets where it’s among the market leaders. In addition to selling its operations in a few markets like South East Asia, China and Russia to local rivals, Uber purposefully exited other markets that it deemed not worth fighting for. Plus, it sold operations that might have future potential, but was bleeding cash such as autonomous vehicles. I mean, innovation can be sexy and as a tech company, Uber may be tempted to pursue that, but because it hasn’t made profit as a company, it’s understandable that Uber tries to focus on what matters: Mobility, Delivery and the markets where it is confident it can generate meaningful revenue and profit.

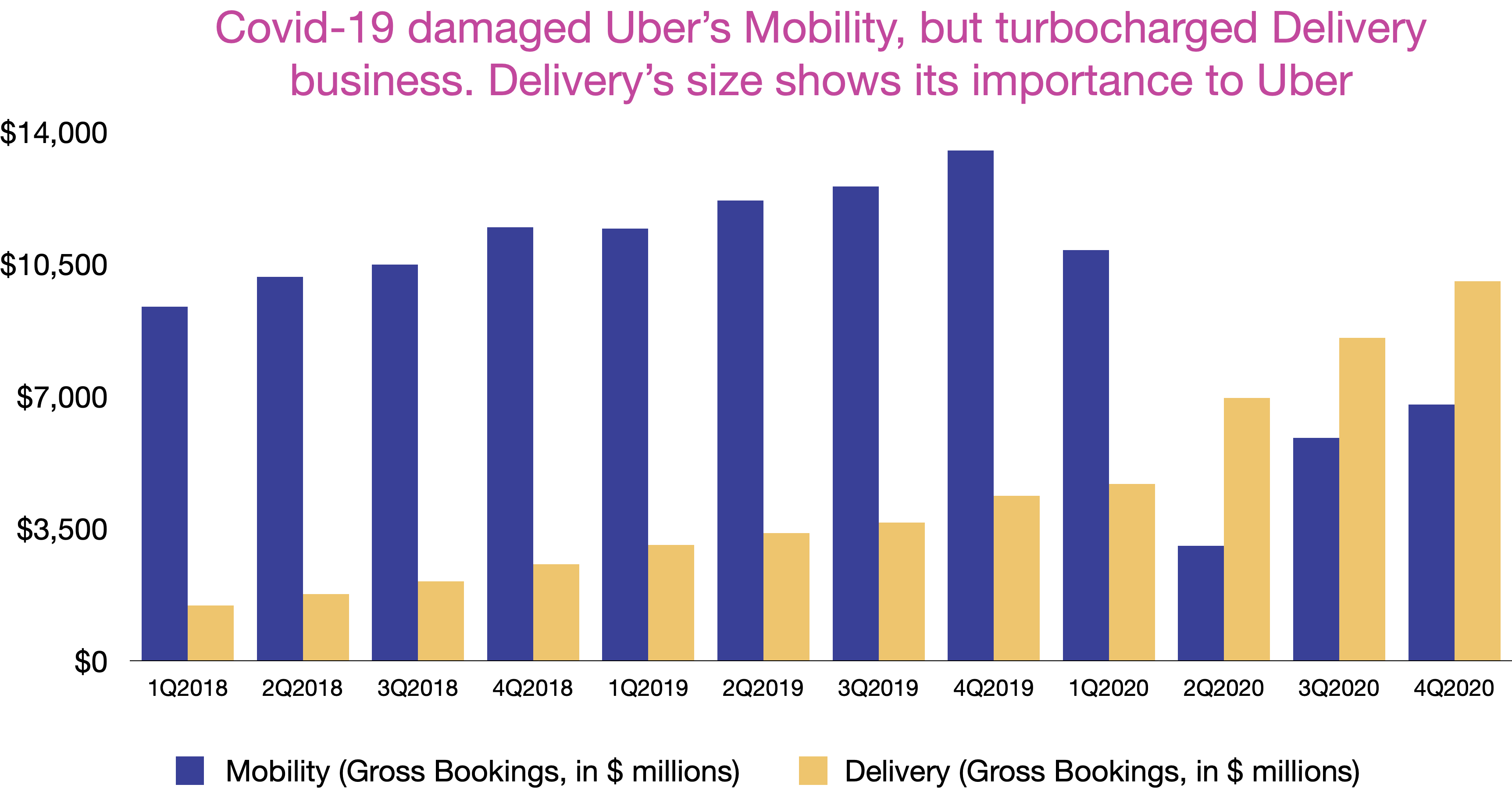

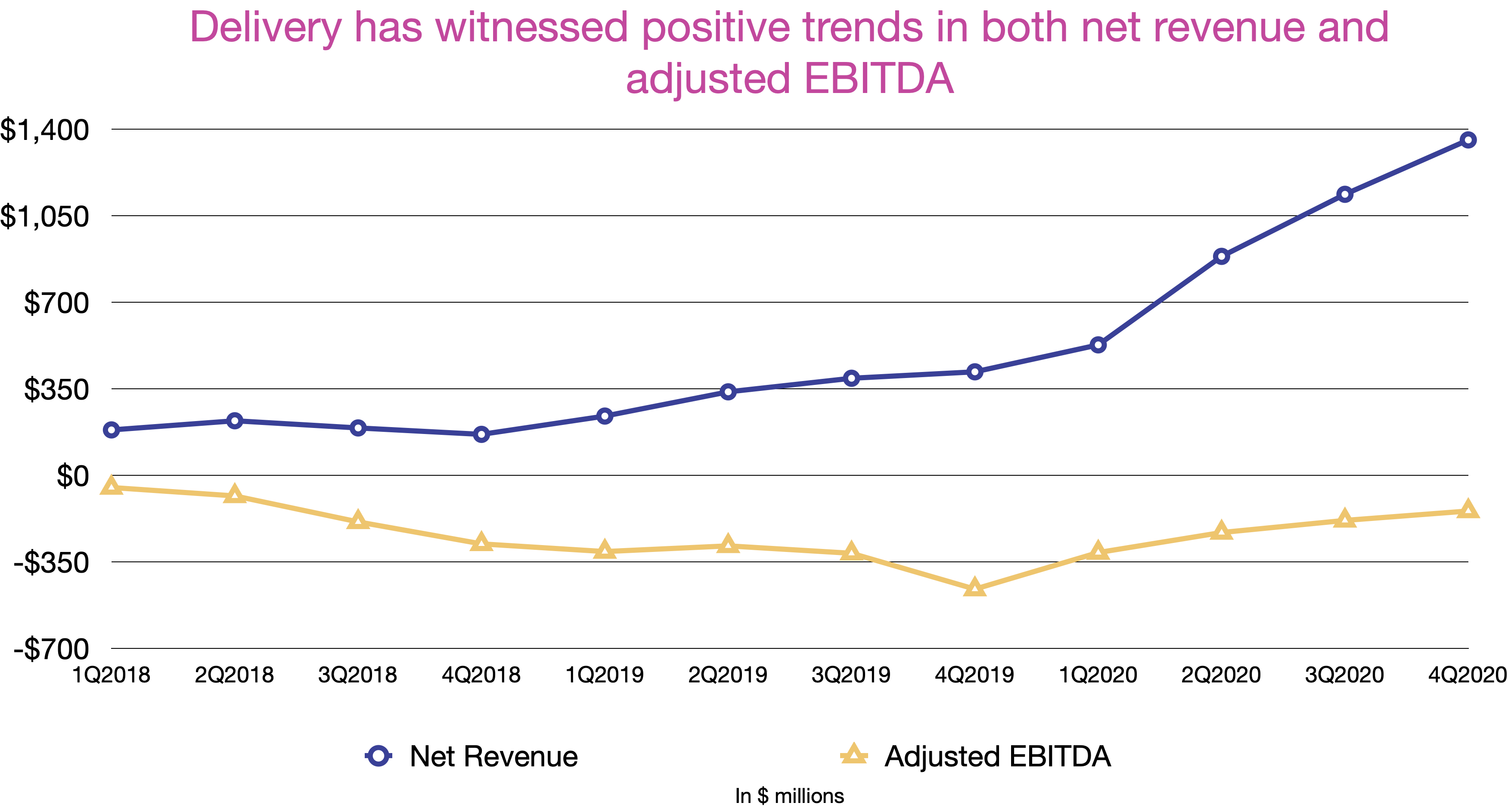

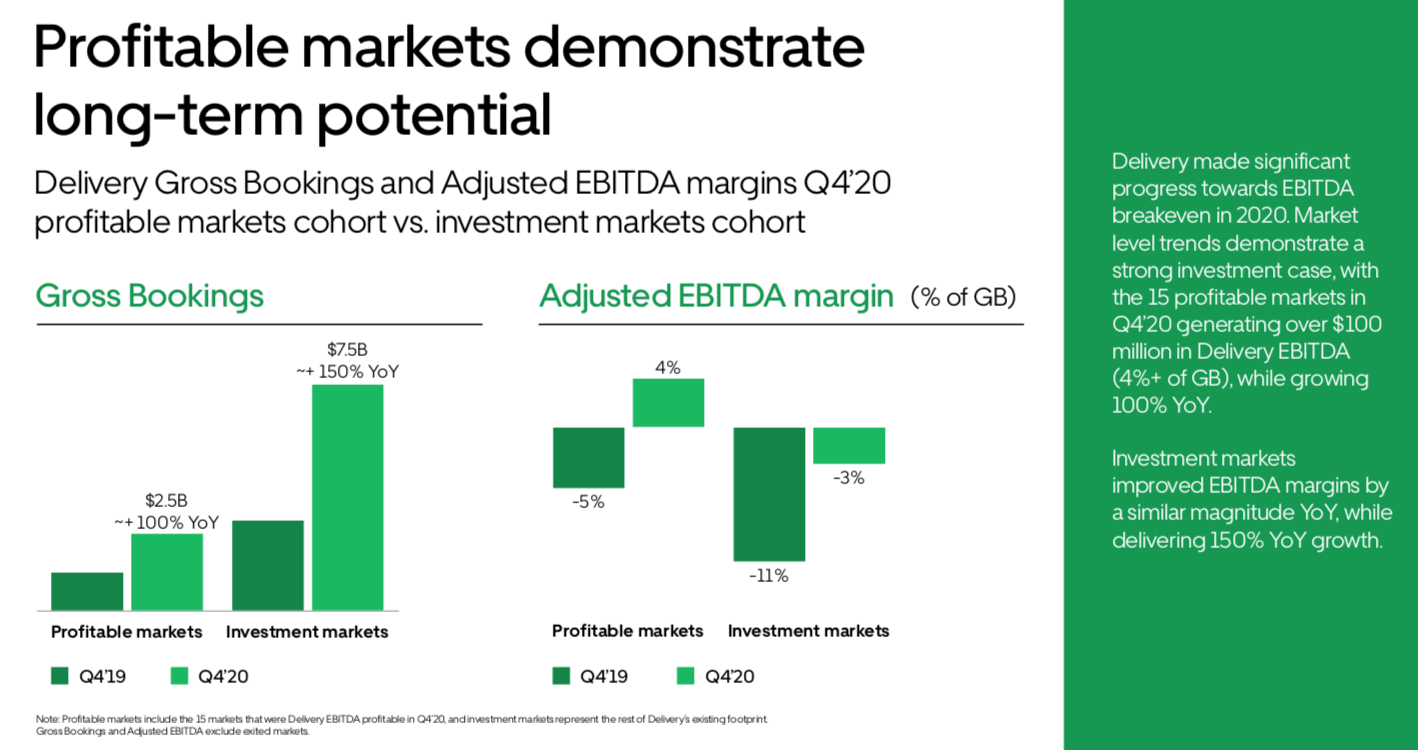

Mobility used to be a much bigger business than Delivery, but Covid-19 turned things upside down. Delivery has grown substantially in the past year and been the savior of a business whose major cash cow was badly damaged by the pandemic. Delivery’s gross bookings in Q4 2020 exceeded $10 billion, compared to $6.8 billion in gross bookings for Mobility. If we look at the rolling 4-quarter average gross bookings, Delivery surpassed Mobility in Q4 2020, but of course, it’s likely that once we get back to normal, Mobility will regain its crown. Delivery has seen its take-rate grow steadily since Q4 2018 to reach 13.7% in Q4 2020 and is now not so far off the long-term target of 15%. Furthermore, while Mobility has been profitable, Delivery