A couple of days ago, media outlets reported that PayPal was in talks to buy Pinterest for what could be a $40 billion deal. Per WSJ, “the talks are at an early stage and may not lead to a deal, some of the people cautioned.” If that went through, this acquisition would be PayPal’s biggest ever. But what does it mean for the iconic PayPal? Below are my thoughts.

Overview of PayPal & Pinterest

Before we go further, let’s recap quickly what PayPal and Pinterest do, how they make money and how their businesses are at the moment.

Formerly known as a check-out and Person-to-Person (P2P) function, PayPal has grown leaps and bounds in the last few years with grandiose ambition to be THE Super App for payments, consumer financial services and eCommerce. PayPal’s services now include almost all the things that consumers need such as debit card, credit card, BNPL, online & offline payment, P2P or remittance, just to name a few. On the merchant side, PayPal has added a plethora of Merchant Services and Marketing Tools in addition to its well-known payment processing. As a two-sided platform, PayPal needs to deliver value to consumers in as many ways as possible, including enhanced and seamless shopping at merchants, while appealing to merchants with tools to grow their business from both marketing and operations standpoints. Last month, the company took a big step towards their grand vision with the new PayPal mobile app.

There are several revenue streams for PayPal. First, a bulk of its revenue is from transaction processing. For each transaction that goes through PayPal, the company takes a cut. Hence, the bigger the volume, the bigger PayPal’s top and bottom lines. Second, PayPal also charges merchants on value-added services such as loans, inventory management or point of sale. Then, it also generates fees from other services such as remittance or credit card-related fees.

The transformation of the business is also evident in the numbers. PayPal’s number of active accounts grew from 244 to 403 million from 2018 to 2021, including 76 million Venmo accounts, while the merchant base expanded from 19 to 32 million. Its quarterly Transaction Volume exploded from $139 to $311 billion, more than $1.2 trillion in annualized volume. In Investor Day 2021, PayPal disclosed their target of $2.8 trillion in annual volume, 750 million active accounts and $50 billion in annual revenue at the end of FY2025. Quite an ambitious target.

The other side of the rumored deal, Pinterest, is a visual-centric social platform whose mission is to bring inspiration to people’s lives. “A photo is worth a thousand words” is essentially their value proposition. Every day, thousands of users & brands, called Pinners, post their ideas in the form of images or videos, called Pins, to the platform. Pins can be grouped together in personalized Boards that are accessible to others. Similar to other social media platforms, Pinterest deploys machine learning algorithm to personalize suggestions of new ideas to users, based on their previous activities. Meanwhile, advertisers can take advantage of the visual-centric experience, the global audience as well as data on consumer preferences calledTaste Graph on Pinterest to optimize advertising dollars and grow their business. Over the last couple of years, Pinterest has invested in features and partnerships to enable commerce on its properties. For instance, it launched Shop from Boards, Shop from Search and Shop from Pins in April 2020. The month after, it announced a partnership with Shopify that allows Shopify merchants to upload their catalogue to Pinterest seamlessly. Earlier this month, the company introduced a few new features to help merchants and creators showcase their hard work and generate more revenue/income.

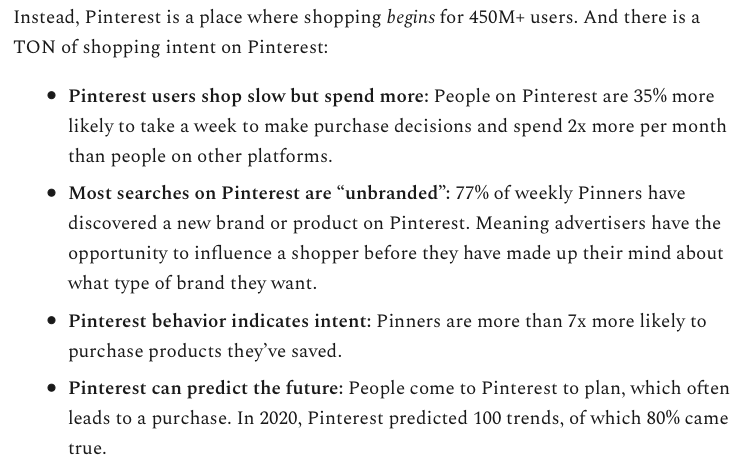

Pinners saved nearly 300 billion Pins across more than six billion boards. We call this body of data the Pinterest taste graph. Machine learning and computer vision help us find patterns in the data. We then understand each individual Pin’s relationship not just to the Pinner who saved it, but also to the ideas and aesthetics reflected by the names and content of the boards where it’s been pinned. We believe we can better predict what content will be helpful and relevant because Pinners tell us how they organize ideas. The Pinterest taste graph is the first-party data asset we use to power our visual recommendations.

