Last Sunday, Square announced that it was going to acquire Afterpay, the Buy Now Pay Later provider from Australia, in a $29 billion all-stock deal. A lot has been said about this merger and the one bear case that I have seen quite often is that people questioned whether Square could actually build its own BNPL in-house and is wasting $29 billion on this deal. Below is how I think about it.

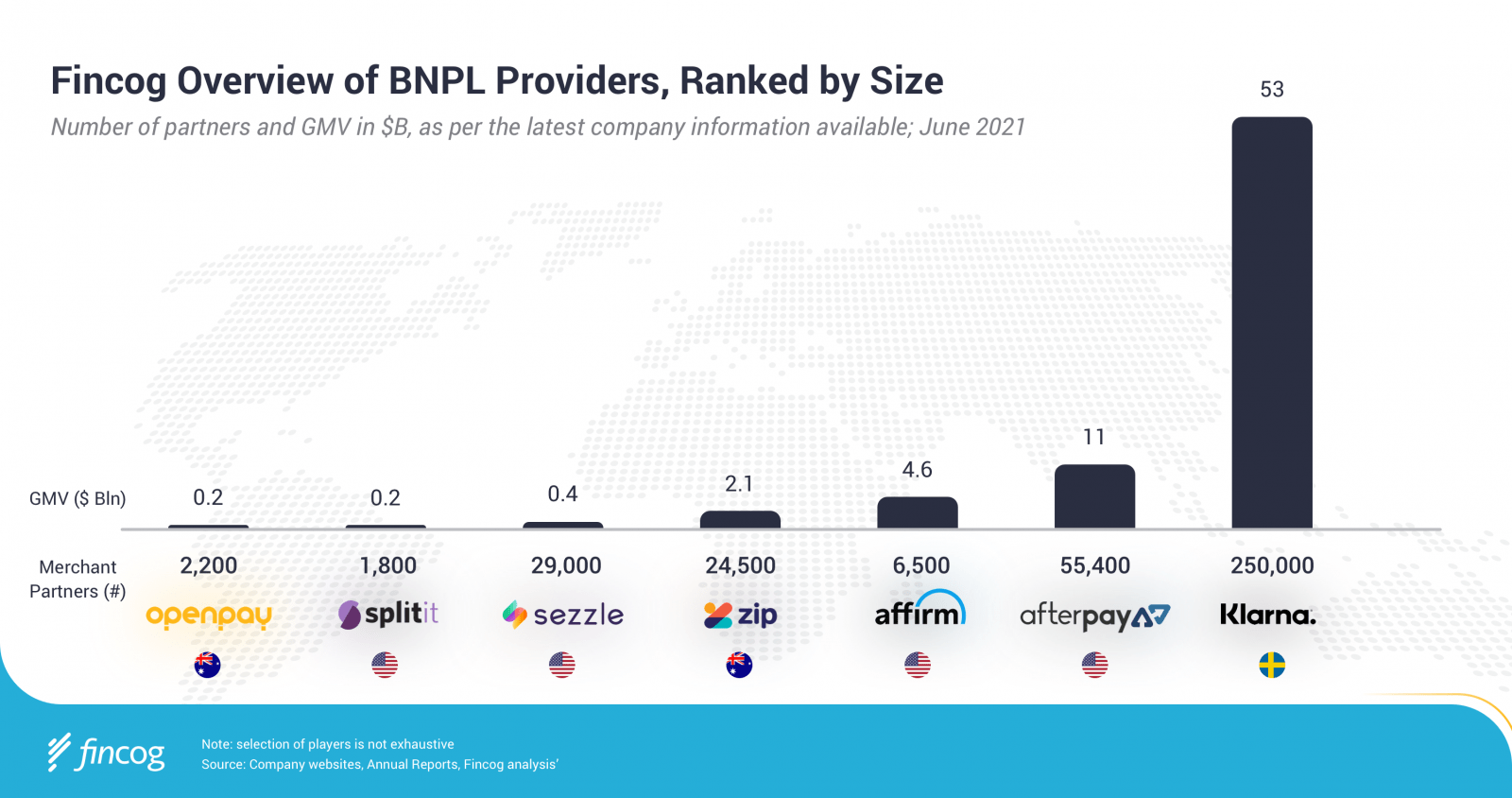

Before we go further, let’s take a minute to talk about these two companies in general. Afterpay was founded in Australia in 2014 by Nick Mornar and Anthony Eisen. The company allows shoppers to break purchases into four interest-free installments paid every two weeks. Afterpay charges merchants 3-4 times interchange rate in exchange for customer leads and the underwriting of the loans. Merchant revenue constitutes the majority of Afterpay revenue while late fees make up around 9% of the top line. Currently available in Australia, New Zealand, the U.S, the UK and Canada, Afterpay is launching services in a few European countries such as France, Italy and Spain.

