Corporate & Commercial – Apple’s next growth opportunity

Apple has always been a household consumer brand. There are still areas that the company can explore in the consumer space to fuel growth such as the global availability of their services, next generation chips, the AR glass or the long waited yet mysterious Apple Car. I remain excited about Apple’s growth prospect as a consumer staple, but Apple may be more than that in the future. There are signs lately that Apple may make a push into the corporate segment. First, it launched Apple Business Essentials, a device management service for small businesses with fewer than 500 employees. The program is still in early days, but the company already said that thousands of small businesses already participated in the program. That’s Apple’s style: choose to come to the market when a service or product is ready and deploy consistent incrementalism over time. Remember how some ridiculed their introduction of Wearables, which is now their 3rd largest business? And if they manage to build that muscle and processes to deal with small businesses, there is no reason not to think that they can expand their market and go further upstream.

Then on the earnings call, Luca Maestri (Apple’s CFO) revealed this anecdote:

Shopify, for example, is upgrading its entire global workforce to M1-powered MacBook Pro and MacBook Air. By standardizing on M1 Max, Shopify continues its commitment to providing the best tools to help its employees work productively and securely from anywhere. And Deloitte Consulting is expanding the deployment of the Mac Employee Choice program, including offering the new M1 MacBook Pro to empower their professionals to choose devices that work best for them in delivering consulting services.

Source: fool.com

I feel that M1 is the last puzzle piece that Apple needed to start making moves in the corporate market. The chip makes Apple devices more powerful and efficient, exactly what the white-collar folks like myself want and opposite of what we are used to (like all those bulky and burning Dell computers). As employees like Apple’s products, companies are more incentivized to offer such products as perks to retain talent; which plays into Apple’s hands. In the past, whether Apple’s products were the clear winners might be up for debate, but the introduction of their in-house chip put the question to rest.

This week, Apple revealed that future iOS updates would let merchants accept transactions with just a tap on their iPhones. The value chain analysis or how exactly this would benefit Apple are still question marks. I suspect Apple will take a small cut on every transaction like they do with Apple Pay transactions. Also, if merchants rely on an iPhone as a card reader, Apple Business Essentials will suddenly become an appeal so that they can manage their devices properly. These are just two early signs of what Apple can put together for businesses. I am eager to learn what they have in store because I am almost confident that they have a roadmap in mind already.