hasn’t. The good news for Uber is that it is achieving increasingly positive operating leverage in Delivery. While its Delivery net revenue has grown fast, its adjusted EBITDA has also gone in the right direction. If Uber can make true of its plan to be adjusted EBITDA positive in 2021, it likely means that we’ll see a profitable Delivery in 2021 as well; which already happened in 15 markets.

Uber’s main four stakeholders are end users, partners (whether they are mom-pop restaurants, well-known chains or grocery stores), drivers/deliver people and lawmakers. Lawmakers have an influential role in Uber’s future as the laws they make can have major impact on Uber’s top and bottom line. But for this section, let’s just talk about the other three.

The way I think about Uber as a business is that it connects end users, partners and drivers altogether. The more end users Uber can present to its partners, the more partners it is likely going to sign. In turn, that means Uber’s end users can have a bigger selection at their finger tips, raising Uber’s value proposition. On the other hand, a bigger end-user pool helps the company sign up drivers. Drivers have limited resources in their vehicles and time, as even the most dedicated drivers can’t drive for more than 24 hours a day. Nobody wants to drive around needlessly all day without getting paid while having to pay for vehicle expenses and gas. As a result, the more business opportunity Uber can bring to drivers, helping them better leverage their time and resources, the more drivers will sign up. When it comes to making more trips and money, do drivers care if it’s a parcel or a person that needs transporting? In return, more drivers lead to faster “delivery” (transportation of an object from one place to another), whether it’s the delivery of a person or an item. Faster delivery means that customers will be happy and stick around using Uber more. In short, it’s an intricate multi-party relationship that Uber has to manage. It’s not easy or cheap to begin with, but once Uber sets these flywheels into motion, they can gain lasting competitive advantages. For example, at the end of Q4 2020, Uber recorded 675,000 active merchants, up from 450,000 in Jan 2020. It’s unclear whether this 675,000 figure includes the 100,000 partnered merchants that Uber inherits from its acquisition of Postmates. Meanwhile, Grocery Gross Booking exceeded $1.5 billion annualized run-rate. These numbers indicate a growing ecosystem.

So how does Uber make money? In short, from all three stakeholders: customers, partners and drivers. Here is what Uber said in its latest SEC filing back in Q3 2020:

Mobility Revenue

We derive revenue primarily from fees paid by Mobility Drivers for the use of our platform(s) and related service to facilitate and complete Mobility services and, in certain markets, revenue from fees paid by end-users for connection services obtained via the platform. Mobility revenue also includes immaterial revenue streams such as our Uber for Business (“U4B”), financial partnerships products and Vehicle Solutions. Vehicle Solutions revenue is accounted for as an operating lease as defined under ASC 842.

Delivery Revenue

We derive revenue for Delivery from Merchants’ and Delivery People’s use of the Delivery platform and related service to facilitate and complete Delivery transactions. Additionally, in certain markets where we are responsible for delivery services, delivery fees charged to end-users are also included in revenue, while payments to Delivery People in exchange for delivery services are recognized in cost of revenue.

Source: Uber

On the Mobility side, Uber takes a cut from bookings (around 20-25%) paid by customers before transferring the rest to drivers. On the Delivery side, it makes money from everybody involved in an order. After paying a one-time set-up fee of $350, restaurants have to pay Uber 15% or 30% commission on every order, depending on what delivery method they choose. If they user Uber for the delivery, the commission rate is 30%. If restaurants use other delivery methods, it falls to 15%. With regard to drivers, drivers receive a fixed fee for picking up and dropping off items and a variable rate based on the distance they cover. From the end-user perspectives, there are more than one fee involved in every order. According to Uber:

– Delivery Fee: Delivery fees vary for each restaurant based on your location and availability of nearby delivery people. You’ll always know the delivery fee before selecting a restaurant.