Originally started as a payment company with a little credit card reader, Square has grown leaps and bounds over the years to become a publicly traded financial company with over 30 different services, a banking license and over $126 billion in market cap as of this writing. Square’s revenue comes from different sources. Bitcoin makes up more than 50% of Square’s revenue, even though the gross margin is only around 2%. The company sells POS hardware at a cost to merchants and charges them for used services. If merchants and customers want to receive funds instantly, they must pay Square a small fee. Square also offers merchants loans from which it earns interests. Last but not least, there is interchange revenue from millions of transactions processed through Cash App.

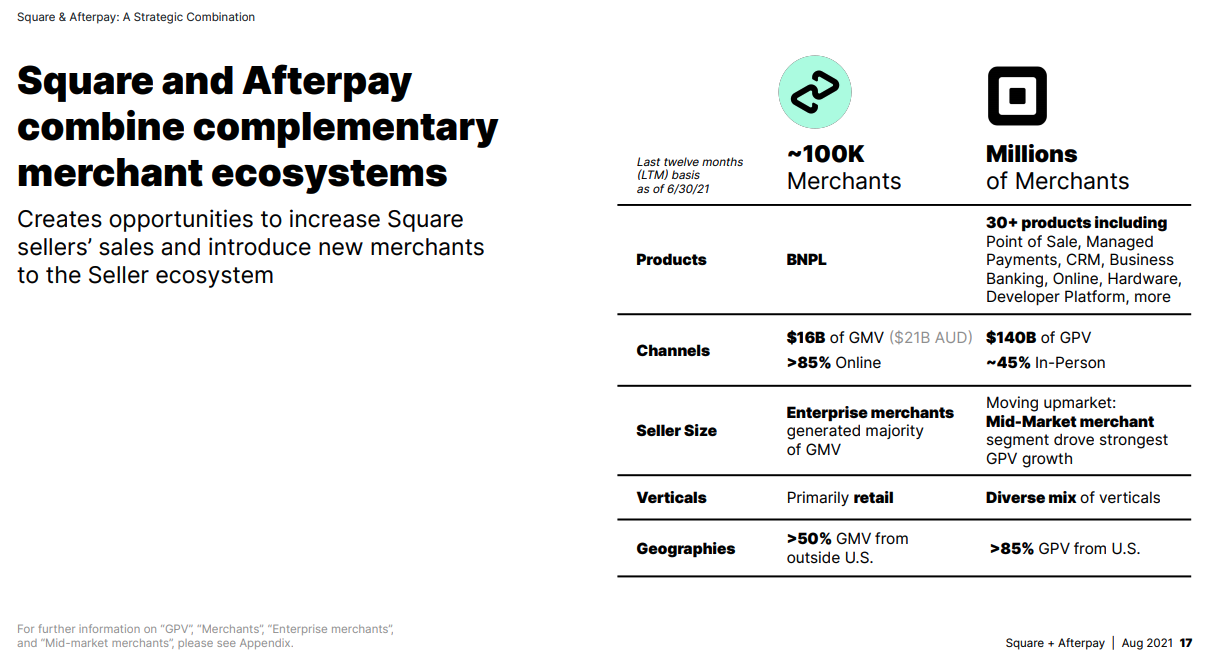

Square used to have a BNPL option which was discontinued due to the effects of Covid-19. Then why the sudden change of heart and why wouldn’t Square reactivate Square Installments instead of paying an enormous sum for Afterpay? First of all, it’s about international expansion. While Square is available in some overseas markets, 85% of its GMV is from the domestic front. Meanwhile, more than 50% of Afterpay’s GMV originates from non-US markets. Acquiring Afterpay gives Square quick access to those international markets and reduces reliance on its home market. Plus, it’s not really easy to build up a BNPL service from scratch. In addition to having to acquire merchants and users, to be a BNPL provider, one has to deal with a lot of regulation hurdles. These are the things that currently Afterpay does better than Square in non-US markets. Hence, this purchase will help Square bypass all the trouble and acquire these skills quickly.

