Uber lost $2.6 billion in the last 90 days!

However, that headline-grabbing figure doesn’t fully tell the whole picture. The fact that Uber stocks went up by more than 10% after hours indicates investors were pleased with what they saw and heard from management. There are reasons to that.

Total Gross Bookings (GB) grew by 33% amidst a challenging environment when inflation was the highest in decades. Revenue went up by 105%, although that included contribution from the acquisition of Transplace. Without the acquisition, my estimate is that Revenue would still be up by at least 30-40%. The number of monthly active platform users hit an all-time high record of 122 million while the number of trips increased by 24% to 1.87 billion, just a tad shy of the all-time record of 1.9 billion set in Q4 FY2019, right before Covid.

More importantly, Uber became a free cash flow generator for the first time in history. All three main businesses, including Mobility, Delivery and Freight, were all profitable on an adjusted-EBITDA basis. I understand that some folks have a bone to pick with the adjusted-EBITDA numbers, but Free Cash Flow doesn’t lie and it indicates Uber is on the right track. The giant net loss quoted above included $1.7 billion of unrealized losses related to Uber investments in Zomato, Aurora and Grab, as well as $470 million in stock-based compensation expense.

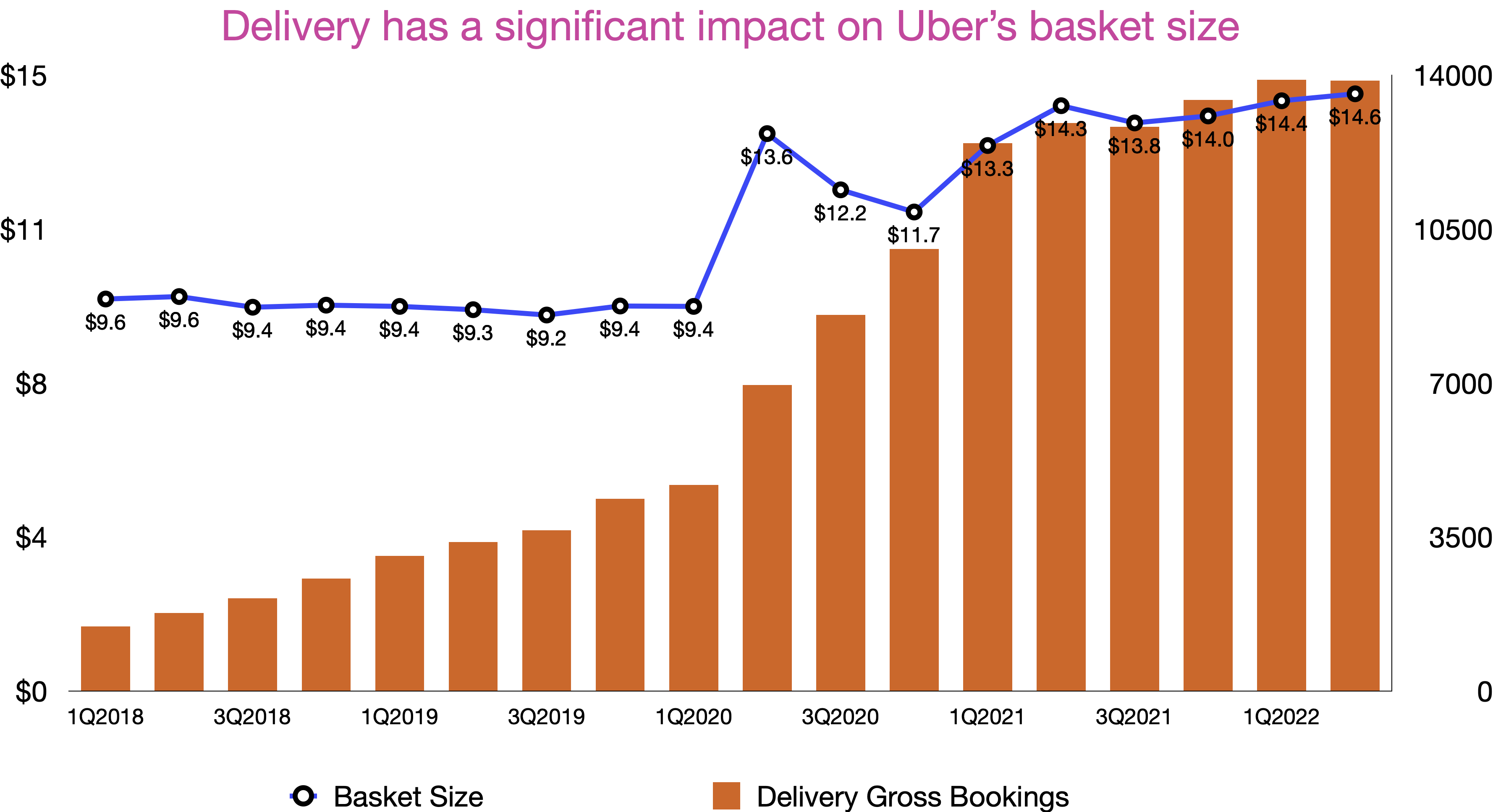

