Want to understand Affirm, what it does and how it makes money? Read on as I am discussing one of the most popular BNPL names below. My goal is 1/ to give you a better understanding of the company than a normal article on the news and 2/ not to overwhelm you with a 20-page essay with a lot of details. Ready? Let’s do it.

What is Affirm? What does it do?

Affirm was founded by Max Levchin, a co-founder of PayPal, in 2012 with the purpose of reinventing the payment experience for consumers and merchants. With Affirm, consumers can spread out a purchase over multiple payments over time without deferred interest, penalties or late fees. There are generally two types of transactions processed on Affirm platform: with or without interest. 0% APR transactions guarantee consumers a payment plan with no interest, fee or additional costs. Interest-bearing transactions carry an interest rate that never compounds. For instance, if a $100 purchase comes with an APR of 10%, $110 is the absolute maximum amount that a shopper will ever pay. The unpaid balance will not compound. All of the benefits give shoppers more purchase flexibility, especially those who are tight financially.

For merchants, Affirm helps increase sales through a bigger ticket size, more leads and more options at the checkout for consumers. When consumers can pay off a big purchase in installments, they are more incentivized to take on more expensive items. What merchants don’t want to sell their pricier products or services? In addition, as one of the most popular technology names out there, Affirm can bring hundreds of new leads – new businesses, to merchants. In exchange for all of these value propositions, Affirm charges participating merchants a fee on every transaction.

How does it originate loans?

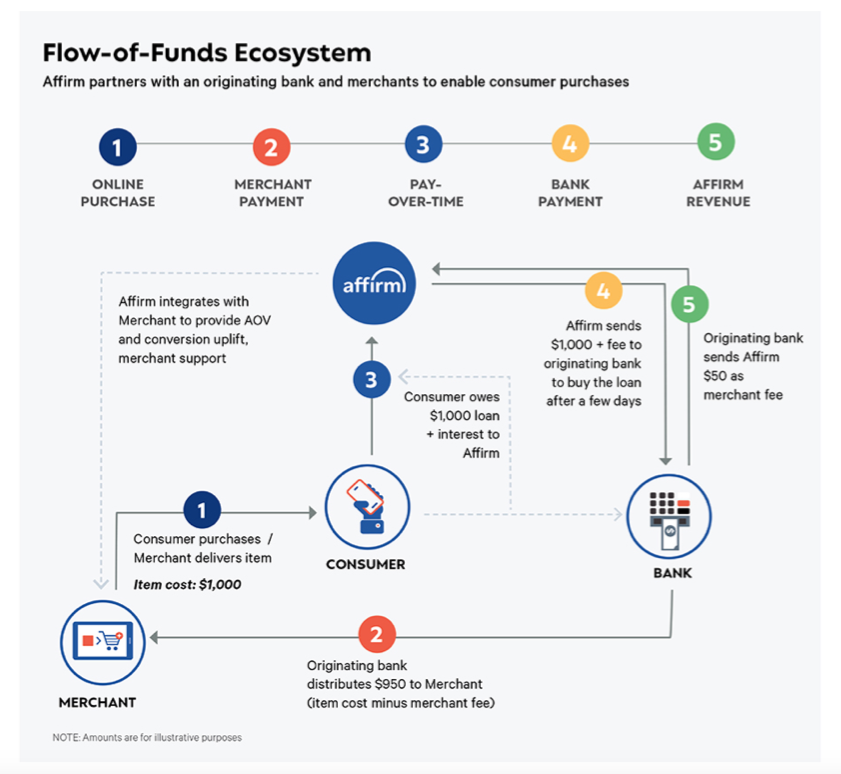

When Affirm authorizes a transaction on its platform to a shopper, it is essentially giving out an unsecured loan. Even though Affirm itself doesn’t have a banking license to do that, it works with Cross River Bank and Celtic Bank, which help the fintech firm originate loans and comply with regulations at state and federal levels. Affirm is obligated to purchase the loans processed on its platform and originated by the partner banks. Such an obligation is backed by a cash deposit that Affirm has at these banks. The purchase price of a loan is the combination of its outstanding principal balance, a small fee for the banks’ trouble and any incurred interest. As a result, Affirm incurs an expense for every 0% APR transaction because they have to purchase the loan at a value higher than the fair market value of the loan. This expense is called “Loss on loan purchase commitment”.

Because the banks originate the loans themselves, they have the ultimate power to either approve or decline such loans and Affirm needs to underwrite within the risk parameters that the banks set. You may ask why banks need Affirm in this whole process after all. The answer is that Affirm brings in the ability to sign up merchants, the marketing expertise to appeal to shoppers and the capability to use machine learning to process data that can help better underwrite loans.

How does Affirm make money?

