What happened?

Last week, PayPal reported its Q4 FY2021 results, causing the stock to reach by almost 25% and reach its 52-week low. Once a $360+ billion company at its peak valuation, PayPal is now worth $148 billion. There are a few contributing factors to this implosion.

The first is the disappointing guidance. A few months ago, the company set the revenue growth for 2022 at 18% which is now replaced by the 15-17% range. The guided Earnings Per Share is $4.67, well below the consensus of $5.21. For Q1 2022, revenue is expected to grow by 6%, significantly lower than the two-digit growth rate usually seen in every quarter since 2019. High inflation, the supply chain issues that have been felt across markets, increased tax rates and tough comparisons to last year’s results are to blame.

Net new active accounts are also a let-down. Total net adds in 2021 stood at 49 million, far lower than the 55 million target reaffirmed in November 2021. This year, PayPal expects to add 15-20 million new accounts. This conservative goal is lower than what PayPal managed in 2018 or 2019 before Covid-19 boosted their business and pulled forward a lot of net new accounts. The management gave two reasons for this muted outlook. First, 4.5 million accounts are found to be illegitimate. Even though the number is immaterial to the overall account base of more than 400 million, it affects the company’s estimate and thinking in terms of net new adds. The second and bigger reason is a new pivot in customer acquisition. Used to plow a lot of money in incentive-led marketing tactics, PayPal is going to abandon low-ROI efforts on low-value customers and instead prioritize high-ROI engagement campaigns which they say have better yields.

Because of the new pivot in customer acquisition, PayPal determined that the target of 750 million active accounts by 2025, which was only set last year on Investor Day, is no longer appropriate. The rumored acquisition of Pinterest a few months ago already called into question the growth outlook. This unexpectedly disappointing development aggravated investor doubt that the management team bit more than they could chew last year and sold investors on unrealistic targets. For me, it is the biggest shock from the earnings call. After Q3 FY2021, I was already concerned about PayPal’s ability to hit its long-term goal, but I, in no way, could expect that they gave up one year into the 5-year plan! Talk about disappointment!

Are the business’ fundamentals still healthy?

Investors are right to be downbeat on PayPal. The announcements on the earnings call gave nothing, but cause for doubt on the health of the business. Nonetheless, I don’t really think that all is lost. The outlook from here isn’t as rosy as we were told before, but one of the most iconic brands in the world can’t just crumble over night. Here are a few reasons why.