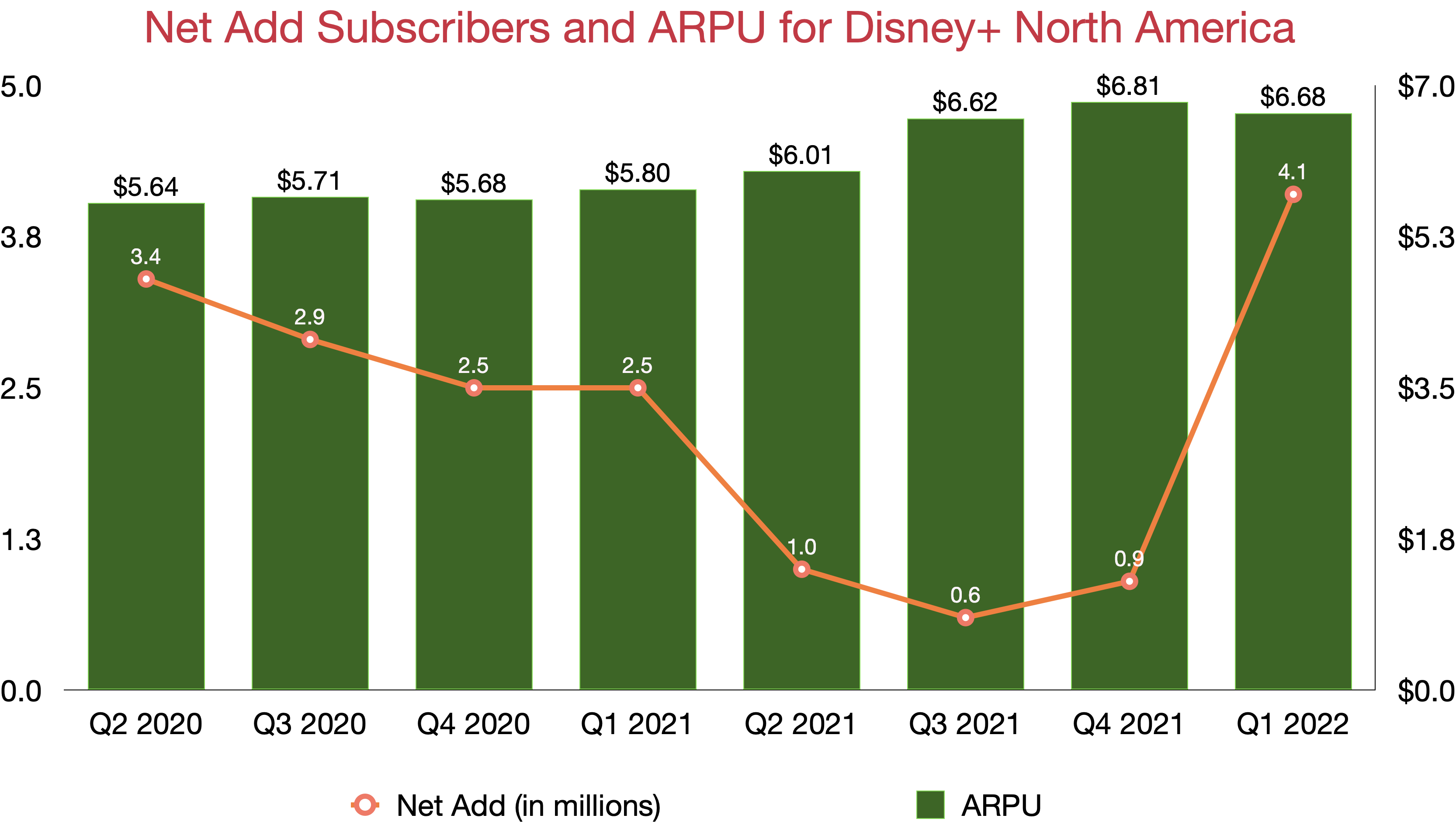

Disney+ and ESPN+ added more subscribers while raising prices. ESPN+ achieved its FY2024 target

The first quarter of FY2022 was a good one for Disney as the company continued to add more subscribers to its flagship streamer Disney+ outside of India and ESPN+ while increasing Average Revenue Per User (ARPU). The testament to the strength of a product or service lies in the ability to retain customers while raising prices. In that sense, Disney+ has so far defied critics and proven its mettle, showing that its streaming services are capable of challenging anyone else in this highly competitive market. The iconic company set the long term target of 230-260 million Disney+ subscribers by the end of FY2024. There are 8 more quarters to go. To attain that target, Disney needs to deliver a quarterly net add of at least 13 million subscribers. The company is on the right track to do so. In fact, the management said that even without the rights to Indian Premier League, the nation’s cricket competition that is arguably the biggest acquisition tool in the Indian market, it is still confident of meeting the FY2024 guide.

If you look at India, we’re certainly going to try to extend our rights on the IPL. But we’revery confident that even if we were not to go ahead and win that auction that we would still be able to achieve our 230 million to260 million. So it’s an important component for us around the world. Obviously, really important in India, but not critical to us achieving the 230 million to 260 million number that we’ve guided to.

Source: Walt Disney Q1 FY2022 Earnings Call

While Disney+ added more subscribers in the US and Canada than Netflix in the last few quarters, I don’t think that any comparison can be fair. The two streamers are operating at a different scale and life stages. Netflix is much more established and has a much bigger subscriber base. Hence, even though it added fewer customers, we shouldn’t draw any conclusion yet on either.

ESPN+ already achieved the FY2024 guide of 20-30 million subscribers. Its tally at the end of Q1 FY2022 is already 21.4 million. I am sure with an imminent international expansion and addition of rights to more sports, ESPN+ will attain the higher end of the guide range, if not exceed it.

Leave a comment