-Service Fee: Service fees equal 15% of your order’s subtotal, subject to a minimum of $2. The fee does not apply to restaurants that deliver their own orders.

– Small order fee: Small order fees apply when an order’s subtotal is less than a certain amount. This varies by city, but is either $2 for subtotals less than $10 or $3 for subtotals less than $15. You can remove the fee by adding more items.

– Delivery adjustment fee: A delivery adjustment fee refers to an update you made after placing your order- like changing your address. It helps to pay your delivery person for extra time and effort.

Source: Uber

In short, if there is no delivery adjustment and orders are above the small order threshold, Uber typically can take at least 15% of the order from merchants and delivery fees from end users which Uber doesn’t share with drivers. If merchants don’t have in-house delivery workforce, Uber can earn more from both ends of the transaction with 30% coming from the merchants and service & delivery fees coming from end users. Mom-and-Pop merchants whose limited resources don’t allow them to retain on the books a delivery team represent a more lucrative segment to Uber. During the pandemic when delivery is a trend, these merchants may not have a choice, but to partner with the likes of Uber. The question is: what will happen when seated dining resumes? How will that affect Uber’s Delivery business?

In Q4 2020, Uber closed the acquisition of Postmates. Similar to Uber, Postmates charges merchants at least 15% on every order and its fee structure imposed on end users is, in principles, similar to Uber’s. What Postmates offers to Uber is less competition, access to Postmates’ footprint and the deliver-as-a-service capability. Instead of building the infrastructure and signing merchants from scratch, Uber can quickly snap up what Postmates has and build from there.

With Postmates, we bolstered our local commerce capability through their delivery-as-a-service offering that already counts Walmart, Apple and 7-Eleven as customers. In December, delivery-as-a-service, represented 18% of Postmates orders, and we intend to scale this out further along with our Uber Direct product.

Source: Uber’s Q4 2020 Earnings Call – From Koyfin

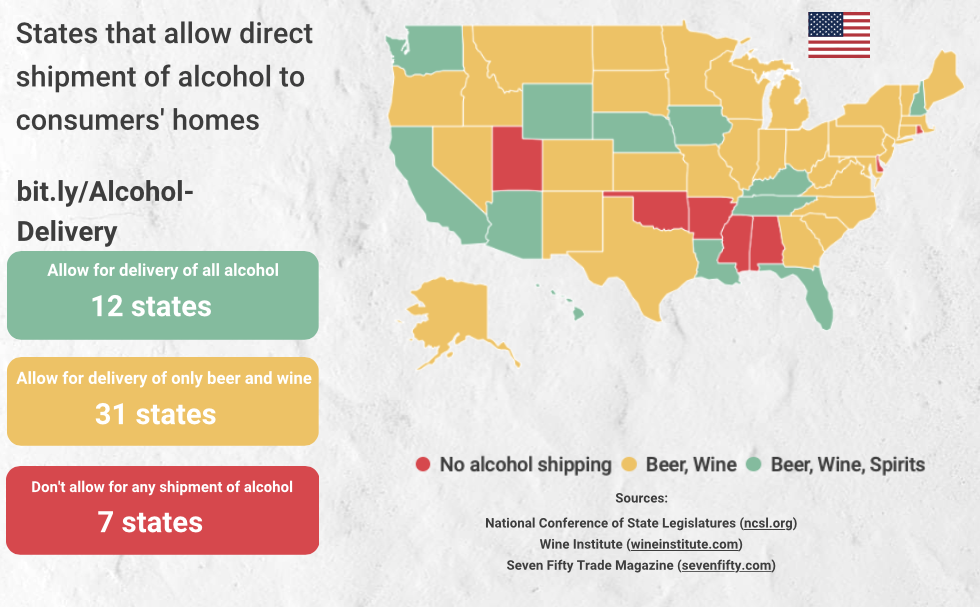

In Feb 2021, Uber announced its acquisition of Drizly for $1.1 billion in stock and cash. I think it’s a smart acquisition on Uber’s part. Let’s look at it together. Drizly was founded in 2012 when their founders realized the complexity of alcohol distribution in the US could present a golden business opportunity. Liquor distribution in the US mainly follows the three tier system and can be pretty fragmented and complex. In short, liquor producers or importers can only sell to wholesale distributors which, in turn, can only sell to retailers who, with a liquor license, can sell to end users. There are exceptions across the states and can vary even from county to county. Added to the complexity are the restrictions on alcohol delivery. Some states allow delivery of liquor, beer and wine. Others restrict delivery to only beer and/or wine while a few prohibit delivery of alcohol altogether.

