The last quarter featured some great developments, acceptable numbers and a couple of concerns for PayPal, from my point of view.

The earning call started with the news that Amazon would let U.S customers check out on their website with Venmo. It’s a great win for the payment company as Amazon is the biggest eCommerce in the U.S, which is PayPal’s main market. The management team didn’t reveal much about the terms of the partnership, but given that Amazon has more bargaining power here, my guess is that PayPal has to offer some sweet economic incentives like a lower rate. In the 9 months ending September 2021, Amazon’s U.S sale was $197 billion, including hardware, physical stores, subscriptions etc. The company doesn’t break down the sale volume for its eCommerce, but for the sake of simplicity, let’s assume that Amazon.com generates around $200 billion in sales ever year. Even if Pay with Venmo processes 1% of that, it will still give PayPal a boost of $2 billion in Total Payment Volume (TPV). Not bad. You may ask given that Venmo TPV for this quarter is $60 billion alone, why is $2 billion lift a year not bad? Well, that’s because Venmo would actually generates money on this $2 billion lift in TPV while the reported $60 billion includes person-to-person (P2P) payments that earn Venmo almost absolutely nothing.

This kind of partnership is possible in the first place because PayPal is no longer constrained by legal obligations with eBay. Hence, we should see the company strike more similar deals in the future. Speaking of deals, PayPal also announced collaboration with Walmart, Booking.com, Fanatic, Phillips 66, GoFundMe and Everlane. At first glance, some of these deals make a lot of sense to me. Walmart is the biggest grocer in the country and a major retailer. Adding PayPal as a checkout option is huge and can help elevate PayPal’s TPV in the same way as Amazon would. 2/3 of Booking.com reservations are online. Since PayPal is already a checkout option, adding Venmo is a logical step to capture more of that payment share. Meanwhile, Everlane, as a fashion retailer, serves as a good case study for Happy Returns, which will be important to PayPal in acquiring and retaining merchants. Last but not least, offering QR codes at gas stations such as Phillips 66 and Valero facilitates seamless payments in a very familiar use case for all consumers.

BNPL has been an astounding success for PayPal. Launched in August 2020, the service already amassed $5.4 billion in transaction volume, $2 billion of which came in the last quarter alone, 9.5+ million users and 950,000 participating merchants. That’s about 2.5% of PayPal’s consumer base and 3% of its merchant base in only 6 markets so far. The potential growth is enormous. The company is introducing PayPal in 4 in Spain and Italy in Q4 2021 and planning new different flavors of its BNPL in the first half of 2022. I won’t be surprised if PayPal has $8-$10 billion in BNPL volume in the next 12 months (60% or 100% growth).

One of the biggest initiatives for PayPal is the launch of its new mobile app. It’s a major milestone towards being THE Super App for consumer financial needs. The early results, as reported by the company, were great. I don’t take much stock in them, though, because 1/ it’s still early and 2/ I don’t fully understand what all of the reported lifts mean. I’d rather wait for a couple of more quarters to see how the new app fares and hopefully the management team can give more color.