Source: Pinterest

According to the latest filings, there are 454 million Monthly Active Users on the platform, 2/3 of which are female and 80% of which are outside the U.S. Even though it makes up only 20% of the MAU base, the U.S generates 78-80% of Pinterest’s revenue which came in at $485 million and $613 million in Q1 and Q2 2021 respectively. Pinterest was operationally unprofitable in the last three years, but has turned in some profit in the first 6 months of 2021. As a result, their free cash flow (FCF) has improved markedly. The company had negative FCF in 2018 and 2019 before turning in an FCF margin (FCF over revenue) of 0.73% in 2020. Their FCF margin for Q1 and Q2 2021 was 55% and 17% respectively. To put it in perspective, PayPal’s FCF margin in the last two quarters was 25% and 17% respectively.

Would the acquisition be about increasing active accounts for PayPal?

I doubt it is the primary reason why PayPal entertained this move. At the moment, these two are completely separate apps. Having Pinterest under PayPal would provide absolutely no incentive for Pinterest users to become PayPal users. Merchants that are already on Pinterest have no extra incentive to work with PayPal just because of this alleged acquisition. If PayPal decided to force the issue and fold the red app into the blue app, it would be catastrophic for both and a value killer for shareholders.

Would the acquisition be about improving free cash flow for PayPal and padding the sheets?

While Pinterest indeed posted higher FCF margin in the last two quarters than PayPal, I don’t think improving FCF margin is the driver of this move either. Competitively, PayPal is in a far stronger position than Pinterest. The former is one of the most iconic brands globally with millions of users and merchants in its network and in the leading position in its field whereas the latter is no match in terms of advertising capabilities with the likes of Facebook, Instagram or Google. The remarkable turnaround in FCF margin only happened in the last two quarters; hence there is no telling what the future would be, given the lack of strong competitive advantages. Plus, the price tag is more than $40 billion. It’s unfathomable to think that PayPal’s board would authorize such a gigantic splash for this reason alone.

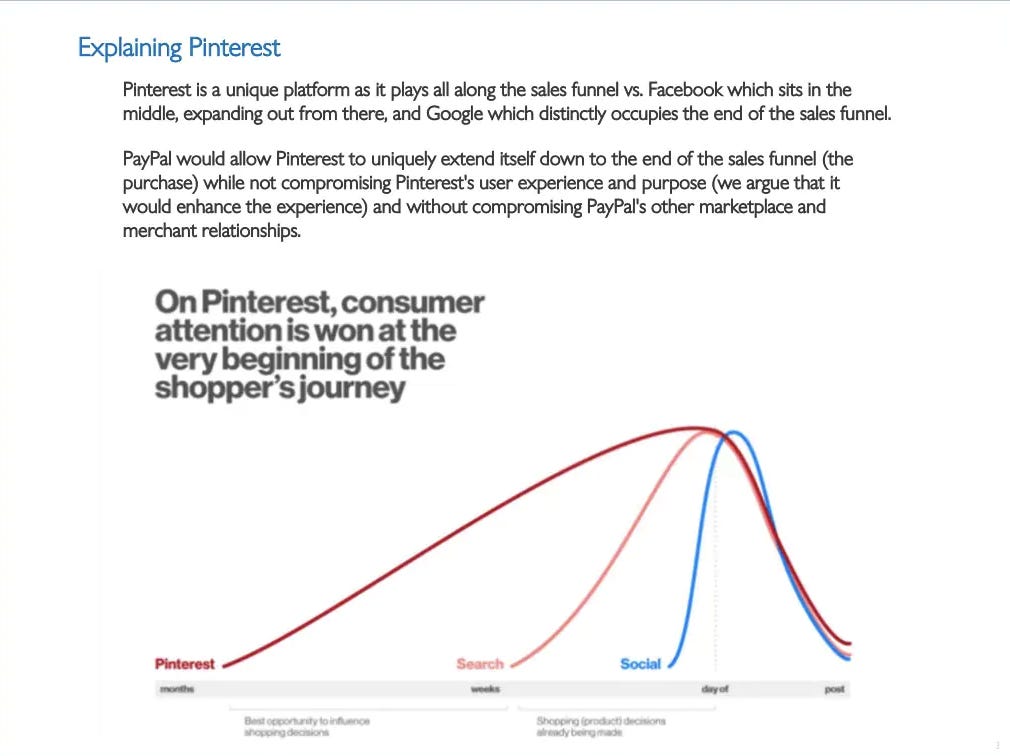

Would the acquisition be about the upper marketing funnel and closing the loop for PayPal?