Back in my review of Uber Q3 FY2021 earnings, I wrote that Covid created a golden opportunity to transform itself. The latest results were further proof of that. Before Covid, Uber was all about Mobility, both in terms of gross bookings and revenue. The pandemic hit Mobility hard, but gave Delivery a great momentum that has not been relinquished since. In the last quarter, both segments notched the second-highest gross bookings in history in Q2 FY2022 while each recorded the highest revenue ever, albeit with some benefits from the model changes in some markets. Without Covid, I doubt that Uber could turbocharge its Delivery business that quickly. Now, instead of relying on Mobility, Uber has two weapons that complement each other well.

In A look at Uber after it acquired Postmates and Drizly, I wrote:

The way I think about Uber as a business is that it connects end users, partners and drivers altogether. The more end users Uber can present to its partners, the more partners it is likely going to sign. In turn, that means Uber’s end users can have a bigger selection at their finger tips, raising Uber’s value proposition. On the other hand, a bigger end-user pool helps the company sign up drivers. Drivers have limited resources in their vehicles and time, as even the most dedicated drivers can’t drive for more than 24 hours a day. Nobody wants to drive around needlessly all day without getting paid while having to pay for vehicle expenses and gas. As a result, the more business opportunity Uber can bring to drivers, helping them better leverage their time and resources, the more drivers will sign up.