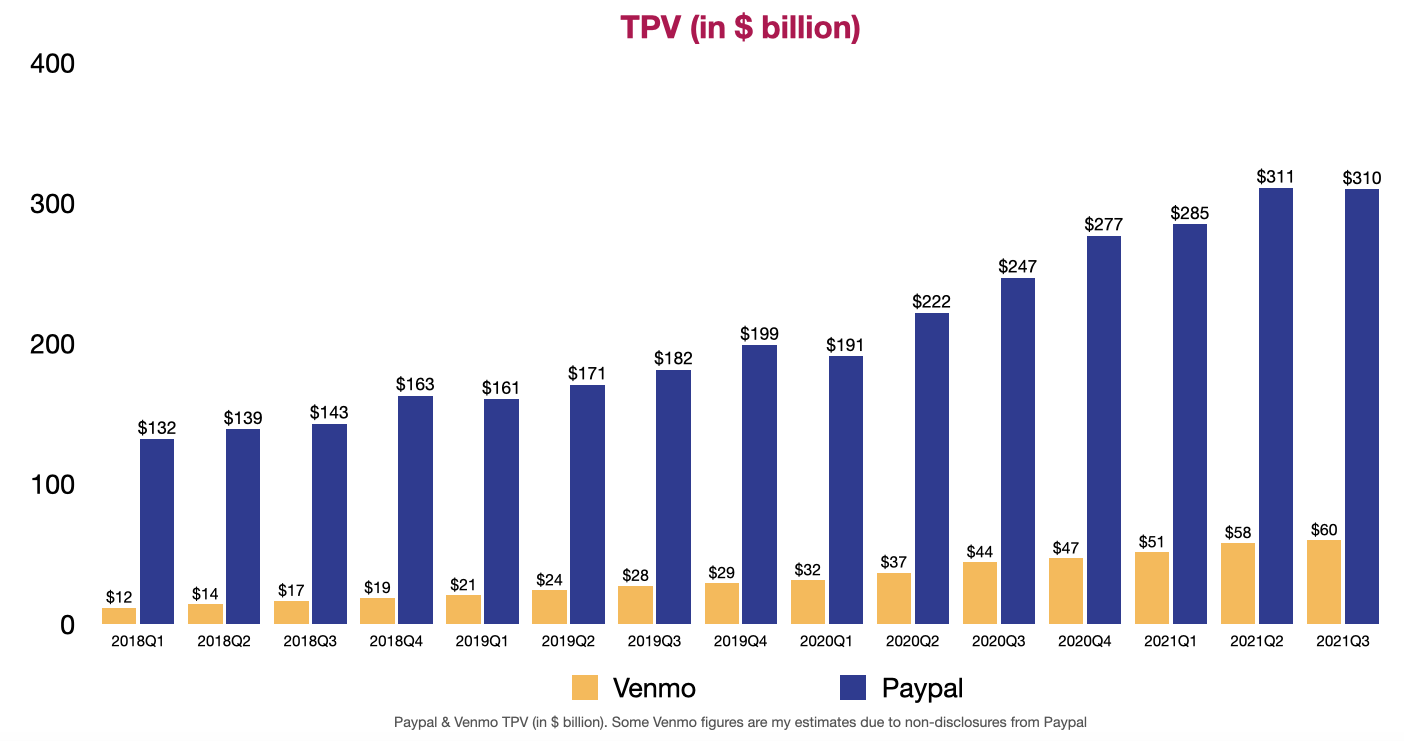

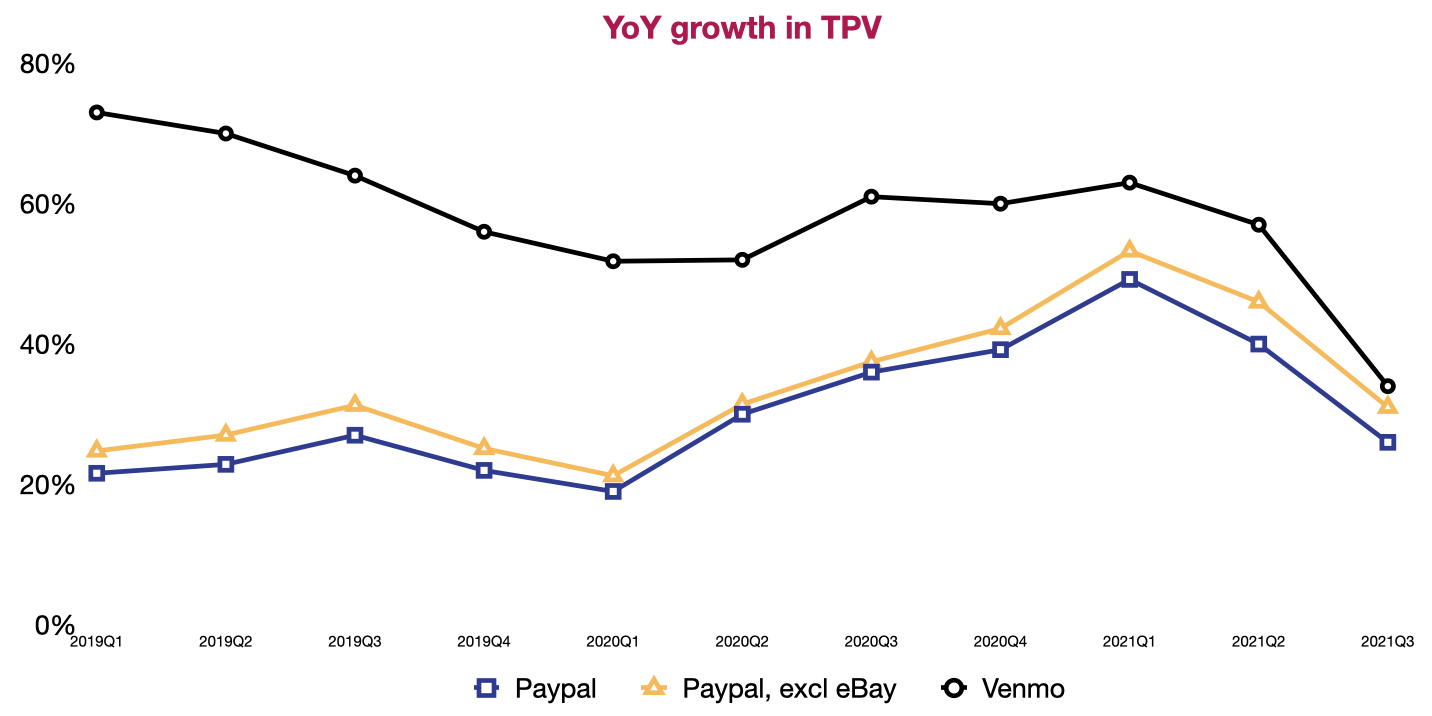

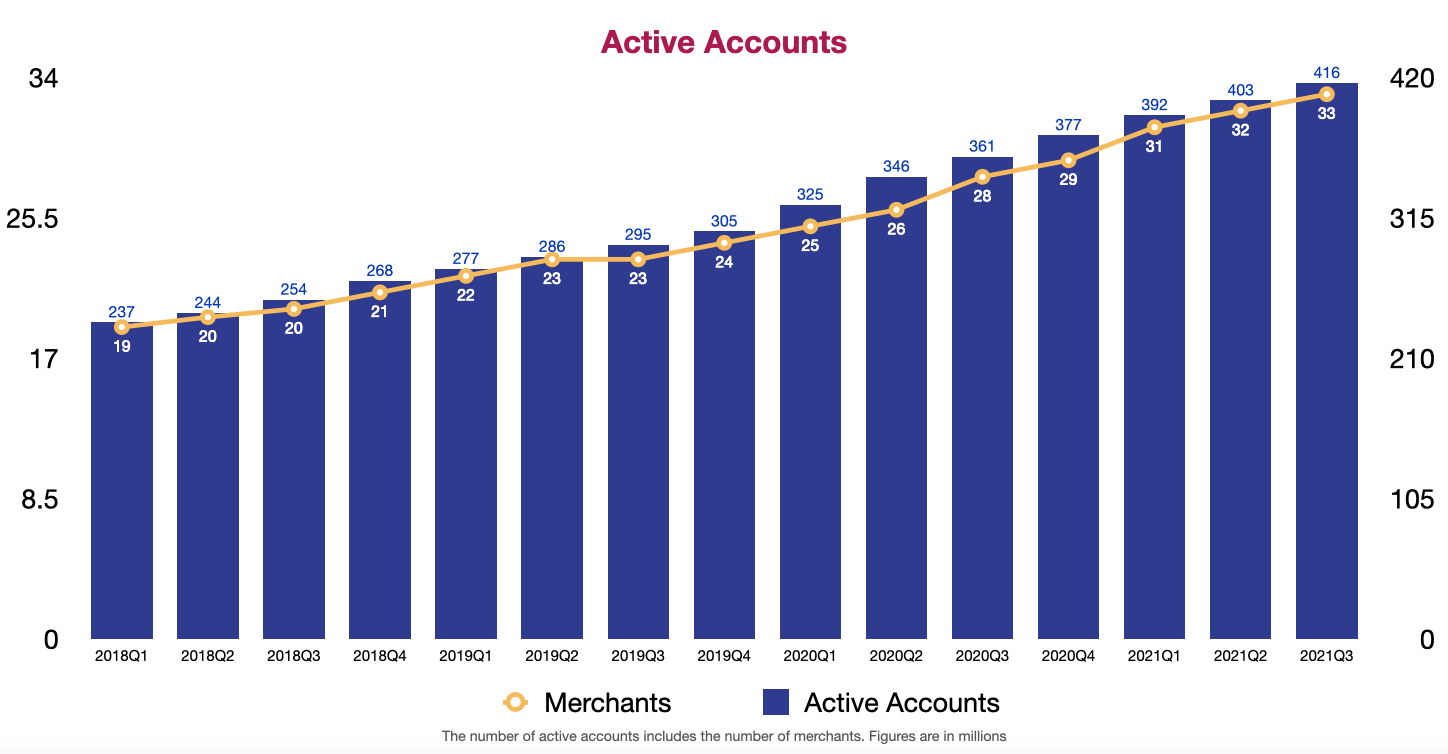

On to the numbers. The last quarter’s TPV stood at $310 billion, a 26% YoY growth. Excluding $10 billion in eBay TPV, which is 3% of the total figure and trending down, the YoY growth is 31%. While eBay is gradually becoming the past for PayPal, Venmo is increasingly looking like the future. Its TPV last quarter was $60 billion, up 35% YoY, faster than the main app itself. Even though it’s only available in the U.S so far, Venmo managed to grow its TPV by more than three folds since 2018. In terms of active accounts, as of Q3 FY2021, PayPal had 413 million active accounts, including 80 million Venmo accounts and 33 million active merchants. Transactions per active account came in at 44.2. Transaction and total take-rates continued to trend down, standing at 1.88.% and 1.99% respectively in Q3 FY2021. As the reliance on eBay tapers off and the product mix is unfavorable (more bill volume or more volume from partners like Amazon that have lower rates), I expect this trend to continue for the foreseeable future.