At the bottom of the customer experience, aka the checkout page, is where PayPal excels with its breadth of both consumer and merchant services. What it doesn’t excel at, yet, is at the upper funnel where the interest seed is planted and where reach is generated. In other words, PayPal doesn’t have the capability or expertise yet to help merchants expand the customer pool. Last year, the company paid $4 billion for Honey, a browser extension that finds online deals and presents them to shoppers. To some extent, Honey helps PayPal address the issue of lead generation, but as a browser extension, there is only so much that Honey can do, especially on a global scale. At the time of the acquisition, Honey had 17 million active users. Not everyone who uses PayPal installs Honey on their browsers. Yours truly is one of those people.

With more than 450 million users across the globe, theoretically Pinterest could be the solution to this problem. However, the question is what the customer experience of PayPal + Pinterest would look like. The ramifications may have significant impact.

At the time of this writing, users can browse for ideas on Pinterest and be directed to merchant websites for further actions without even having to leave the red app if they choose to click on the hyperlinks that come with the Pins. The problem for PayPal is that this whole journey has nothing to do with them. Merchants choose which payment processor offers the best value, not which one owns Pinterest. If PayPal forced merchants to use their own product to use the social platform, it would backfire. In this scenario, there is no strategic value add for PayPal.

One possibility floated on the Net is that Pinterest could be PayPal’s eBay. Ironically, eBay owned PayPal from the early 2000s till their divorce in 2015 and since then PayPal has gradually reduced their reliance on eBay for transaction volume. I am not sure that PayPal wants to pay a mountain of money for something that they want nothing to do with any more. Even if PayPal wanted Pinterest to become their own eBay, running a two-sided global marketplace is a resource-consuming endeavor. After pouring $40+ billion in acquiring Pinterest, PayPal would have to spare valuable resources to help the acquired firm. Given the intense competition that PayPal faces and the head start in terms of marketplace that Facebook and Instagram have, this possibility, while not too wild, doesn’t sound appealing.

What I suspect is the crown jewel that might interest PayPal is the Taste Graph mentioned above. While the new PayPal app is definitely an improvement over its predecessor, the Shop tab is underwhelming. There are a bunch of offers on the tab, but there is little personalization. Hence, I don’t think at the current state, it helps merchants drive a lot of sale. In theory, PayPal could do a lot more personalization given the data on shopping behavior that it possesses. By mining transaction data, PayPal could know which merchants are one’s favorite, how often one shops at those merchants, which product categories (using Merchant Category Codes) are popular and even what items (SKU data) are shopped the most. By working with bureau agencies like Experian, PayPal could learn about financial status of its users such as how many trades are open, the total balance of all trades, the delinquency history and all that.

What PayPal doesn’t have is the interest data outside of the transactions processed on its platform. Let me give you an example. I am a huge fan of Manchester United and Scuderia Ferrari F1 team. But you wouldn’t know it if you merely looked at the transactions on all my credit cards, let alone only my PayPal account. PayPal could work with another company to acquire this data; however, this presents two challenges. If the data is not 1st-party data, it’s usually very unreliable. The Taste Graph is Pinterest’s intellectual property and 1st data. The reliability is certain. The other problem is that who has the global footprint that Pinterest has and available for an acquisition. Facebook, Google, LinkedIn, Twitter or even Snapchat isn’t available. I am sure PayPal could find another company with 1st party interest graph for the U.S market, but it’s not easy to find it for the global audience. If PayPal is serious about meeting their 4-year target, the U.S market alone wouldn’t cut it.

For good measure, PayPal likely doesn’t have the top of wallet share for its users. In other words, if an average person spends $1,000 a month, I don’t think that user will spend everything through PayPal. If I have to guess, PayPal only sees less than 30% of the wallet share. The implication is that they have no idea about the spending pattern and interest that lies in the other 70-80% of the wallet. So if they wanted to operate a serious deal-recommending engine on the PayPal app, they would want as much data as possible. As PayPal already strives to get users to spend as much as possible through their platform, increasing the wallet share organically takes time.

PayPal offers consumers all possible checkout options: BNPL, its mobile wallet, debit card, credit card and line of credit. It definitely wants the app to be the ultimate shopping app for consumers. Right now, a PayPal user like me doesn’t open the app unless I need to send somebody money. I figure that PayPal wants users to actually open the app and spend time there every day. To do that, they need to incentivize shoppers to visit and the best way is personalized deals. To grow its merchant base, the best way is to generate sales and leads for merchants. In my mind, the alleged acquisition of Pinterest could help with these two objectives. With that being said, $40+ billion is a huge price tag and acquisitions are generally challenging to pull off, especially expensive ones. I am also concerned about how much overlap there is between the two user bases. There is also a question of engagement of international users. Despite making up 80% of Pinterest MAUs, users outside the U.S bring only 20% of revenue. Is it because Pinterest isn’t popular among international advertisers? (I know there are Pinterest users in Vietnam, but I doubt there are brands and advertisers that actually use the platform) Or is it because user engagement isn’t high? While I can try to see the logic, I am not too comfortable with this major move.

Appendix

Leave a comment