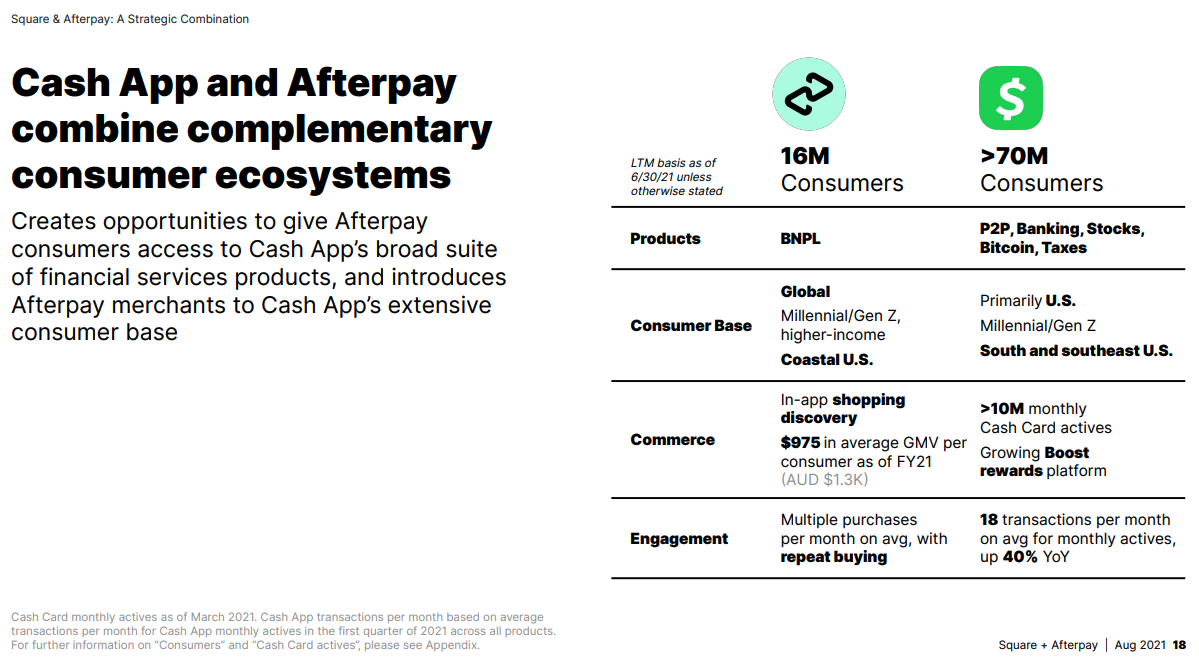

Second, customer acquisition. Afterpay’s main clientele includes Enterprise merchants wanting to leverage its popularity with consumers. On the other hand, while Square’s fastest growing segment is merchants whose GMV is higher than $500,000 a year, I doubt they are big enough that we can call them Enterprise. Hence, this acquisition enables the acquirer to move up the ladder and into a new market. The U.S is responsible for 62% and 43% of Afterpay’s active customers and GMV respectively. However, I’d say that in terms of reach to U.S consumers, Square is the far better company in this equation and has multiple touchpoints that it can use to acquire new users (Credit Karma tax, Cash App P2P, Bitcoin trading). Therefore, Square can definitely assist Afterpay in user acquisition. On the other hand, Afterpay gives Square access to the former’s high income customer base in coastal cities where Square isn’t as competitive as in the South.