The decrease in take rates will continue to heap pressure on revenue. Q3 FY2021 revenue growth already slowed down to 13%, much lower than what was reported in the previous four quarters. If we isolate the revenue from value added services which have little to do with the core business of PayPal, revenue growth is clocked at 10%. International revenue only grew by 2% YoY. This is particularly concerning if the management team wants to meet the goal set on Investor Day. To reach $50 billion in annual revenue at the end of 2025 starting with $25 billion in revenue this year, PayPal would have to grow the top line by at least 25%. Growth at the current clip is not going to cut it. On the Q3 Investor Update presentation, PayPal mentioned that the acquisition of Paidy would add 3 million new net accounts in 2021, but said nothing about revenue lift. I suspect that the company will continue to use M&A to aid with the growth numbers in the future. Is it a good approach? It could be, though every M&A carries a certain level of risks and you can’t fault people for doubting your own organic growth if you rely on M&A.

Back in Q2 FY2021, PayPal made a major change to their pricing that went into effect on the 2nd of August 2021. Essentially, merchants will have to pay PayPal more in commission when consumers use the company’s branded mobile wallets such as PayPal, Pay with Venmo, PayPal in 4. On the other hand, when consumers key in card information without using PayPal’s wallet options, merchants will incur slightly lower rates. The assumption behind this move is that PayPal is confident in the attractiveness of its own mobile wallets. According to the latest 10-Q, the company claimed that the pricing changes didn’t meaningfully affect revenue. While it sounds encouraging, it has been only two full months. So we’ll have to wait a bit before rendering any verdict.

In summary, I’d give the quarter around 7 out of 10. The numbers aren’t catastrophic. We may just see the effect from a tough comparison from last year and the rule of big numbers. What concerns me more is that I don’t have enough information as of now to believe that they can hit the aggressive goal set for FY2025.

Leave a comment