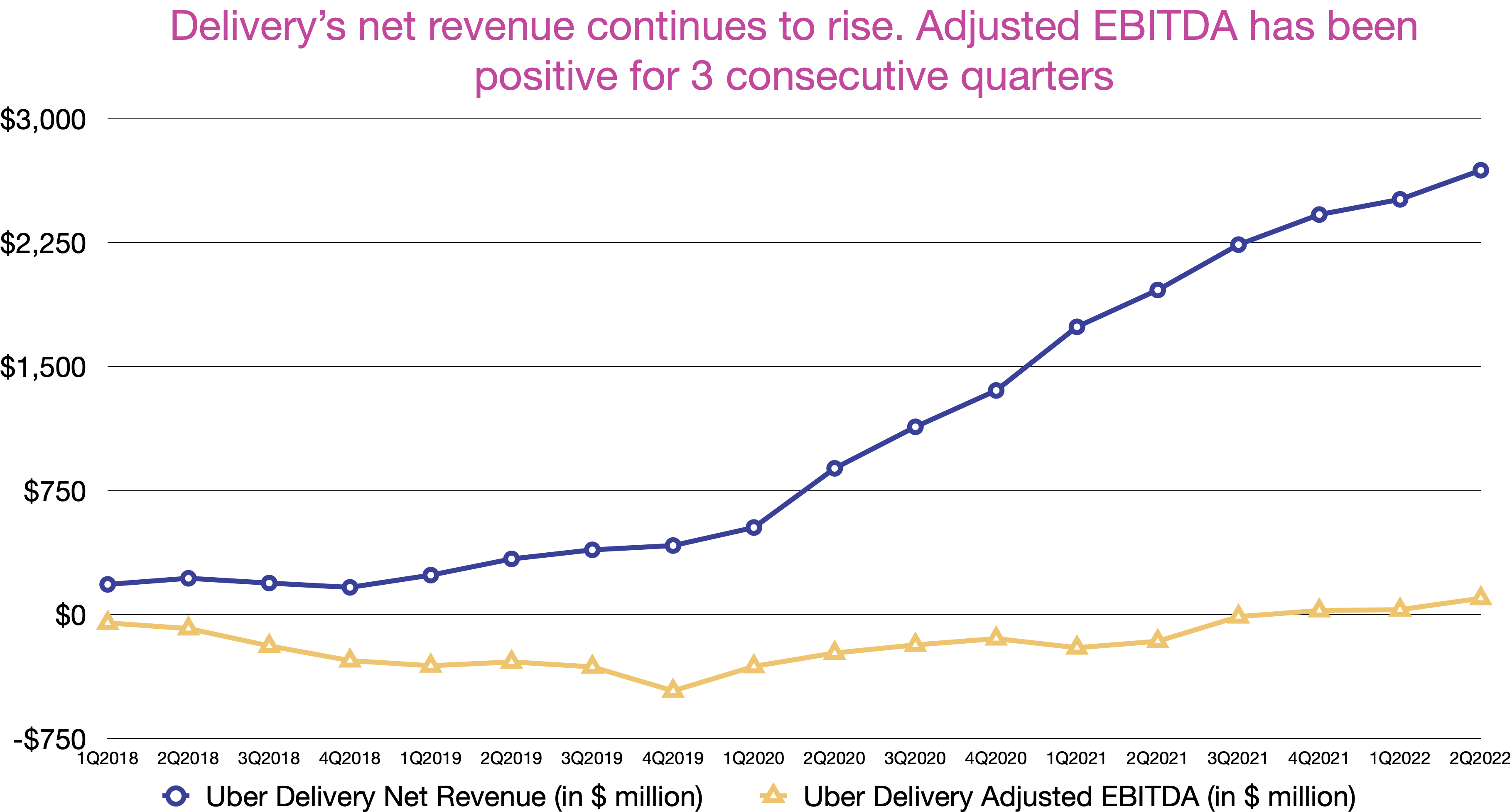

The rise of Delivery does wonders for Uber as it can bring more businesses to drivers. At times, when there is no rider to transport, couriers can deliver food or other items to better utilize the one resource that we can’t get back: time! Now that consumers are back on the road to office and travel, drivers have more opportunity to earn. On the call, the executives bragged that drivers in the US earned $30 per hour on average. That’s pretty competitive. Thanks to its scale, Uber believes it is best positioned to attract and retain drivers. The company has consistently talked about being more efficient with their operations and relying less on incentives. Such self-sustained growth is reflected by the fact that Delivery has had positive adjusted EBITDA for three quarters in a row.

Uber is a multi-sided network, dealing with consumers, drivers and merchants. They co-exist together and each cannot without the other two. Retaining drivers is crucial to retaining merchants and riders. In addition to the $30+ per hour income, Uber recently introduced some new features to support drivers. Soon, for the first time ever, drivers will be able to see in advance where the trip will end and how much they will earn for that trip. Drivers can compare multiple trips at once and decide what works best for them. Then, Uber will offer drivers a chance to earn 2-6% cash back at gas stations with Uber Pro Card. Gas is arguably one of the biggest expenses for drivers. The cash back is a nice gesture that will go a long way to retain this important class of stakeholders.

When delivery companies such as Getir or GoPuff are forced to shrink operations, the scale that Uber is operating on provides a great deal of advantages. If they can maintain that scale, other competitors will find it highly challenging to take share from Uber without near-term damage to profitability. And in case you haven’t noticed, profitability and sustainable growth is the tune that Wall Street wants companies to sing, not growth at all cost.

Sustainable growth is one area where Uber has been much better since Dara became CEO. Back in 2020, in Uber’s latest chess moves, I wrote about the downside of Uber operating in many markets and praised Uber’s effort to withdraw from countries where it was not competitive. Yesterday, in a conversation with Bloomberg, Dara reiterated that stance by saying that Uber is still operating Mobility in India, but will shut down Delivery because they don’t think they can be the market leader. This type of strategic thinking and discipline can only benefit a company like Uber in the eyes of investors.

Moving forward, there are several levers that Uber can pull to stimulate growth and profitability. The first is Uber One. As of Q2 FY2022, Uber One has 10 million paid subscribers. That’s a respectable figure, compared to the 6 million reported in Q3 FY2021. However, considering that the company has 122 million monthly active platform customers, Uber One’s penetration is less than 10%. Once that number increases, it will boost the company’s top and bottom line meaningfully.