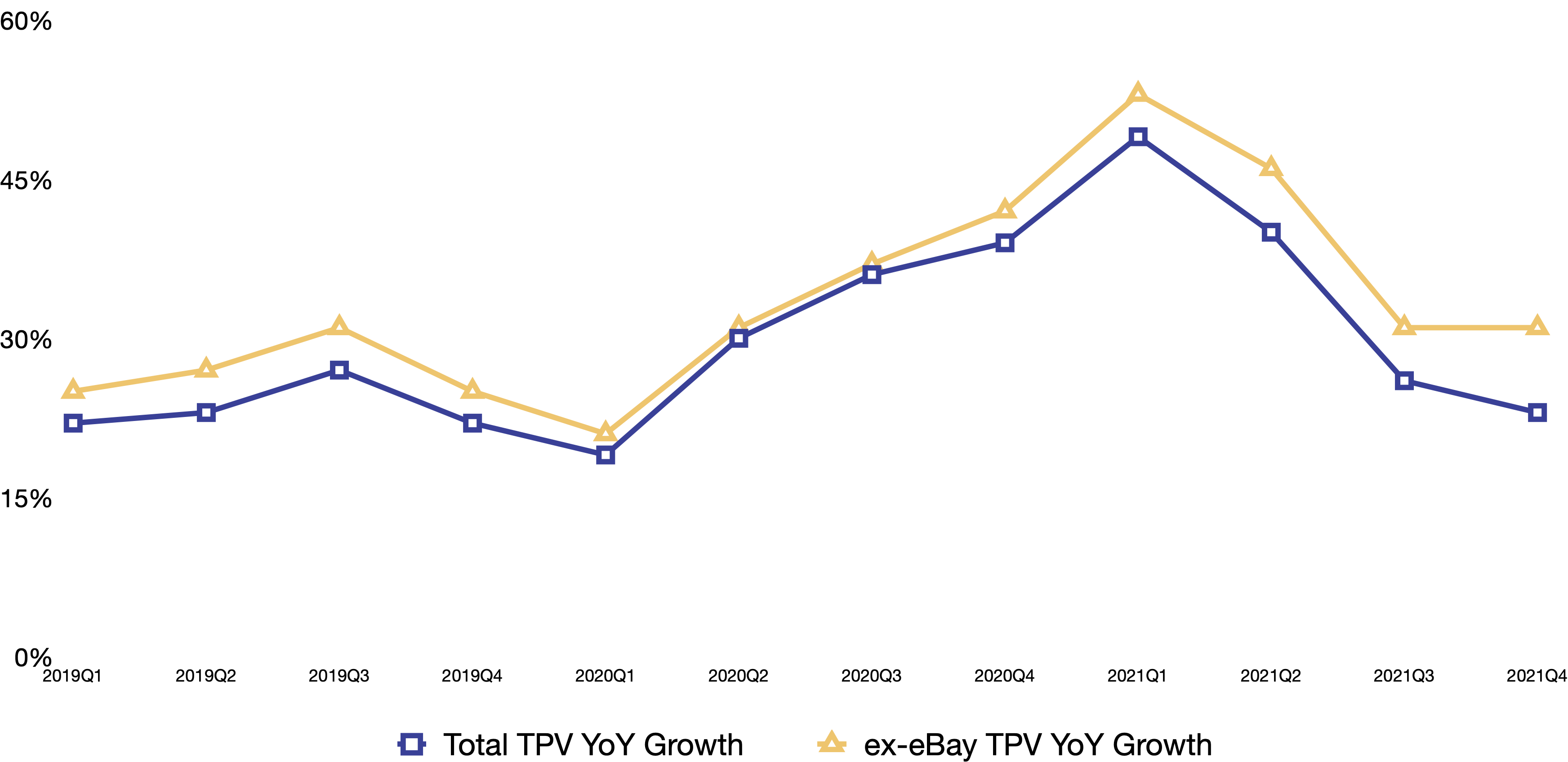

The divorce from eBay is strategically essential as it liberates PayPal from the exclusive partnership. EBay is now responsible for only 3% of PayPal’s total payment volume (TPV) and revenue, down from 8% of total TPV and 14% of revenue in the same quarter two years ago. Ex-eBay TPV growth has outpaced total TPV’s every quarter since Q1 2019. This, coupled with the fact that average transactions per active account continues to rise, signals that PayPal’s non-eBay services grew on merit and appeal to consumers.