How does Drizly make money? Drizly works with local retailers that wish to sell alcohol to consumers and charges these retailers a fixed monthly fee for the privilege. In return, retailers receive two things: marketing and an age-verification technology. Local retailers, especially smaller ones, don’t have the coins to spend on marketing nor do they have the ability to verify the legal age of buyers during the transaction. Hence, these retailers could face a huge legal liability if things went wrong and they were caught selling alcohol to whomever they shouldn’t have. Drizly offers retailers its proprietary technology to verify IDs to ensure buyers are who they said they are. Furthermore, Drizly charges consumers roughly $7 on each transaction, including a Delivery Fee of around $5 and $1.99 Service Fee. It’s important to note that retailers are responsible for the delivery task. What it means is that Drizly never takes possession of the alcohol during the transactions and therefore, doesn’t have to get a permit. By avoiding the expensive delivery business, Drizly can focus on what it does best: navigating the complex legalities, connecting merchants and consumers and marketing. On the merchant side, they are free to set up their own prices on Drizly marketplace and do not have to relinquish a cut of the sales to the company. The more alcohol Drizly can help them sell, the cheaper that monthly fixed fee becomes and the more likely retailers can negotiate a better term with distributors.

First of all, by acquiring Drizly, Uber gains access to a profitable and growing business. According to Uber, Drizly is growing at 300% YoY and already profitable on an EBITDA basis. I suspect that once we get out of this pandemic, consumers will be more aware of the prospect of alcohol delivery. Hence, Drizly will likely continue to see growth in the future, albeit perhaps not on the level that it saw in 2020. Furthermore, Drizly is a boon to Uber’s target of becoming profitable in 2021. Not only is the acquired profitable itself, but Drizly’s monthly revenue from retailers presents a much higher gross margin than Uber’s main businesses.

Second, Uber acquires a team that knows how to navigate the legal challenges in the alcohol market and an ID verification technology. Uber is well-versed in dealing with local authorities itself, but transportation is a different beast from alcohol delivery. With Drizly, Uber won’t have to start from scratch and will be able to stimulate Drizly’s growth with its much more sizable pocket.

Third, snapping up a market leader like Drizly prevents it from falling into the hands of Uber’s competitors. It’s a pre-emptive strike. Once the integration of Drizly into Uber’s platform is completed, Uber users can order the transportation of themselves (Mobility), food, groceries, parcels and alcohol all under one app. Uber’s competitors can match its offerings to some extent, but none can offer the same breadth of services like Uber, now that it adds alcohol delivery to the mix. To be able to do what Drizly does is not an easy feat, but to Uber, it’s adding to their competitive advantages.

Fourth, Uber has an advertising business that Deutsche Bank estimates to earn $1 billion in 2024. With the integration of Drizly, Uber adds to the potential clientele of advertisers and more data generated by Drizly’s marketplace.

In short, this is a great marriage between Drizly and Uber. Uber offers the smaller app its experience in building a marketplace, more financial resources, a much bigger brand name and especially marketing reach which is important to Drizly’s merchants. On the other hand, Drizly gives Uber a growing & profitable business, as well as access to a highly regulated business that is challenging to replicate.

Uber’s ambition to become a Super App has been obvious for a while. What should be encouraging news to investors is that it restructures itself to be more focused, exiting cash-bleeding businesses and unprofitable markets, and is willing to invest in its vision with the acquisition of Postmates & Drizly serving as proof. Of course, nobody can say with 100% certainty that these acquisitions will work out in the future, but in theory, I personally think that they make sense and are important pieces of a growing jigsaw.

Disclosure: I have a position on Uber.

Leave a comment