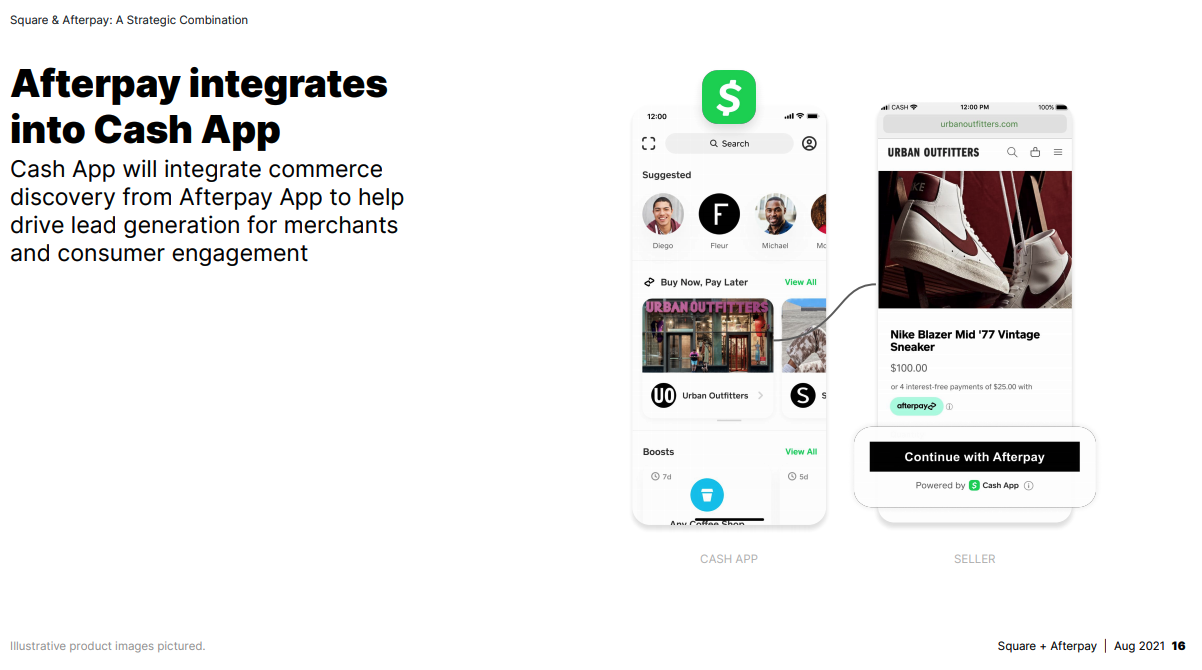

Third, merchant acquisition and retention. Merchants pay BNPL providers because of not only consumer preferences, but also the new business that these providers bring due to their marketing reach. For instance, Klarna reported 22 million customer lead referrals in the U.S December 2020 alone. This extra revenue is what merchants, especially smaller ones, crave and are willing to pay for. With the Discovery tool from Afterpay, Square can strengthen the relationship with merchants and keep them in the ecosystem. The more merchants they have, the more their Cash App can appeal to consumers and the healthier the whole ecosystem will be. As a result, the addition of the Discovery tool is strategically beneficial to Square.

Last but not least, this merger is about the competition. Square ‘s main challenger in the race to become the Super Financial App is PayPal. Formerly a P2P platform and a primary checkout option on eBay, PayPal has transformed itself into a financial service and a formidable eCommerce player. It provides both merchants and consumers with multiple different services to facilitate in-store and online transactions. With PayPal, shoppers can pay in stores and online with QR Code, tap-to-pay, mobile wallet, debit cards, credit cards and PayPal Credit. In the past few months, the company has ramped up significantly efforts in cryptocurrency trading, one of the selling points of Cash App. Additionally, PayPal recently launched Zettle, its card reader, in the US, a direct threat to Square’s bread and butter. PayPal’s own BNPL, PayPal in 4, has facilitated $3.5 billion in GMV in a few markets since its launch in August 2020, $1.5 of which came in the last 90 days alone. As mentioned above, Square no longer has an installment service.

Outside of the U.S, PayPal and Klarna, the global leader in BNPL, share a lot of market overlap with Square and Afterpay. This acquisition of Afterpay gives Square an instant counterweight to these competitors. Could Square build its own BNPL muscles? Absolutely, I have no doubt about it. But it will take a lot of time and resources for Square to play catch-up. By the time the company could form a respectable presence in the markets, PayPal and Klarna would already sign more merchants, gain more market share and establish a purchase habit as well as brand name with consumers. It would be incredibly tough to overcome these advantages. With Afterpay, Square won’t have to start from scratch and can compete right away with their rivals.

In summary, from my perspective, there are legitimate reasons why Square made such a big splash. Afterpay brings to the table what Square needs for its growth plan and more importantly, it does so instantly. Of course, M&A deals fail all the time. Synergies are often overstated. Cultural clashes tend to be overlooked. Execution doesn’t materialize as expected. Management teams butt heads. All kinds of trouble can happen to derail a partnership. This one isn’t immune to such risks. But I hope that one day we can look back at this deal as an important milestone and lever that propels Square to incredible heights.

Leave a comment