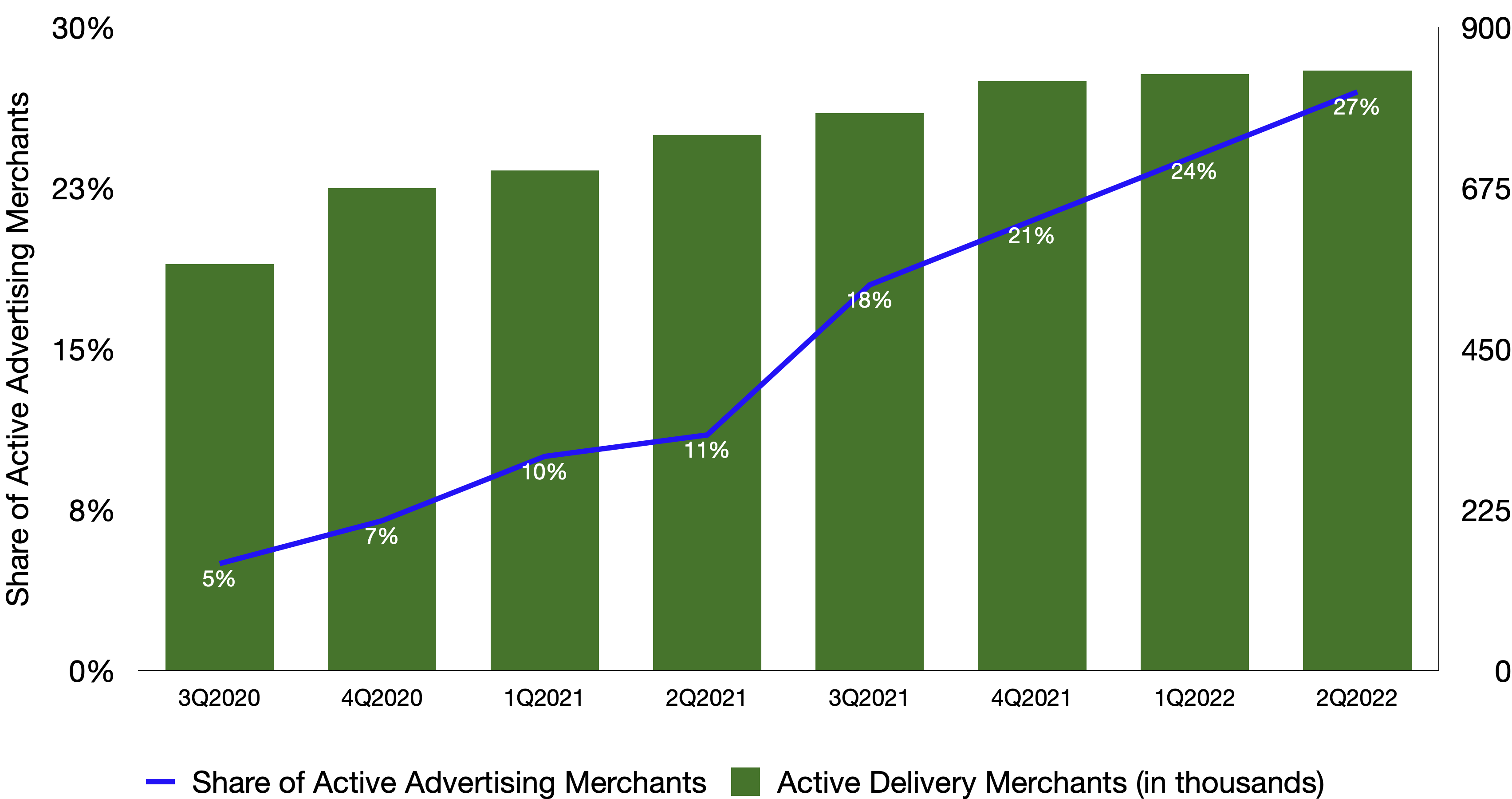

The second lever is advertising. Every company wants those high-margin ads dollars and Uber is no exception. Since its launch in Q3 2020, advertising on Uber has been used by 27% of all active Delivery merchants. Though Uber should be mindful of how a litany of ads can adversely affect customer experience, I don’t see any reason why the share of active advertising merchants cannot reach 40%.

Then, there are New Verticals in Delivery (groceries and non-food items) and Uber 4 Business. Combined, these two levers make up less than 10% of Uber’s Gross Bookings, indicating that there is room to grow in the future. The management team mentioned that they are still hiring for Uber 4 Business, a strong signal that they consider it important to the company’s future. New Verticals, like the partnership with Albertsons, plays a key role in increasing the utility of the Uber apps to consumers. Here is what Uber had to say:

As far as new verticals go, we’re quite satisfied in terms of the growth of that team. It’s at about a $4.5 billion run rate in terms of gross bookings. We are investing in this business. And despite investing in this business and it’s in the hundreds of millions of dollars, you can see the profitability that we’ve been able to drive with the delivery business overall. It’s really because of the scale and efficiency that we’re bringing to bear.

What we’re seeing with new verticals customers is that Uber Eats customers who also order from new verticals tend to stay with us, tend to have higher frequency. And it’s really a part of the power of the platform that we’re having. If you ride with us, if you eat with us, if you drink with us, if you order groceries with us, we just become an everyday part of your life. You top that off with the membership program. And we think we have a relationship with customers that really can’t be duplicated in industry on a global basis. That’s what the strategy is all about and we’re quite optimistic about our progress to-date

Source: Alphastreet

Overall, I am pleased with what Uber reported this quarter. Even though the stock is still down significantly, the business is in a stronger position now than it was before and during Covid. That is not to say that the company can afford to take its foot off the gas pedal and to lose discipline. What is gained today will be easily lost in 90 days. The macro economic situations remain chaotic and unpredictable. Consumers may have to cut back on non-essential spending and Uber, whether they like it or not, often falls into that category. Regulatory threats are always there. Formidable rivals such as DoorDash and Instacart are still competing hard. Hence, they need to stay focused and relentlessly execute. But with this result, I think at least they gained some investors’ confidence, including mine.

Leave a comment