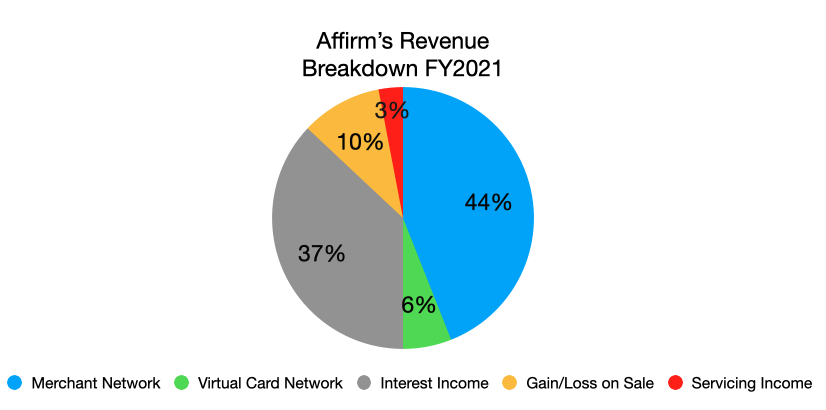

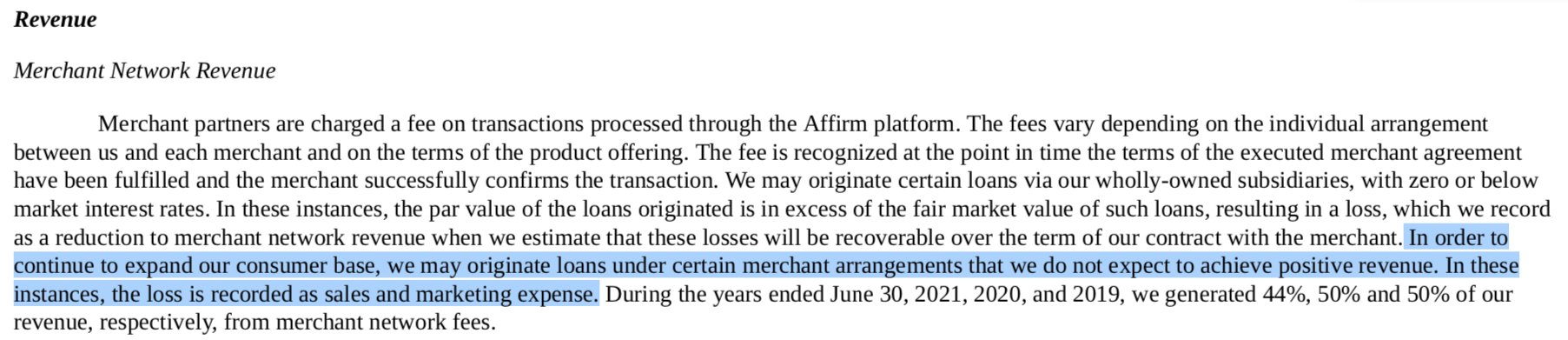

Affirm has multiple revenue streams. The first is Merchant Network Revenue, which consists of transaction-based fees. Every time Affirm processes a transaction on its platform, it takes a percentage cut from the purchase amount, coming out of the merchant’s pocket. The amount varies depending on a specific arrangement between Affirm and the merchant in question. Typically, Affirm earns larger Merchant Network fees on 0% APR transactions. Similarly, the firm earns a higher commission rate on higher value purchases. In some cases, in order to grow its user base by working with a giant partner, Affirm may not generate positive revenue and the loss is recorded as Sales and Marketing expense.

The second revenue stream is Virtual Card Network. This revenue stream essentially is comprised of interchange fees earned by Affirm for transactions on its platform. Apart from paying the Merchant Network above, merchants also have to pay another on every sale smaller fee called interchange. A portion of that fee, or I would say, the lion share of that fee will go to Affirm. Based on the aforementioned descriptions, it’s obvious that how much money Affirm can make in Network Revenue (Merchant Network + Virtual Card Network) in general hinges on how much transaction volume (GMV) it processes. Barring some caveats that I will explain later, GMV is a good indicator of Affirm’s health.

In addition to Network Revenue, Affirm also makes money from the interest on non-0% APR loans to consumers (Interest Income). These interest-bearing loans typically result in lower Merchant Network fees than 0% APR loans, but fill in the gap with interest. In Q1 FY2022 ending September 30, 2021, 57% of Affirm loans were bearing interest and the rest were interest-free. During the fiscal years 2019, 2020 and 2021, 45%, 37% and 37% of Affirm’s revenue came from this revenue stream.