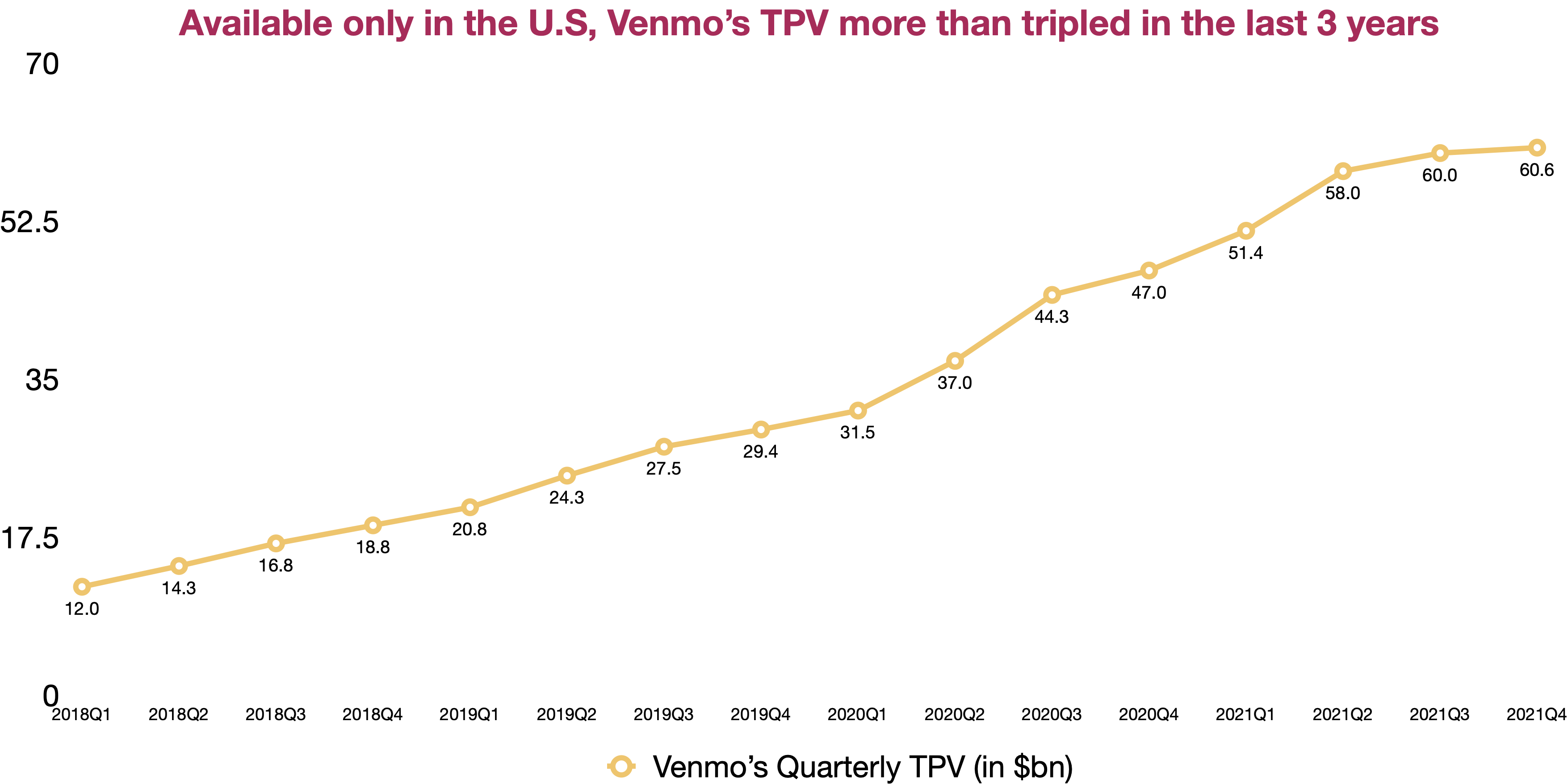

Venmo continues to impress with $60.5 billion in TPV and $250 million in revenue in Q4 FY2021. There are 83 million active users in the U.S alone, meaning that almost 1 out of 4 people in the country uses Venmo. The TPV and the popularity are likely to rise with new major partnerships such as the one with Amazon or DoorDash. However, since these partners may command a low take-rate, whether they will help with the monetization remains to be seen. That’s the overall concern with Venmo. Despite the apparent popularity and making up 17% of PayPal’s active account base, Venmo is only responsible for 3.6% of the company’s revenue. The likelihood of merging the two apps any time soon is low. The risk of damaging the Venmo “cult” and taking away its appeal by folding it into the parent app is too big, but at the same time, how would the company entice Venmo users to try out other services? Currently, Venmo is available only in the U.S. What about an international expansion? Investors definitely can use some more disclosures on both issues from the management team.

BNPL is another bright spot. Launched only in August 2020, Pay in 4 already reached $8 billion in total TPV, 12.2 million unique customers and 1.2 million participating merchants. Considering that the parent company has 383 million consumer accounts, 33 million active merchants and 200 markets, there is a lot of growth ahead. As customers who used BNPL delivered 2x average revenue per account, this service will be an important acquisition and engagement tool. Would that translate into money for PayPal? The jury is still out on this question. As there is no fee charged to consumers and no additional service fee to merchants, PayPal is hoping to generate revenue through additional services. This is one of the areas on which I wish to gain additional insights in the near future.

Ironically, I find the new pivot in customer acquisition positive to some extent. While I was disappointed by the abandonment of the 5-year target, I think or at least hope that this is the right move for the business. Let me explain why. I used to receive a lot of incentive-led marketing campaigns from PayPal such as a reward for downloading an app, a discount at a partner store or a chance to win a money pot. As a consumer, I liked these efforts. The investor in me, though, thought that these outreach efforts seemed like a desperate attempt to inflate active account numbers and keep the Street happy with the progress towards the magic 750 million number. But as the active consumer account base grows, you can’t buy cheap engagement forever. Soon, the cost of low ROI campaigns would catch up and it did for PayPal. Therefore, now that the target doesn’t float over their heads any more, the company can be smart about allocating valuable marketing dollars. The next few quarters and the new disclosures on ARPU will be critical in regaining investor trust.

Competition

Adding fuel to investor doubt is the fact that PayPal has fierce competition in the payment market. The silent killer Apple Pay provides a seamless checkout experience on millions of Apple devices and thousands of online stores. Block/Square is investing and pushing aggressively (such as the acquisition of Afterpay) to gain an upper hand over PayPal to become THE Super App for financial needs. Affirm is evolving from being a pure BNPL player, and adding new capabilities such as eCommerce button, savings and rewards. Additionally, there are Shop Pay and Facebook Pay, native checkout experiences on hugely popular platforms with thousands of merchants and consumers. Last but not least, the rise of real-time payments around the world and in the U.S will also be a threat. Given this elevated level of competition and the sudden change in long-term targets, it’s obvious that PayPal underestimates competitors and overplays their hands. From now on, it’s back to the basics which include constant innovation, addition of value-added services and a firm grip on its engaged and loyal customers.

In summary

The latest quarter is undoubtedly a disaster. There is no other way to describe it. Management overestimated their competitive advantages and consequently set unrealistic goals which led to misguided actions (the rumored acquisition of Pinterest). When such mistakes came into light, the punishment followed, in the form of billions of dollars in market capitalization. But the iconic and trusted brand is still there. PayPal still has incredible assets and millions of active accounts on its platform. The ingredients for redemption are ready. Now it’s up to management to bring about results and restore investor trust.

Leave a comment