The company can also leverage its outstanding loans for more income. It can sell part of its outstanding balance to any interested party and record Gain/loss on Sale. While keeping a balance on balance sheet can lead to more interest income, it comes with a charge-off (consumers don’t pay off) risk and additional expenses (cost of funds). By selling some of the balance, Affirm can recognize, usually, gain on sale and reduce its risk exposure. Moreover, loan owners can solicit Affirm’s expertise to manage the loans in exchange for a monthly fee or what the company calls: Service Inc

What are Affirm’s competitive advantages?

Affirm’s competitive advantages come down to two things: its two-sided network and underwriting capability. Let me expand on that.

While difficult to build at first, a two-sided network provides a real strong competitive advantage. More shoppers entice more merchants that make the whole ecosystem more appeal to new shoppers. To maintain and grow its two-sided network, Affirm needs not only consumers, but also merchants. So far, the company has done a good job at this by partnering with some of the biggest names in the U.S such as Target, Peloton, Shopify, Walmart and Amazon. By locking in popular retailers, Affirm becomes more popular among shoppers which, in turn, help it acquire more merchants and negotiate more favorable terms. By working with Shopify, Affirm can onboard a lot of merchants right away and appeal back to shoppers. I suspect that some of these partnerships (Walmart, Shopify and Amazon) come at a cost for Affirm as the company must make major concessions, but in the long run, it’s a smart move by its management. Who else can make the same claim that they are the BNPL provider for these brands?

The second advantage is its ability to use data analytics for underwriting. Underwriting unsecured loans is a tricky business. Quite often, the riskier customers are the more profitable as they pay interest income yet they can also default on the loans. The art of underwriting is to find a sweet spot between profitability and risk. If Affirm only had reliable borrowers, they could still make money with their business model. However, they would leave out folks who need POS-lending the most, you know, the folks with FICO less than 700 or bad credit history. This population is significant, but it can result in losses. This is a challenge for not only Affirm, but all the companies that are offering unsecured loans. With a lot of transaction data, Affirm can fine-tune their underwriting model to limit losses while expanding the customer universe.

It is an interesting and fairly complex business

It’s not straightforward to understand Affirm’s performance from one quarter to another. The first issue is the nature of the company’s partnership with strategic brands. The partnership with Peloton, while fruitful and successful in the beginning, gave the POS lending tech firm some headaches, such as its recall of products (it reduced the merchant network revenue by more than $5 million in FY2021), 0% APR loans that are more expensive to originate and the delay in loan recognition as well as revenue booking. In FY2021, Affirm facilitated $66.3 million more transaction volume than what was captured and reported by Peloton.

Even though GMV, at first glance, can be a good indicator of Affirm’s business health, how the company generates GMV affects its revenue streams heavily. A high concentration of low-value or interest-free transactions negatively affects the company’s top and bottom lines, as explained earlier, despite an excellent growth in merchant and shopper counts. Case in point, the number of active merchants increased from 29,000 in Q4 FY2021 (ending June 30) to 102,000 in Q1 FY2022 (ending September 30). while the number of active customers rose from 7.1 million to 8.7 million in the same period. However, revenue only increased by 3%, from $262 to $269 million. One of the main reasons is that the average order value decreased from $495 to $402 and the concentration of 0% APR loans went up from 38% to 43%. As the partnerships with Amazon, Walmart and Shopify ramp up, I expect the trend of a bigger ecosystem, lower AOV and modest increase in revenue will persist. But who knows? If Peloton roars back and brings more high-value loans or if Affirm signs a similar partner, the situation will certainly change. This makes it a bit tricky to analyze this business as it has more than meets the eyes.

Another factor is how much the company estimates its provision for credit losses. The fancy term essentially means how much of the loan is expected to be lost. This estimate depends on not only the concentration of 0% APR loans or new product lines with higher expected losses but also macro economics factors. At the beginning of the pandemic, Affirm expected higher losses, but the expectation subsided over time before it was normalized to the pre-pandemic level. Because we are not out of the woods yet with Covid-19 (thanks Omicron!), it’s not practical to have a consistent estimated provision for credit losses.

Lastly, and this one is more for the future: the regulatory risks. As of now, the BNPL field is largely unregulated, yet there are signs that it’s about to change. The Consumer Financial Protection Bureau already opened an inquiry into BNPL products and ordered information from the main players, including Affirm. Whether there would be new regulations in place, what such regulations and what the ramifications would be remain to be seen. Personally, I think that the worst that could happen is Affirm will have to deal with the same regulations as banks do. But the same would also go for other BNPL firms. As long as the fundamentals of the company are strong and not prone to collapsing under more scrutiny, Affirm should be fine.

In short, even though what Affirm does sounds simple on the surface, the inner workings behind the scenes and the numbers are not. I hope if you make it this far, you already have a better understanding of the company. Not too deep, but not too shallow either.

Disclaimer: I have Affirm stocks in my personal portfolio.

Leave a comment